Monty Rakusen

Overview

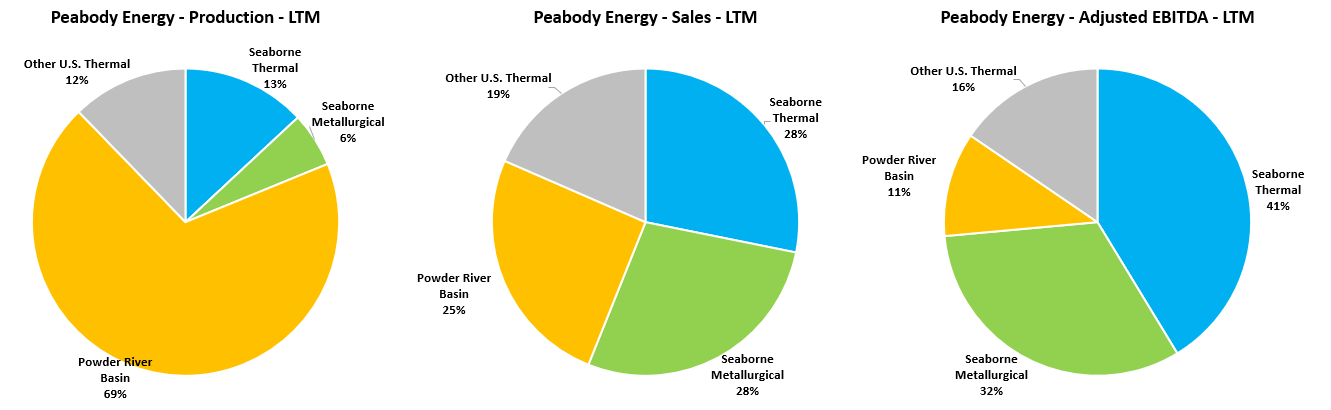

Peabody Energy (NYSE:BTU) is a U.S. coal mining company, with production of thermal coal and metallurgical (“met”) coal. The company operates four different business segments, where most of the adjusted EBITDA normally comes from the seaborne thermal and seaborne met segments, even if the company has a lot of lower-margin production in the Power River Basin.

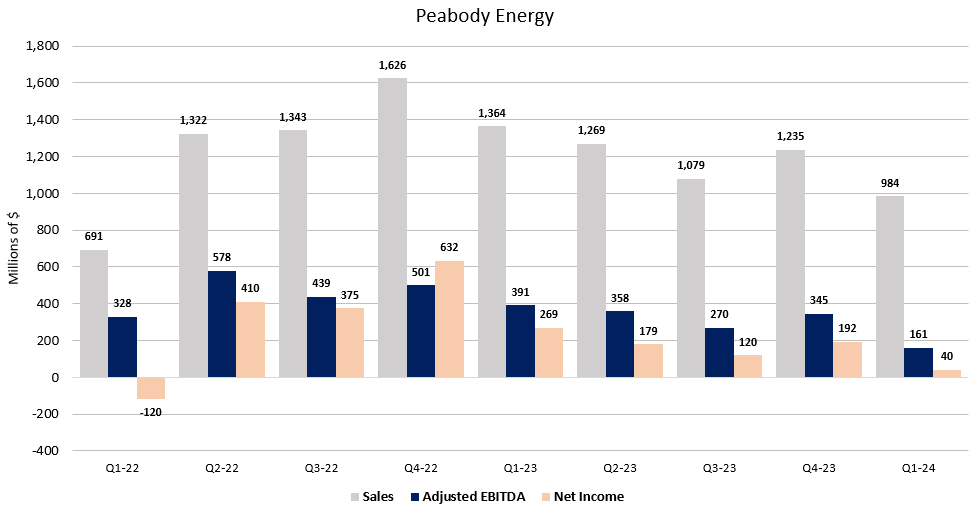

Figure 1 – Source: Peabody Quarterly Reports

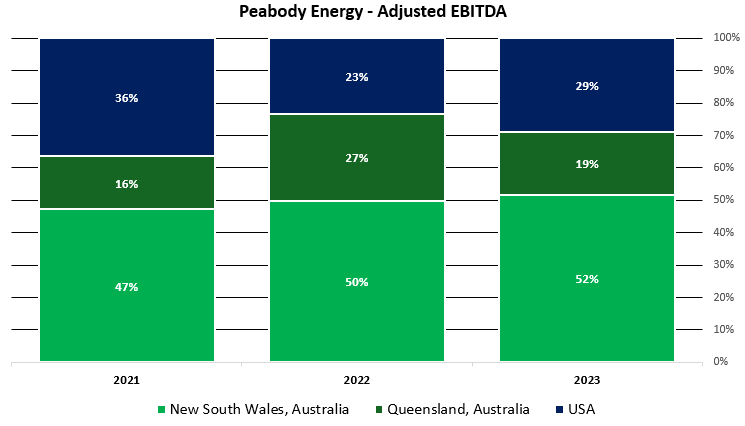

While Peabody is a U.S. domiciled and listed company, the majority of adjusted EBITDA has come from the Australian mines over the last few years.

Figure 2 – Source: Peabody 10Ks

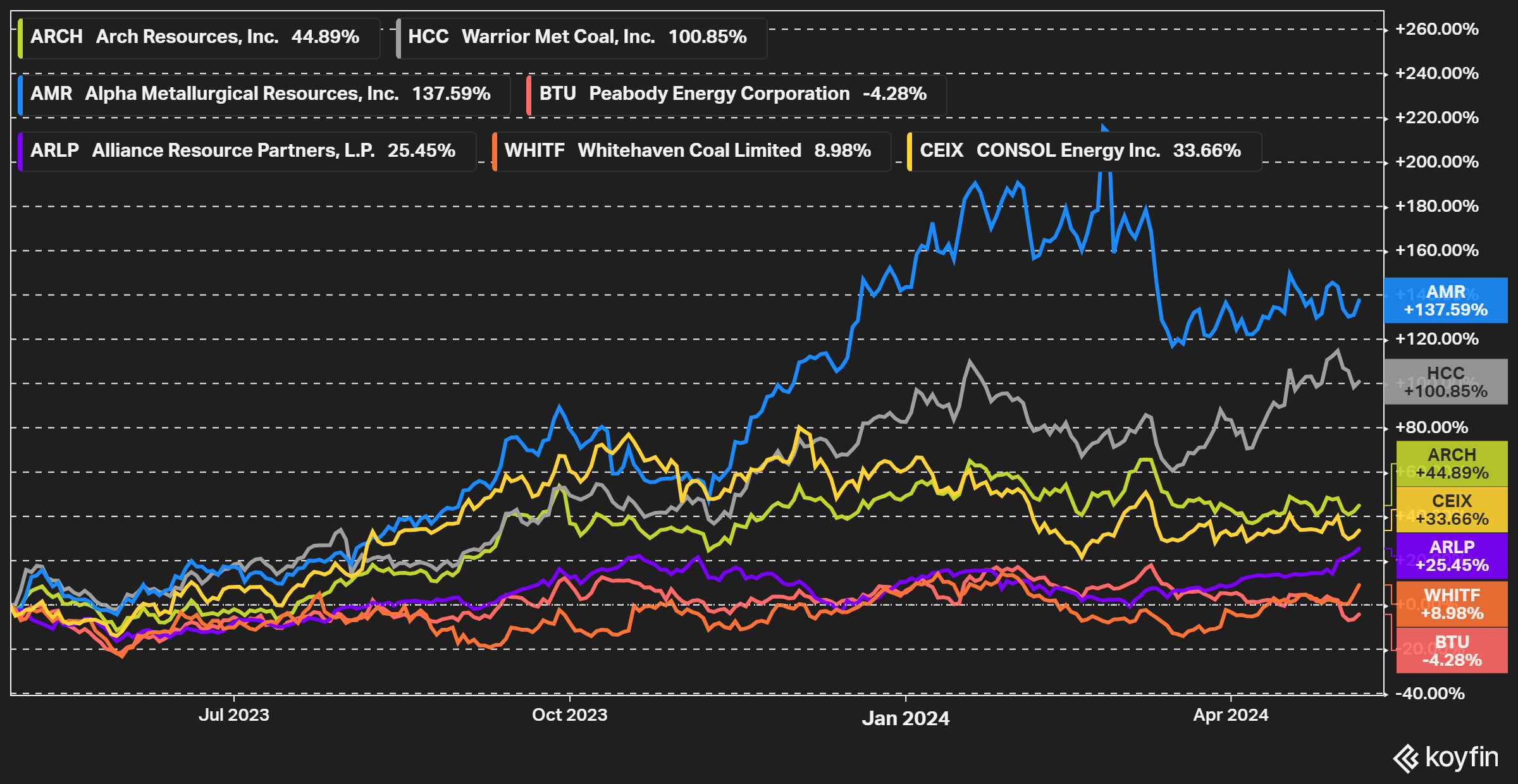

Peabody is a company I have covered earlier this year, and the prior articles can be found here. In this article, I primarily wanted to focus on the Q1 2024 result which was released on the 2nd of May.

Figure 3 – Source: Koyfin

The stock price of Peabody has been marginally negative over the last year, and it has lagged peers by a substantial margin. That the coal miners exclusively focused on met coal have outperformed should not come as a surprise given that thermal coal prices have been weaker than the met coal prices during this period.

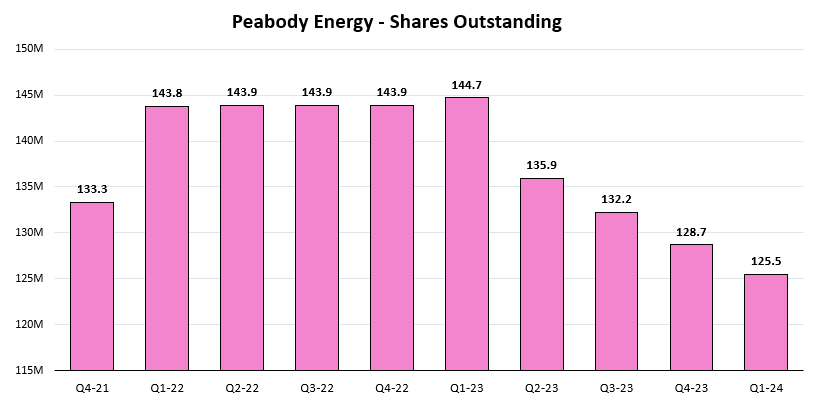

However, Peabody gets around 30-40% of adjusted EBITDA from the seaborne met segment and that number will increase once the Centurion mine starts longwall mining in a couple of years. So, I consider the recent underperformance excessive as Peabody has generated solid cash flows over the last couple of years and distributed much of those cash flows to shareholders, primarily via buybacks. We can in the chart below see that the shares outstanding has decreased by around 13% over the last year.

Figure 4 – Source: Peabody 10Qs & Press Releases

Q1 2024 Result

Peabody did on the 11th of April already flag that the Q1 result would be weaker due to operational issues in the quarter. The company reported an adjusted EBITDA of $161M and a net income of $40M for the first quarter of the year. The figures were much weaker than last quarter or Q1 in 2023.

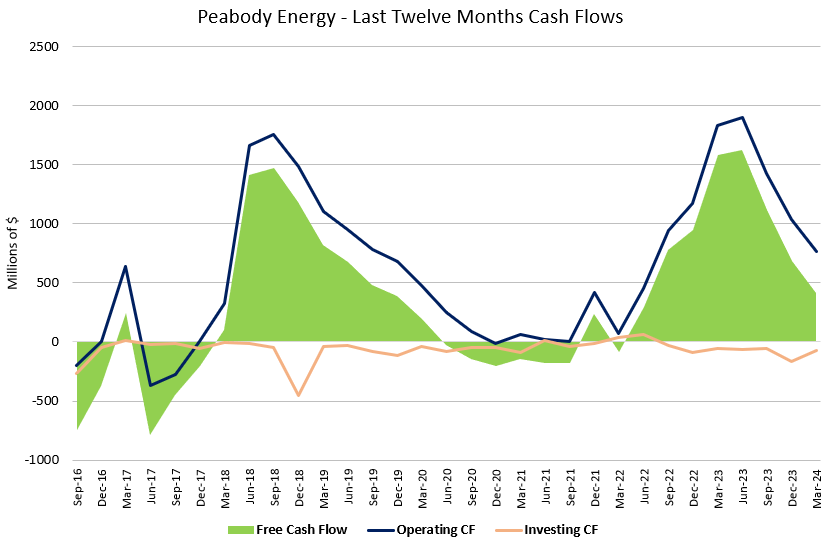

Figure 5 – Source: Peabody Quarterly Reports

Available free cash flow was negative $4M in the most recent quarter, which is down substantially compared to what we have seen over the last couple of years. Management did also on the Q1 2024 conference call indicate that free cash flow will be more muted in Q2 as well due to tax payments and other items, but the second half of the year should generate significantly higher free cash flow.

It was also clarified on the conference call that the capital distributions are based on the annual cash flow, so it will still be possible to see material buybacks in Q2 even if cash flows are expected to be lower in the quarter. Peabody had a net cash position of $838M at the end of Q1, which means there is plenty of liquidity even if that is expected to be used for ramping up the Centurion mine. The company also confirmed that the regular $0.075 per share quarterly dividend will be paid in June.

Figure 6 – Source: Koyfin

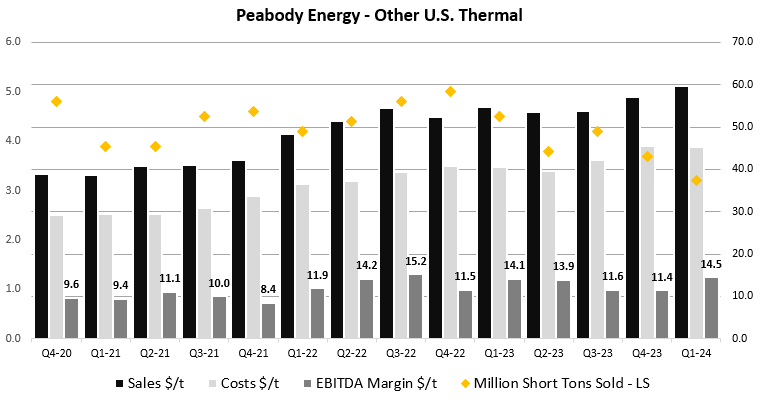

In a quarter-over-quarter comparison, the Other U.S. Thermal segment generated a respectable EBITDA in Q1 due to a higher sales price and an increased margin, even if the production volume declined.

Figure 7 – Source: Peabody Quarterly Reports

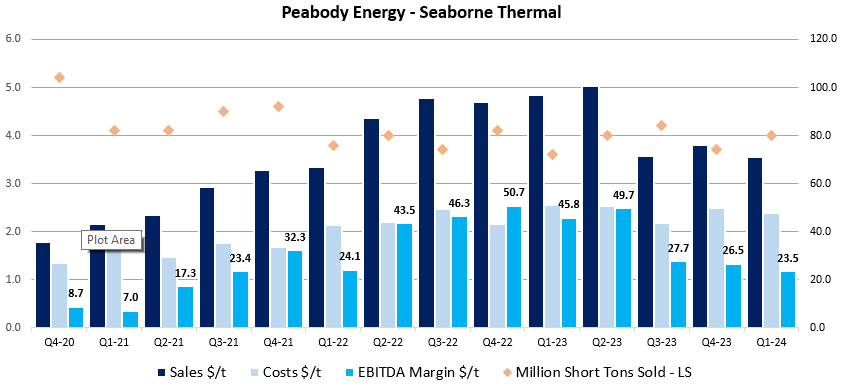

The seaborne thermal segment saw a marginally lower EBITDA compared to Q4 2023, following a lower sales price, which was partly offset by a higher production volume and lower costs.

Figure 8 – Source: Peabody Quarterly Reports

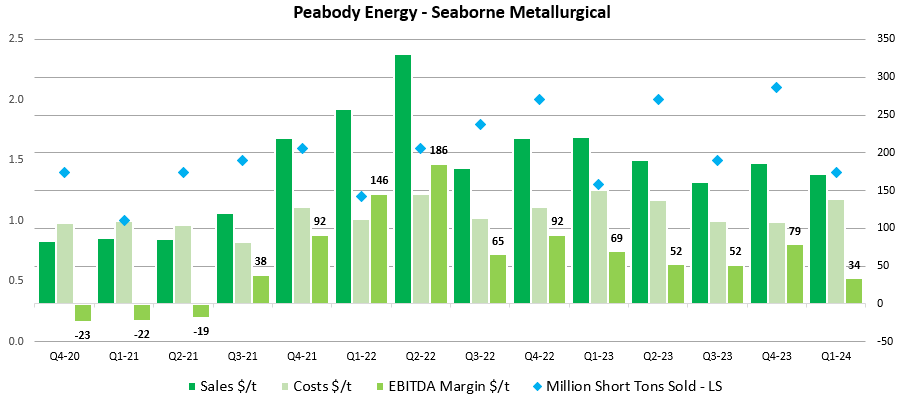

The EBITDA was down significantly in the Power River Basin segment due to lower production and higher costs, which ate into the already small margin in that segment. However, the larger negative impact came from the seaborne met segment, where production declined 33%, the realized sales price dropped 8%, while costs increased 29%. There were a few one-off items in the segment during Q1, but the segment EBITDA to dropped 71% compared to Q4 2023.

Figure 9 – Source: Peabody Quarterly Reports

Valuation & Conclusion

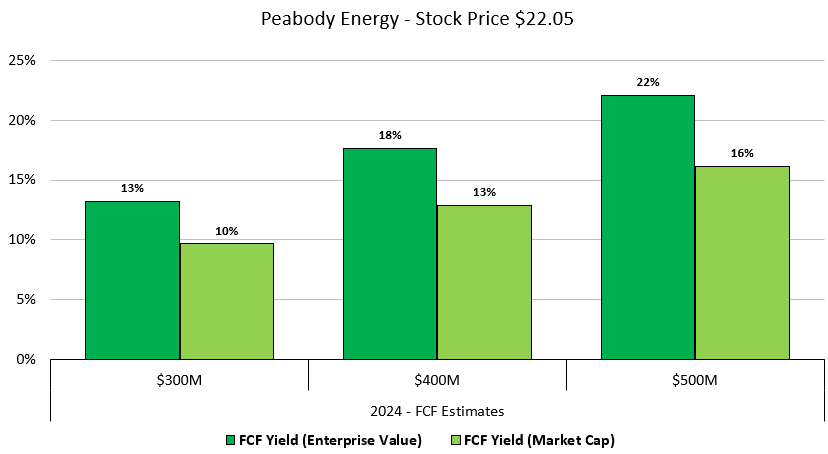

The company has maintained its annual guidance for 2024 but following a weak Q1 and soft cash flow guidance for Q2, there is more uncertainty in my cash flow estimates for 2024. It does to some extend also depend on whether we include growth capex and the Wards Well acquisition, which is adjacent to the Centurion mine complex. If we use relatively conservative coal price assumptions, we are looking somewhere around $300M in free cash flow for 2024.

Figure 10 – Source: My Estimates

A free cash flow of $300M would still indicate a free cash flow yield in the 10-13% range, depending on whether we rely on enterprise value or market cap. That is still an attractive valuation in my view, given that an investment in Peabody is partly an investment based on what the company will look like in a few years once the Centurion mine is up and running, where cash flows from the seaborne met segment are expected to increase a lot.

In an earlier article, I touched in increased royalties for Australian coal production, which has been implemented over the last few years. That is certainly a risk to be aware of for Peabody, but given the recent changes, I would be surprised if we saw another royalty increase so close to the last one.

So, the main risk with an investment in Peabody is probably a delay or substantial cost overrun of the ramp up of the Centurion mine, even if it is worth remembering that Peabody is extremely well-capitalized.

Overall, I consider Peabody a solid buy at this level, especially for investors with the patience to hold the stock for a few years over the ramp up of the Centurion mine.

{kind=link}