wildpixel

My Thesis Update

Initially, I began covering the S&P 500 index (SP500) (NYSEARCA:SPY) at the end of January 2024, highlighting a risk I perceived for the market at that time – that risk, which hasn’t materialized eventually, involved the potential for growing inflation due to another supply chain disruption. The market didn’t consider rising inflation as a base scenario for future developments (and so inflation was indeed getting lower), and to this day, it remains non-priced. However, I believe that ignoring this risk today could lead to serious consequences or at least limit future growth opportunities for SPY buyers. That’s why I still think investors should consider underweighting SPY in their portfolios.

My Reasoning

First off, let me start by updating the information regarding what the market participants are pricing today. According to Yardeni Research, the S&P 500 index is now trading at 20.7 times forward earnings (based on 52-week consensus operating EPS), which is ~14% below its 2000 peak but way higher than its pre-2008 average. Compared to the long-term median figure, today’s multiple is 10.7% higher:

Yardeni Research [August 2024]![Yardeni Research [August 2024]](https://static.seekingalpha.com/uploads/2024/8/24/53838465-1724485702867238_origin.png)

As you probably guessed, the main driver of market valuation growth in recent months has been the mega-cap stocks. Never in the history of SPY trading has there been such a wide deviation between the top 10 stocks and the other 490 companies in the index:

Yardeni Research [August 2024]![Yardeni Research [August 2024]](https://static.seekingalpha.com/uploads/2024/8/24/53838465-17244858454005005_origin.png)

The U.S. economy continues to grow rapidly: consumers are still spending, the labor market is strong, and inflation is moderating. Many justify the overall market growth by expecting the remaining 490 companies to start catching up with the top 10, further fueling today’s rally. Additionally, I frequently encounter the opinion that the current deviation of mega-cap stocks is logically explainable: the AI race is progressing rapidly, and it’s likely that the largest companies in the index (all major tech firms) will be the main beneficiaries due to their scale. However, I see a potential issue with this view: if the market shares of the remaining non-top-10 firms fall sharply, it contradicts the idea that they should catch up with the top 10 companies.

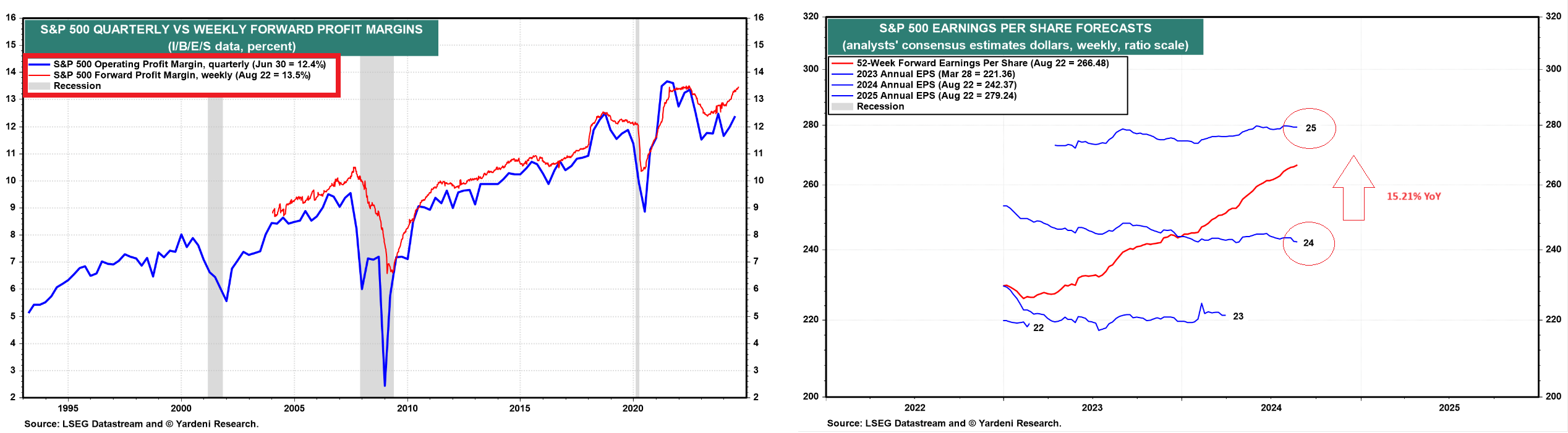

Anyway, the main market assumption that drives stock prices higher today lies in the future operating margin expectations. Apparently, due to continued falling inflation and optimizing business processes through artificial intelligence, the market expects SPY’s EPS to grow by about 15.21% in 2025, YoY.

Artificial Intelligence is revolutionizing business processes, driving operational excellence through automation, optimization, and enhanced decision-making. By leveraging AI, companies can streamline workflows, improve efficiency, and deliver superior customer experiences. As AI technology continues to evolve, its role in achieving operational excellence will only become more significant, offering businesses new opportunities to innovate and excel in a dynamic market environment.

Source: Gazetrail Consulting, emphasis added by the author

This suggests that the long-term trend of increasing margins, according to consensus forecasts, should continue even further:

Yardeni Research, Oakoff’s notes

This brings me to the analysis of a risk that, in my opinion, the market has not yet accounted for – the possibility of a new round of inflation.

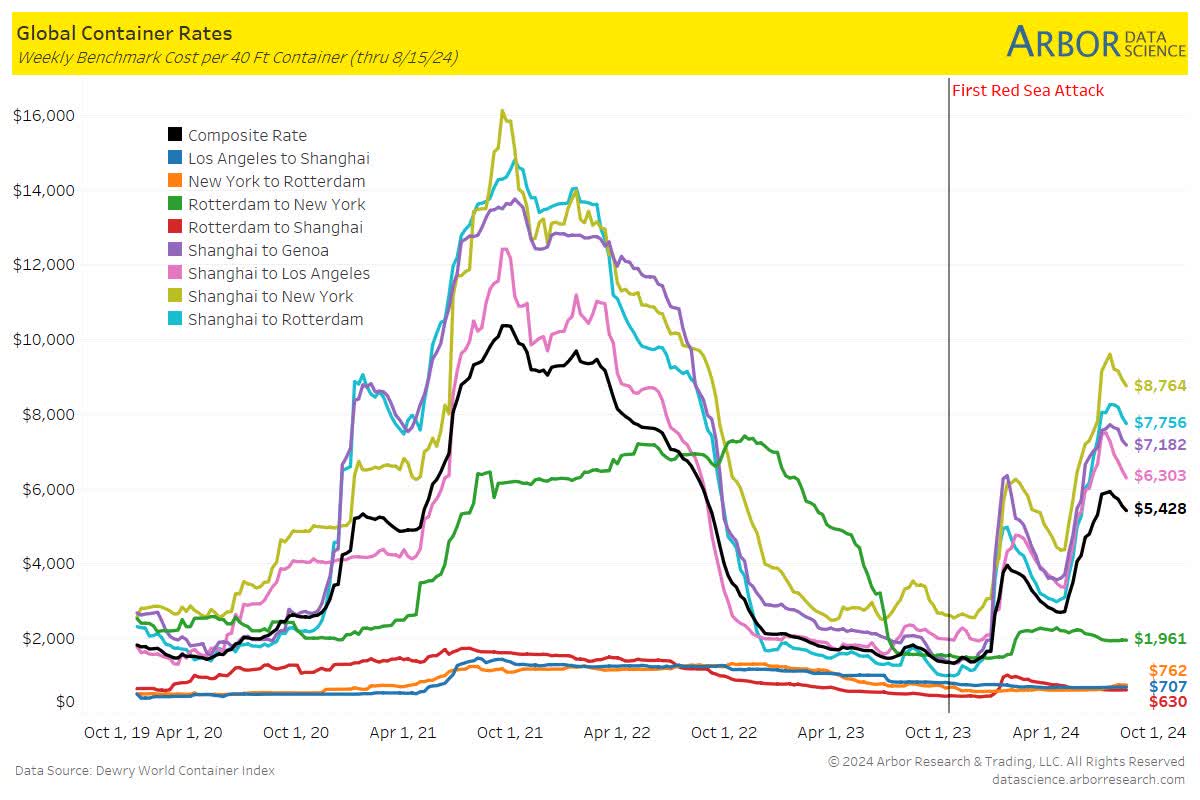

I understand that this idea may seem somewhat marginal in current economic circles so to speak, i.e. it is not widely recognized and may not quite align with the latest economic data. However, the issue I raised at the end of January, namely the growth in freight rates, is still relevant. In fact, it has worsened as rates have risen even further since then and are no longer falling as fast as they were rising.

Arbor data, shared by @LizAnnSonders on X

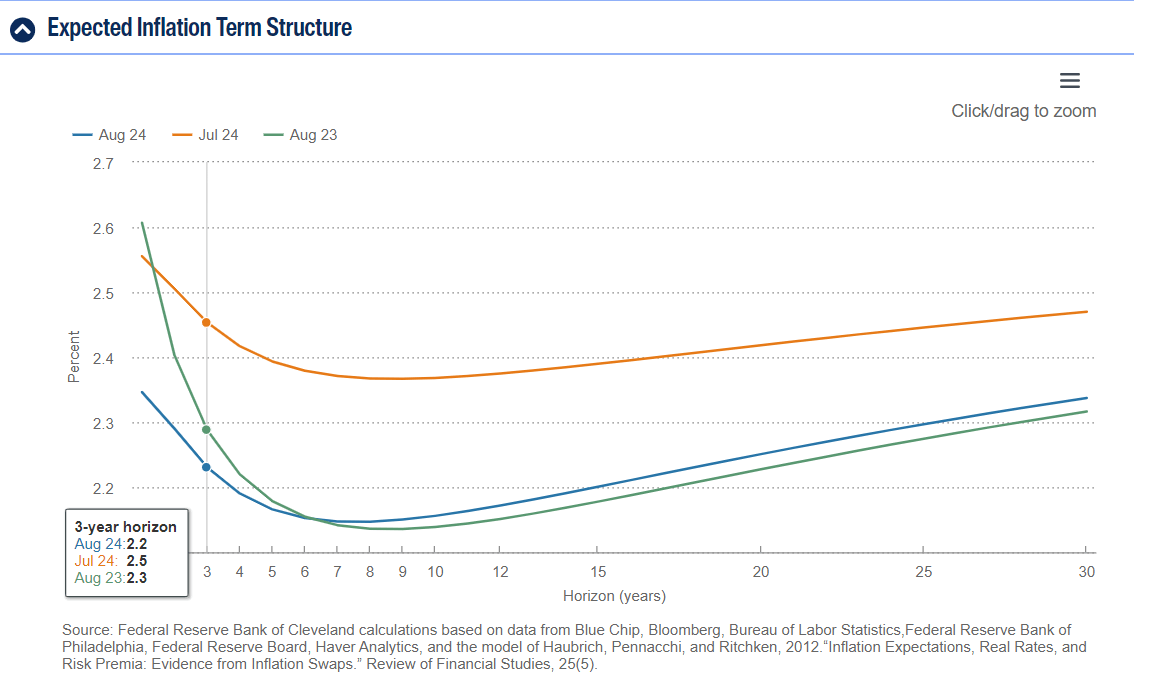

In my opinion, the nature of inflation dependence on freight rates has a kind of lag: As these rates remain relatively high, they slowly but surely begin to gradually become embedded in the cost of imported products, which in the end make the final products you buy more expensive. Consequently, some time may pass before year-on-year inflation rises again. I can’t time it, and neither can anyone else. However, as we can see from the inflation expectations for the coming years, this possibility is not reflected in the consensus.

Cleveland Fed data

Obviously, the situation today is very different from the one that triggered the rapid growth of freight rates in 2021. Back then, rates were primarily driven up by a lack of vessels, leading customers to pay any delivery price. Today, the situation is somewhat different. As I previously assumed, the new supply of container vessels entering the market in the coming years should fully compensate for demand, and at some point, rates should indeed go lower. However, the ongoing crisis in the Middle East over the past six months, affecting the security of the Suez Canal, has shown no signs of resolution. From a geopolitical standpoint, as I see it in the news today, there’s no apparent common ground between the conflicting parties. Therefore, I don’t think this crisis will be resolved anytime soon. And if it remains unresolved, these rates will likely stay higher for a longer period than many expect today. In that case, my assumption will likely come true: inflation should indeed rise because we’ll be comparing our basket of goods with a basket formed during a period when rates were much lower.

Let me clarify how freight rates may affect the cost of goods. Imagine you’re a retailer in the United States and you import products from abroad, for example from China. In addition to customs duties, you have to pay transportation costs. As these transportation costs increase, your goal as a seller is to maintain your profit margin. If transportation costs become a widespread problem in the market, especially in your niche, everyone will try to maintain their margins. This typically leads to an overall increase in the price of goods for US consumers as sellers pass the higher costs on to them.

While it’s difficult to calculate the impact of increased rates on the CPI accurately, I believe it’s clear that a large portion of goods imported into the US from Europe and Southeast Asia will be affected.

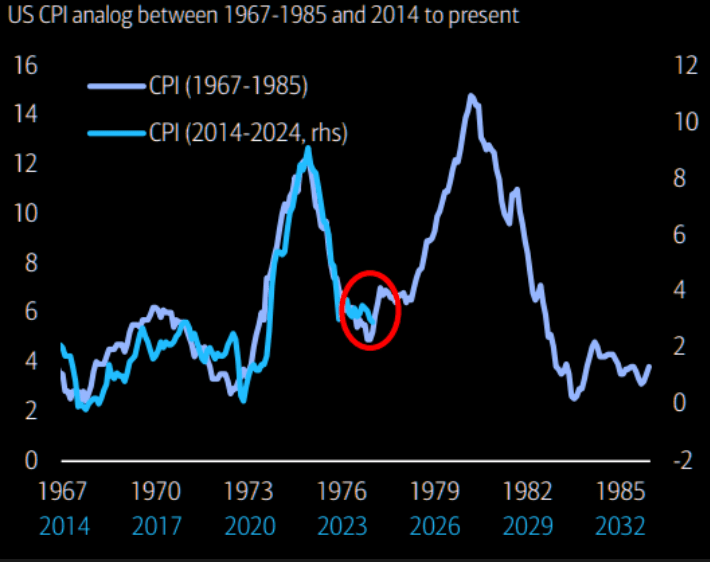

Many economists and fund managers compare the scenario I described above – the potential resurgence of inflation – to what we observed in the 1970s or 1940s.

While the macro environment today differs from that of the 1970s or 1940s, a lesson from history remains: inflation tends to develop through waves. We have recently witnessed the conclusion of the first wave and are likely in the process of reaching a bottom in the recent deceleration period, with a new upward trajectory underway.

Source: Otavio Costa on X, July 2024

And indeed, if we overlay the 1970s chart on how inflation behaves today, we see an almost perfect match, where the old momentum predicts a worsening inflation problem for us in the next few years:

BofA data, proprietary source

Well, I wouldn’t compare the two periods so directly, as there were different driving forces at play. However, in addition to rising transportation costs, we’re currently dealing with a trend toward protectionism in many countries (so-called “deglobalization”) and rising oil prices. Despite the push from environmental activists for a complete shift away from hydrocarbons, crude oil consumption remains stable. Also, the issue of underinvestment in the oil industry remains unresolved, even if some analysts believe it’s an overblown problem.

Be that as it may, the important thing is that the market today is not factoring the possibility of rising inflation into its baseline forecasts, although there are signs that such an omission may be misguided.

Your Takeaway

Long-standing market wisdom suggests buying when fear is prevalent. However, I currently see no fear among market participants; instead, there’s widespread optimism about how artificial intelligence will transform operations across all 11 sectors of the S&P 500. While this may be true, it’s crucial to remain realistic given the premium valuations: When allocating assets within your portfolio, consider reducing preference for SPY, as it’s based on overly optimistic forecasts that often overlook emerging risks. From what I see right now, the risk of inflation shouldn’t be dismissed, even if many believe it is a thing of the past. If my conclusions are correct, another market correction could severely impact those buying SPY at current prices.

Good luck with your investments!

{kind=link}