nuttapong

The macroeconomic environment has been challenging, to say the least, since 2020. There was the pandemic, which was followed by a surge in re-opening, followed by supply chain disruptions and war in Europe. We now find ourselves on more stable footing. But for the long-term investor, all of this is just noise. Where are the bargains and what companies are trading at unfair valuations relative to their medium and long-term growth potential?

Enter Rentokil (NYSE:RTO) – the king of an industry that is neither sexy nor highly visible in society.

Rentokil Commercial Website

That industry is Pest Control. Rentokil is the amalgamation of two major brands – Rentokil and Initial, which form their key service brands. Rentokil is the market leader in the majority of the 81 companies that it operates and employs more than 43,000 people worldwide. It has grown significant and major businesses broken up in the following regions:

- North America

- Europe

- UK

- Latin America

- Asia and Pacific

- Rest of World

The bulk of revenue comes from Pest Control and also Hygiene services (delivered through Initial) and they use economies of scale, and digital technology to deliver those services efficiently across the globe.

Market

Rentokil controls 21 percent of the global market for pest control, according to analysts at Oppenheimer research.

This is a very large market estimated to reach $42.5 billion by 2032, growing at a CAGR of 5.7% with reasonably high margins.

Allied Market Research Report 2023

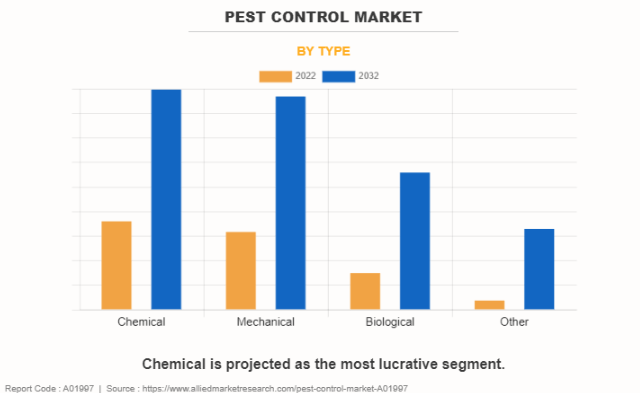

The pest control market tends to be focused in the chemical pest control segment and mechanical:

Allied Market Research Report 2023

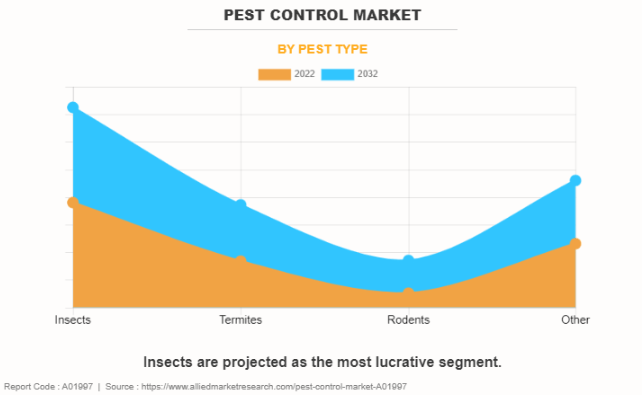

In terms of pests, the focus is on insect control and specifically termites, which is great for Rentokil because they acquired Terminix as a brand recently. More on that to follow:

Allied Market Research Report 2023

Rentokil’s main clients and customers are commercial and residential pest control. North America is the biggest market and it is also the fastest growing.

One thing that’s quite enticing in Allied Market’s research report is the fact that significant population growth, the increase in people moving to big cities, and climate change are all having an impact on pests and increasing the need for services in this area.

The business is investing significantly in leveraging post-merger cost efficiencies and to capitalise on its significant US market presence, with continued de-leveraging as it seeks to consolidate its position.

Key issues

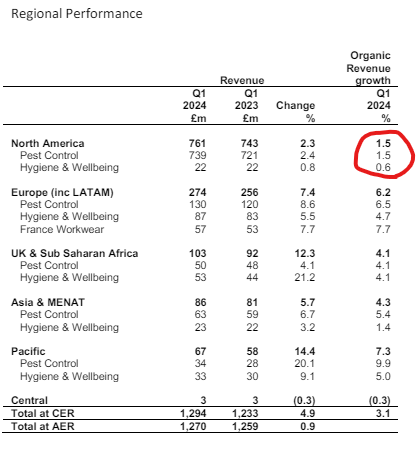

Following its acquisition of Terminix – a $6.7 billion dollar deal nailed down in October 2022 – there have been teething problems that are not immediately apparent. Reported headline figures at the last annual update were revenue increases of 45% and adjusted operating profit bumping up 57%. What that masked became clearer in the Q1 2024 update on 18th April, which showed quarter on quarter revenue growth of 0.9% on actual exchange rate basis and factoring in for the acquisition. (Rentokil quarterly report April 2024).

CEO Andy Ransom re-iterated guidance of 2-4% Organic Revenue growth for North America and expectations that results would be weighted towards H2. Total group wide organic revenue growth was 3.1% on a quarter by quarter basis for Q1.

The regional update highlights the problem – North America:

Rentokil Q1 Trading Update 2024

There are teething problems post-acquisition that are weighing on their key US market. In comparison to its market peers Rentokil has been losing market share to competitors as results flat-lined in Q4 and into Q1.

In the 2023 preliminary results the bug-bear surfaced:

Nevertheless, we recognise that the business was not sufficiently effective in attracting and closing sales leads. In 2023, integration planning focused attention on organisational change. Our marketing and sales leadership underwent considerable change, which in part affected our marketing performance to generate leads and convert sales (close rate in H2 was flat with prior year). Increased digital marketing spend by the competition and flat sales colleague retention (c.60% in Terminix and c.77% in Rentokil) compounded the overall impact. There was also a slightly disruptive influence felt from branch closures and pilots” Preliminary Results & Statements, Rentokil 2023

The market has continued to price in this bad news and the idea that perhaps the Terminix acquisition was a bad idea, they overpaid, and potentially it will not add as much to group profitability as they expected.

Is this the case?

Buffett-Style Assessment of Balance Sheet, Income Statement, Company

For me, there are three things to assess. How has Rentokil done as a revenue compounder, and what’s it like in terms of profitability, that is, converting working capital into cold hard cash? How well functioning is the underlying business? Let’s cover them in turn.

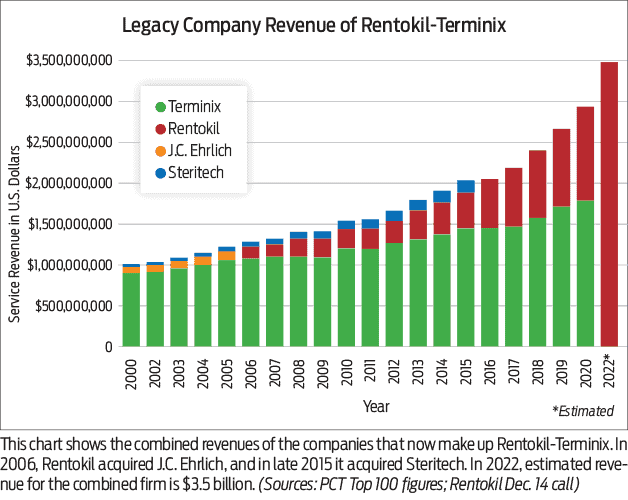

If we look at Revenue Growth and take a fairly long-term view, the company has done an excellent job at M&A and long-term focused growth:

PCT Top 100 Figures

2023 saw Revenue hit £5.375 billion, and consensus analyst forecasts for Revenue are for £5.52 billion and £5.79 billion over the next 2 years. So the expectation on Wall Street is that Rentokil will flat line over the course of the next 2 years as it absorbs Terminix and integrates it into the business, which ties in with the expectation that this will be done by 2026.

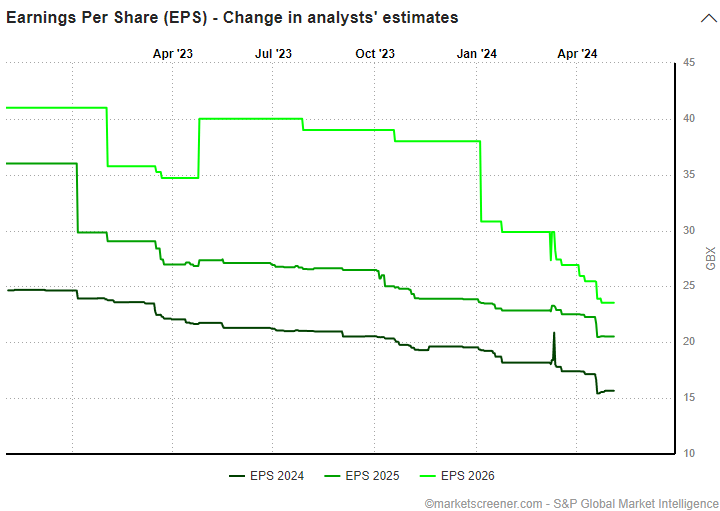

EPS – Analysts have in turn been racing amongst themselves to downgrade EPS estimates for 2025 and 2026:

S&P Global Market Intelligence 2023

This is quite stark since the acquisition:

S&P Global Market Intelligence 2023

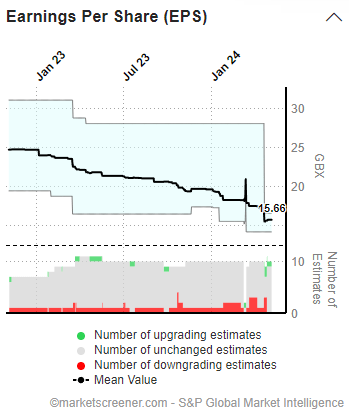

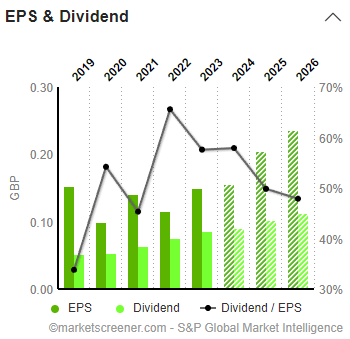

There are forecasts for EPS and Dividend growth, and it looks like the market and analysts are currently sceptical of the ability of management to deliver on them out to 2026:

S&P Global Market Intelligence 2023

It’s pretty normal for a business that has tacked on a substantial acquisition to see limited revenue growth in the first year or two. The business went from £3.7 billion in sales to £5.3 billion and really needs to get a grip on managing it in their biggest market. What I like here more than anything is that the lack of organic growth in North America appears to be priced into the shares.

Buffett-style analysis of the company. I use a rubric I developed after reading Warren Buffett and the Interpretation of Financial Statements by David Clarke and Mary Buffett. It’s helpful to be able to drill deep down to bedrock and think in terms of what makes a company tick, and how it makes money.

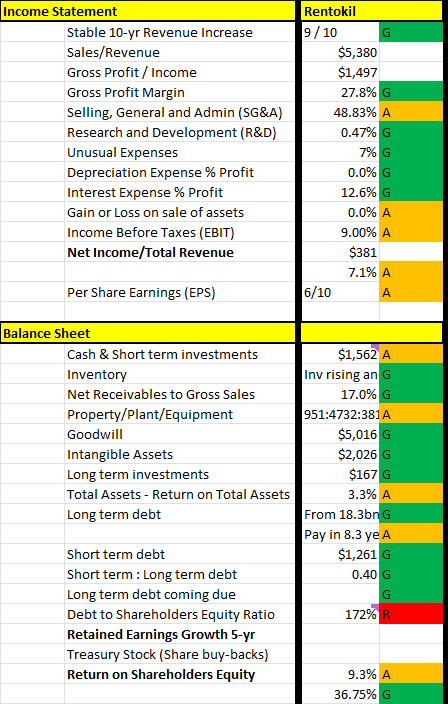

Let’s take a look at Rentokil:

David Huston, 2024

The company clearly has issues related to taking on such a big acquisition, but it’s in solid shape. SG&A expenses are too high and warrant an amber score. They have risen since 2019 from £323 million to £731 million, which is gobbling up cash. However, you would expect this to come down as they improve operational efficiency.

Fundamentally, this is not a high-profit margin business. Net income (EBIT) is about 9% and the analyst consensus forecasts for net margin is 9.32% for 2024.

On the balance sheet, Buffett likes to look at the ratio between PPE, Debt and Net Earnings. It’s a great way to think about the big levers of a business. How much stuff does the company need (PPE = Property, Plant and Equipment) and how much debt (total debt) is required to produce so much net income after taxes? In Rentokil’s case, we need £951 million PPE and £4.7 billion in debt to produce £381 million in net income. It’s actually not bad, given that the debt pile includes major acquisition costs. But it’s part of the reason the market is sceptical of the growth story.

Return on assets is a paltry 3.3% and debt to shareholder equity is 172%.

Finally, what about valuation?

Rentokil trades on a P/E of 26 and forward PE of 20x earnings, which is expensive against a peer average of 15.8. What’s interesting is that if you look at the PE in terms of growth, which is the PEG ratio, you get a very enticing PEG of 0.78. This uses a 5-year EBITDA growth rate of 28.7%. The market is essentially “calling shenanigans” that Rentokil has the stuff to maintain this level of EBITDA and revenue growth. If it does, then the PEG suggests that growth is not priced in.

FCF Yield is fair to middling at 3.38%, and we lock in a 2.2% dividend yield for our patience.

Overall, we have a growth compounder, which has demonstrated a strong history of top and bottom line growth, who is going through major acquisition pains and testing the market’s commitment and resolve to the business. The main worries are the low ROE/ROA, and high debt to shareholder equity ratio. The net income margin needs to improve too.

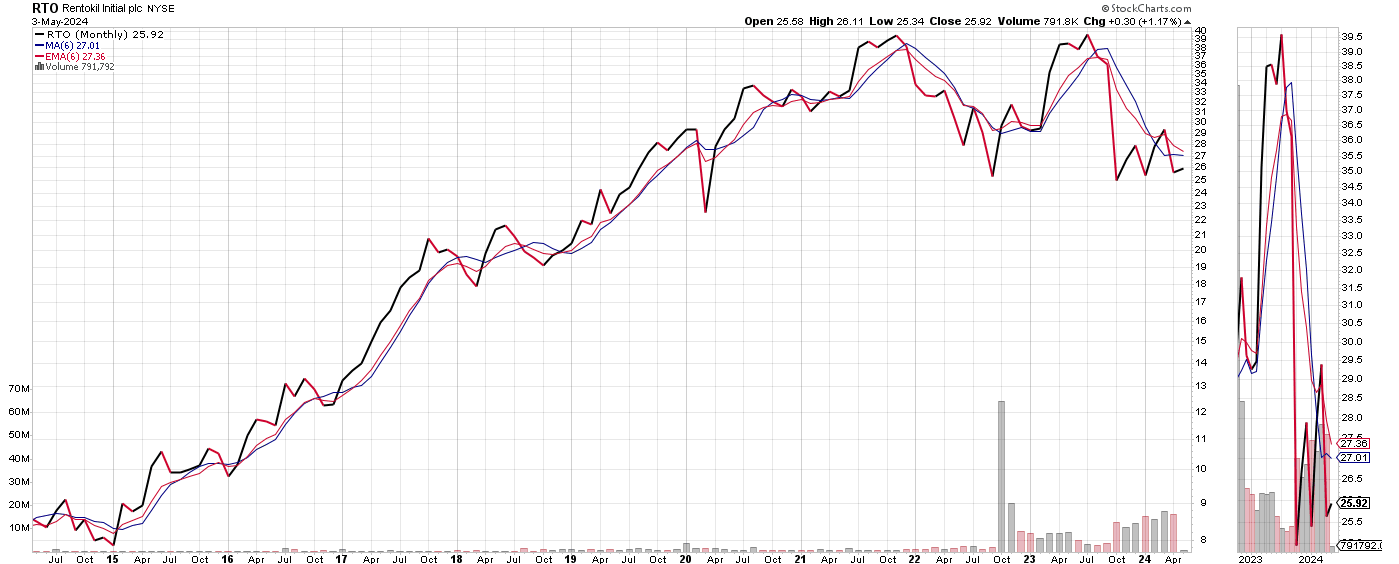

Technicals

Stock Charts

Using the 6-month moving average on a monthly basis, the share price has pierced through support at $27.01. It might be prudent to wait for a bit of upward momentum and consider purchases at or above $27. Rentokil closed at $25.92 on Friday and therefore has a bit of ground to cover.

There is the annual AGM coming shortly next week and that may be a good time to consider a position if we get a positive update.

Overall Assessment

Rentokil is a wide-moat rated business with a significant presence globally in the pest control market.

A lot of ink has been spilled about the Terminix acquisition, but broadly speaking and with a long-term view, it looks like they are having temporary problems that will be hammered out over the next 12-18 months. Long-term investors should take note because Rentokil is likely to move fast when signs emerge that this negative trend is reversing.

From a valuation perspective and looking at the balance sheet, income statement, and cash, flow Rentokil is an average, to perhaps slightly better than average company. The market is right to worry about the issues that they are facing, and it’s not a fundamentally “highly profitable” business.

Overall, I believe Rentokil is a “Hold” until such time that two conditions are met:

- Rentokil begins to trade above key technical levels or shows better price momentum on the 20-day moving average and 50-day moving average

- Rentokil shows signs of an easing with the situation in North America, whether by improved margins in that key segment, or increased revenue

Growth worries are a bit like an oil tanker changing course; you only have to see it shifting in the right direction to know where it is ultimately headed to.

I have taken a small position in the company and will be looking to add on signs of strength and improving business conditions.

{kind=link}