alexeynovikov

Elevator Pitch

I have a Hold investment rating for Sumitomo Corporation (OTCPK:SSUMF) (OTCPK:SSUMY) [8053:JP].

My earlier December 15, 2023 initiation article drew attention to Sumitomo Corporation’s portfolio restructuring efforts, the company’s recent quarterly performance, and the stock’s valuation metrics.

The focus of the current update is SSUMF’s latest fiscal year financial results, and its new financial goals. Sumitomo Corporation’s weaker-than-expected headline net profit for FY 2023 (YE March 31, 2024) implies that the company still has a lot of work to do in terms of restructuring its business portfolio. Based on my analysis, the stock’s current valuations have already priced in the company’s FY 2026 financial goals. Therefore, I see no reasons to change my existing Hold rating for Sumitomo Corporation.

Readers should be aware that they can trade in the company’s shares on both the Over-The-Counter market and the Tokyo Stock Exchange. The 10-day mean daily trading values for Sumitomo Corporation’s OTC shares and Japan-listed shares were $200 million and $1 million, respectively as per S&P Capital IQ data. Interactive Brokers is one of the US stockbrokers that allows their clients to buy and sell Japanese shares.

Most Recent Fiscal Year Net Profit Came In Below Expectations

Sumitomo Corporation issued an announcement disclosing its financial results for fiscal 2023 or the year ended March 31, 2024, on Thursday, May 2.

The company’s net income attributable to shareholders dropped by -32% YoY from JPY565.3 billion for FY 2022 to JPY386.4 billion in FY 2023. This turned out to be -23% lower than the sell side analysts’ consensus bottom-line estimate of JPY500.9 billion (source: S&P Capital IQ).

I noted in my mid-December 2023 initiation piece that SSUMF’s “short-term financial performance could be possibly affected by portfolio changes” considering that “some of the company’s businesses still have ROICs (Returns On Invested Capital) below their WACCs (Weighed Average Costs of Capital).” This has turned out to be the main reason for Sumitomo Corporation’s substantial FY 2023 earnings miss.

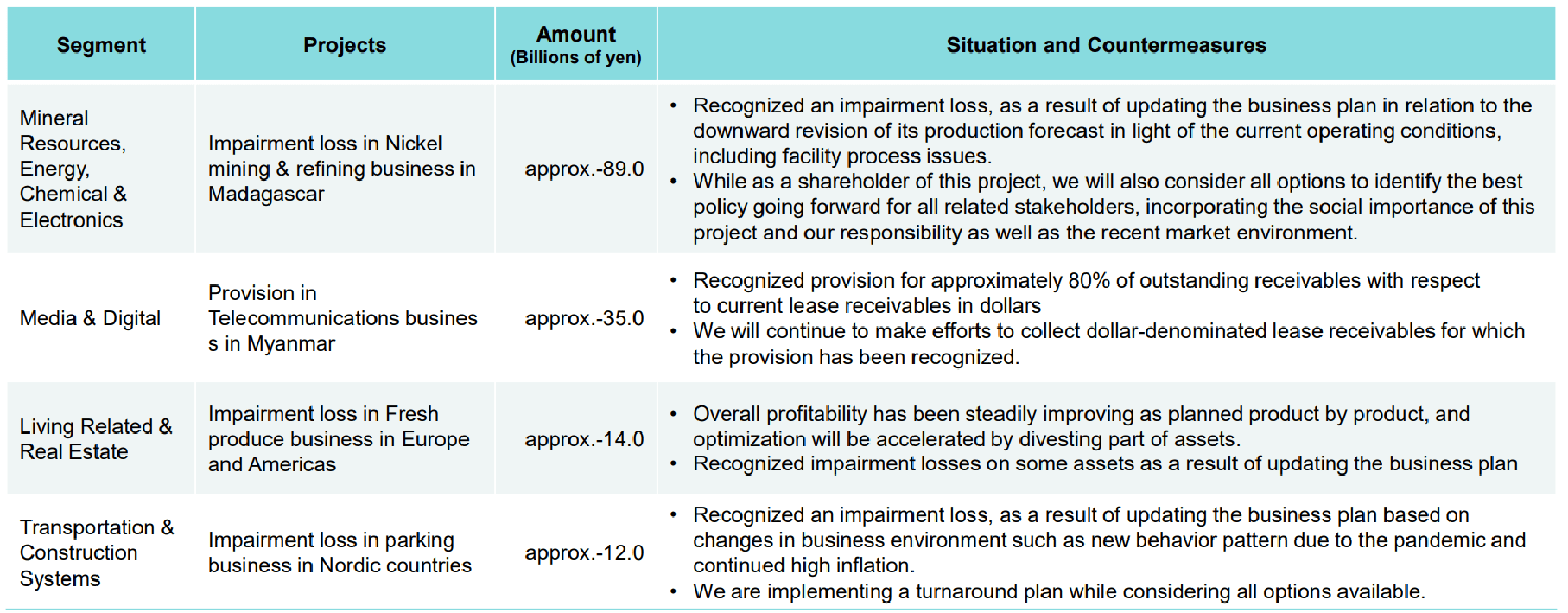

Some Of Sumitomo Corporation’s Key Non-Recurring Items For FY 2023

Sumitomo Corporation’s FY 2023 Earnings Presentation Slides

In its FY 2023 results presentation slides, Sumitomo Corporation shared that it suffered from “one-off profits/losses” (including but not limited to those outlined in the chart above) amounting to -JPY114.0 billion. In other words, SSUMF’s core earnings adjusted for non-recurring items, would have been JPY501.0 billion, or in line with the market’s consensus JPY500.9 billion net profit forecast.

Nonetheless, the substantial impairments and provisions that the company took for certain of its businesses in the latest fiscal year have negative read-throughs. With my prior December 15, 2023 write-up, I cautioned that “it will take some time before Sumitomo Corporation can realize some success associated with the company’s ongoing portfolio restructuring process.” My unfavorable view of SSUMF’s portfolio restructuring progress is validated by its below-expectations headline FY 2023 earnings, which were impacted by write-downs for its underperforming businesses.

New Financial Targets Have Been Factored Into The Stock’s Valuations

In conjunction with its FY 2023 earnings release, SSUMF also published a report revealing its “new medium-term management plan (FY 2024-FY 2026).” In specific terms, Sumitomo Corporation intends to deliver a ROE of at least 12% and a net profit attributable to shareholders of JPY650 billion for FY 2026 (YE March 31, 2027).

Sumitomo Corporation currently trades at a consensus FY 2024 normalized P/E of 9.9 times (source: S&P Capital IQ). In comparison, the implied three-year forward earnings CAGR is +9% based on its FY 2023 adjusted net income of JPY501 billion and its FY 2026 bottom-line goal of JPY650 billion.

The company’s expectations of a +9% annualized bottom-line expansion for the coming years are positive. But the stock is already trading at a PEG (Price-to-Earnings Growth) multiple of 1.1 times (9.9/9) that is indicative of fair valuation.

Separately, the market is now valuing Sumitomo Corporation at 1.2 times trailing P/B as per S&P Capital IQ data, which is close to what I deem as a fair P/B multiple for the name. My target P/B metric for Sumitomo Corporation is 1.25 times.

A P/B ratio is derived by dividing [Return on Equity minus Perpetuity Growth Rate] by [Cost of Equity minus Perpetuity Growth Rate] based on the Gordon Growth Model. My Return on Equity, Cost of Equity, and Perpetuity Growth Rate assumptions are 12%, 10% , and +2%, respectively. 12% is the company’s FY 2026 ROE target. The industry average cost of equity for US diversified companies is about 9.38%, so I have chosen to use a 10% cost of equity assumption for Sumitomo Corporation. For the Perpetuity Growth Rate, it is typical to use the long-run global economic growth rate at the low single digit percentage level.

In other words, SSUMF’s 12% ROE target for FY 2026 is already reflected in the stock’s P/B valuation metric. Furthermore, Sumitomo Corporation had delivered a superior ROE of 16.2% for both FY 2021 and FY 2022.

In summary, Sumitomo Corporation’s current P/E and P/B valuations are aligned with the company’s FY 2026 financial expectations. As such, I don’t expect a further valuation uplift for the stock, even if the company does deliver on its intermediate term ROE and earnings growth target.

Concluding Thoughts

A Hold rating for Sumitomo Corporation is maintained. The company’s recent results validate my view that the company’s portfolio restructuring efforts are still a work-in-progress. Also, SSUMF’s new FY 2026 financial goals are already priced into the stock’s valuations as seen with the stock’s P/B and P/E ratios.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}