bymuratdeniz/iStock via Getty Images

Investment thesis

Viant Technology (NASDAQ:DSP) is a digital ad platform that enables advertisers and agencies to purchase ads across various channels, with a primary focus on video-related ads such as CTV, a market that is growing at nearly 20% annually. The company’s recent growth and improving margins have been fueled by its latest AI-driven product offerings, which aim to significantly enhance ROI for its clients. Looking ahead, management plans to expand its AI-based solutions to deliver even greater value, which will in turn lead to increased spending by clients on its platform. Despite this optimistic outlook, I believe that the shares are fully valued at an EV/FCF multiple of 20. Given the competitive pressures from larger players and the absence of a reasonable margin of safety at this valuation, I maintain a Neutral rating on the shares.

Financial highlights and my expectations looking ahead

Q2 Investor Presentation

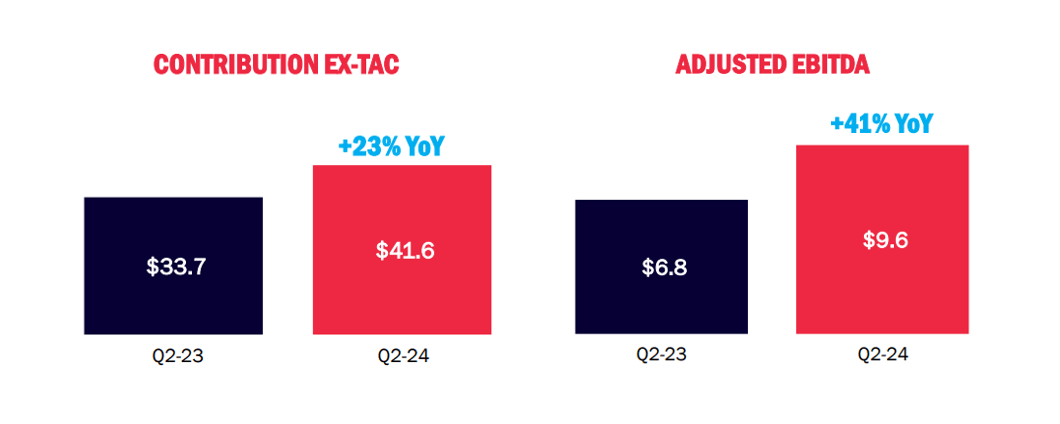

Viant delivered a 23% year-over-year increase in contribution ex-TAC for Q2. Adjusted EBITDA grew 41% to $9.6 million as shown above, reaching a margin of 23%, demonstrating the operating leverage in the business. One of the key drivers for growth in the quarter was the release of version 2 of the company’s bid optimizer product, which makes AI-based recommendations for its clients on how to deploy campaign budgets across different channels through advanced ad strategies. According to commentary from management at a recent investor conference, this product has helped customers reduce their bid prices by as much as 50%. As the company introduces new AI-based products in areas such as measurement and planning, which enhance clients’ ROI, it is expected to drive increased spending on the platform and contribute to strong revenue growth.

Looking ahead, management has guided for contribution ex-TAC and adjusted EBITDA of $45 million and $11.5 million, respectively, for Q3. Management, however, does not provide full-year guidance. According to my estimates, I see contribution ex-TAC and adjusted EBITDA for Q4 at $50 million and $15 million respectively. This implies a strong growth year-over-year growth of 17% in Q4, which is seasonally the strongest quarter, while also benefiting this year from increased political spending related to the US presidential elections. CTV, which is one of the company’s core segments, is especially expected to see a significant boost from political spending, which is estimated at $1.56 billion. I believe the positive impact from political spending will be higher than management’s own estimate of 200 to 300 basis points, and have therefore incorporated this expected outperformance in my estimates, which I will later also use in my valuation model.

Given the company’s large net cash position of $210 million and the expectation for continued FCF generation in upcoming quarters, capital allocation becomes a crucial aspect for shareholders. I anticipate that the company will primarily use its excess cash for share repurchases, particularly to counteract dilution from stock-based compensation (SBC). Although the company has explored acquisitions in the past that did not come to fruition, I do not expect significant M&A activity in the near term.

Valuation

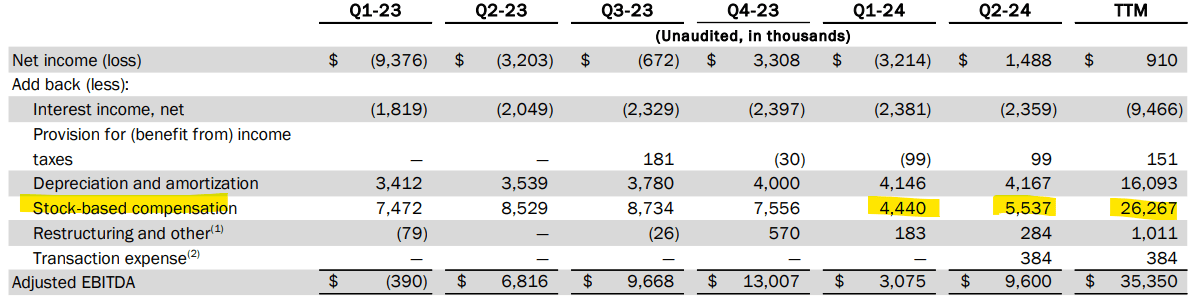

By combining management’s guidance for Q3 and my estimates for Q4, I arrive at estimates of $171 million and $40 million for contribution ex-TAC and adjusted EBITDA for the full year. Accordingly, I expect FCF generation to be approximately $24 million. I arrive at this figure by deducting the company’s cash expenses towards capital expenditures, which is around $16 million annually. I assume tax payments will be insignificant, given that the company is expected to be unprofitable on a GAAP-basis. The main reason behind weaker GAAP profitability is the elevated level of SBC, which is currently at an annual run-rate of $26 million, as shown below.

Q2 Investor Presentation

At the current share price of $11, the company has a market cap of $700 million. Given its net cash position of $210 million, it has enterprise value is $490 million. This implies that shares are trading at Price/FCF and EV/FCF multiples of 29 and 20 respectively. Given the analyst estimates for low double-digit growth in the medium term, this valuation reflects a significant premium versus AdTech peers like Magnite (MGNI) and PubMatic (PUBM), which have high single-digit growth rates, and trade at Price/FCF multiples of around 10. One of Viant’s major competitors, The Trade Desk (TTD) is growing well above 20% and trades at a significantly higher Price/FCF multiple above 60. However, I believe that TTD’s valuation is not directly comparable to Viant’s due to its substantially larger scale, stronger growth, and superior margins.

In terms of valuation, I consider DSP shares to be fully valued at their current price. While the valuation may not be particularly attractive, I do not see significant downside given that the company is FCF generative and has a large cash position related to its market cap.

Risks to consider

Competition

Viant faces tough competition from much larger DSPs such as Google’s (GOOGL) (GOOG) DV360, Yahoo Advertising and The Trade Desk. Viant seeks to differentiate itself by offering its clients a superior ROI on their ad spend by leveraging its proprietary cookie-less Household ID solution for user targeting. Speaking of its product’s performance compared to rivals, its CEO stated:

It’s the scale of the household ID versus other DSPs, all other DSPs out there as an alternative identifier that works holistically. That continues to be a point that we’re driving home. And the productivity of using our software to buy media versus a different software, I think we’re starting to show market differences and we’ve got new products in the pipeline that I think can expand that leadership position we have today.

Dependence on video

According to management, video ads, including CTV, represented over 60% of the total spend on its platform during the quarter. Given that these ads typically command higher CPMs, Viant must consistently deliver compelling ROIs to ensure that video advertising remains an attractive option for clients compared to alternatives such as social media, digital out-of-home (DOOH), and audio ads.

Macroeconomic impacts

Client spending on Viant’s platform is likely to be adversely affected by a weaker economic environment. As I discussed previously, the company is expected to benefit from political spending in the next two quarters related to the US Presidential elections, which will lead to tougher comparisons during Q3 and Q4 next year.

Conclusion

While the company has a promising outlook for growth and improving profitability as it plans to introduce new AI-based products designed to enhance ROI for clients’ ad spend, I believe the current valuation fully reflects this optimism. Due to the lack of a sufficient margin of safety given the associated investment risks, I maintain a Neutral rating on the shares.

{kind=link}