littleclie

MSCI (NYSE:MSCI) reported results that were in line with my base case for the company, reaffirming my thesis that the weakness we saw in the business in the first quarter was not the start of a worsening trend, but rather, more of a one-off and short-term occurrence.

Management demonstrated in the quarter that despite the tough market conditions, MSCI continued to grow solidly, form new partnerships and invest in its core and new businesses.

The ESG & climate segment and private assets segment are two promising segments, which are in the early stages for MSCI, and where MSCI has structural advantages on which it can lean on.

While the environment remains difficult and management remains cautious, I am cautiously optimistic that we will see the headwinds from 1Q24 slowly dissipate as the year progresses.

Brief introduction

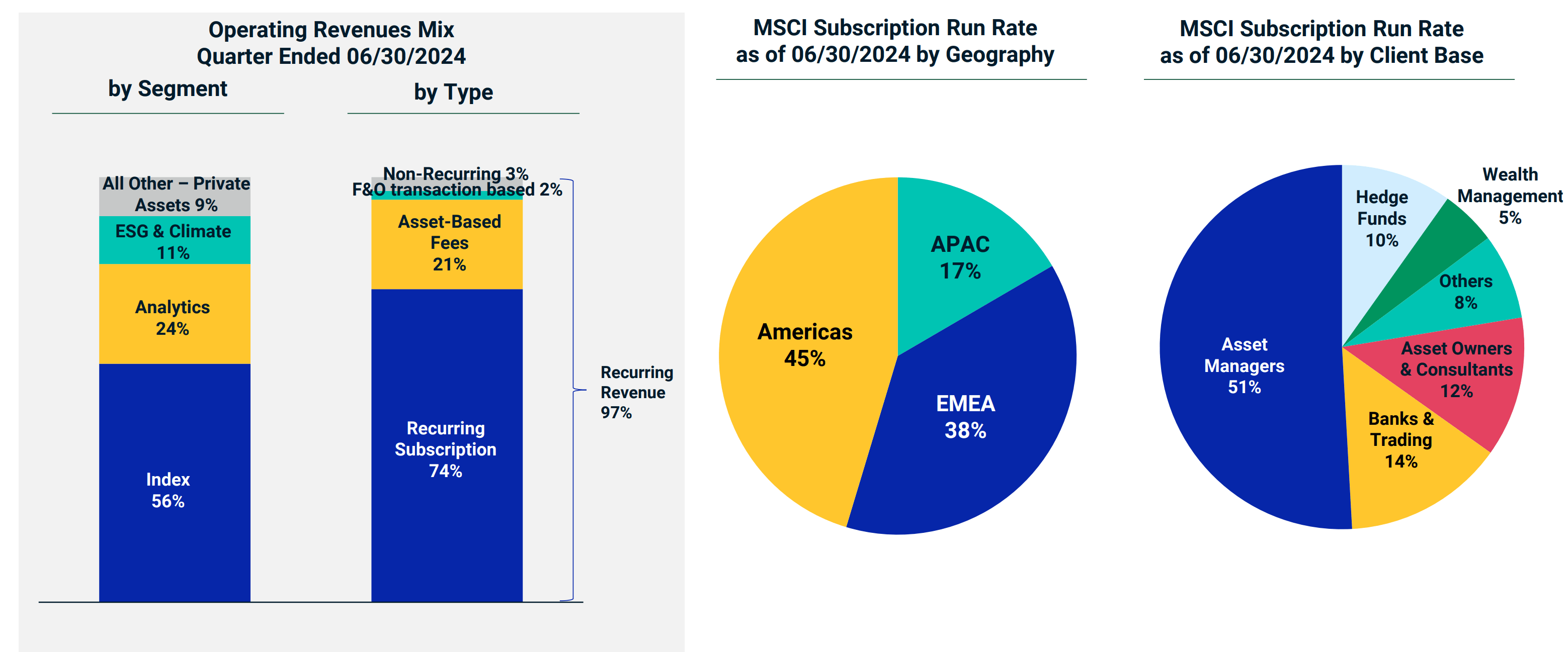

For those who are new to the MSCI story, MSCI has three main segments, the index segment makes up 56% of revenues, analytics segment makes up 24% of revenues and ESG & Climate makes up 11% of revenues.

By client base, asset managers, hedge funds, asset owners and banks have traditionally formed the bulk of its business. MSCI has been focusing on a new group of client segments with strong potential, including insurance companies, wealth managers, general partners, corporates and corporate advisers.

Revenue and client mix (MSCI)

2Q24 results

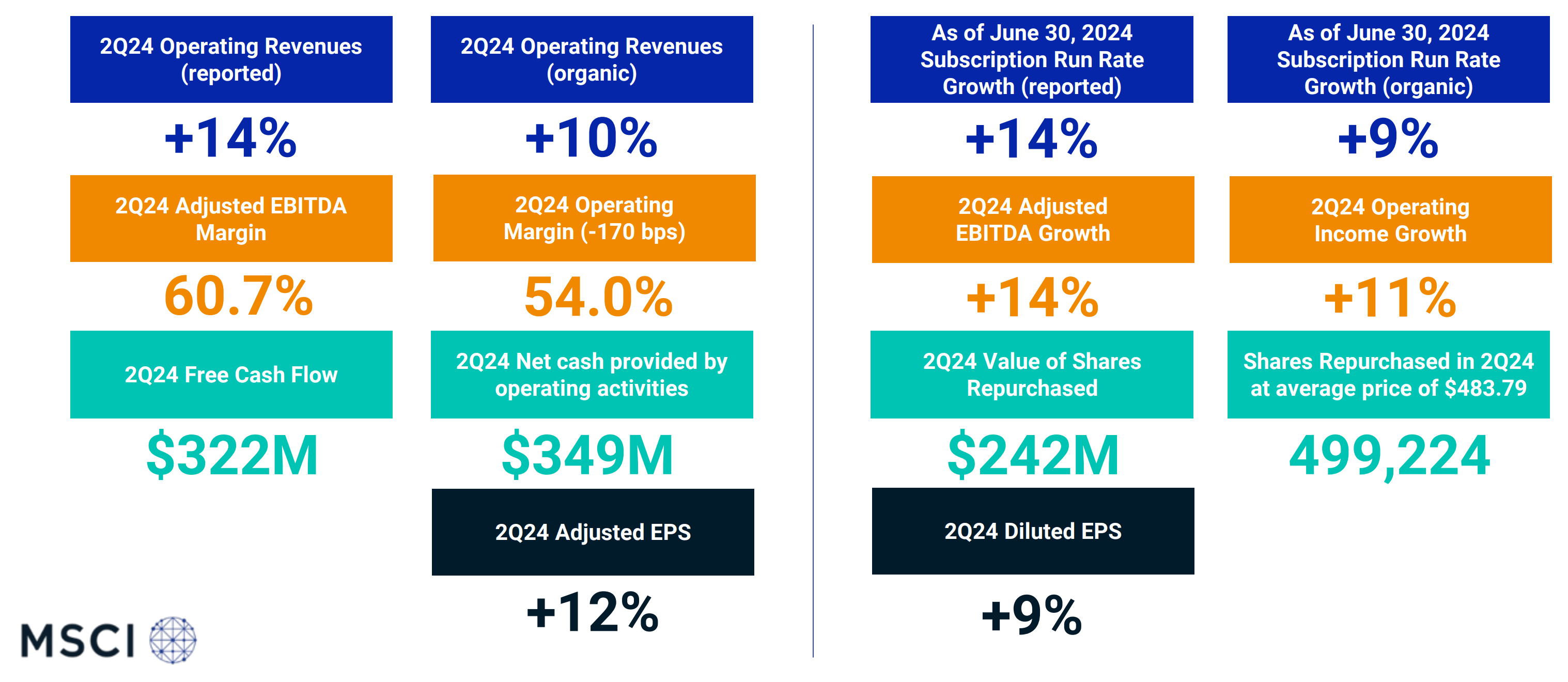

Revenues came in at $708 million, up 14% from the prior year (Beat consensus by 2%).

Operating income came in at $385 million, up 11% from the prior year (Beat consensus by 4%).

EPS came in at $3.64, up 11% from the prior year (Beat consensus by 4%).

Results overview (MSCI)

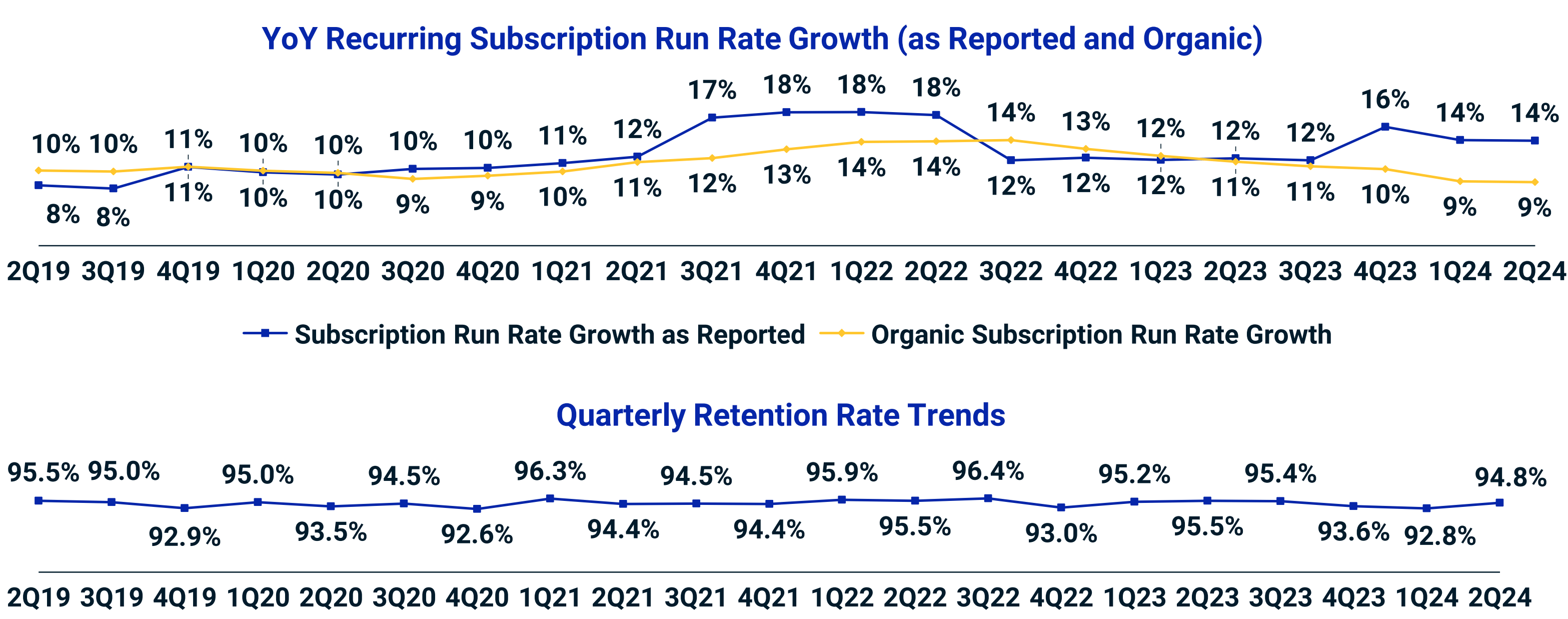

Most importantly, as can be seen below, the retention ratio quickly recovered to 94.8%, which is around its average retention ratio, after the metric fell to 92.8% in 1Q24.

This helped relieve fears that we could see further deterioration after the 1Q24 weakness because retention ratios rebounded immediately as I initially expected.

Run-rate and retention ratio (MSCI)

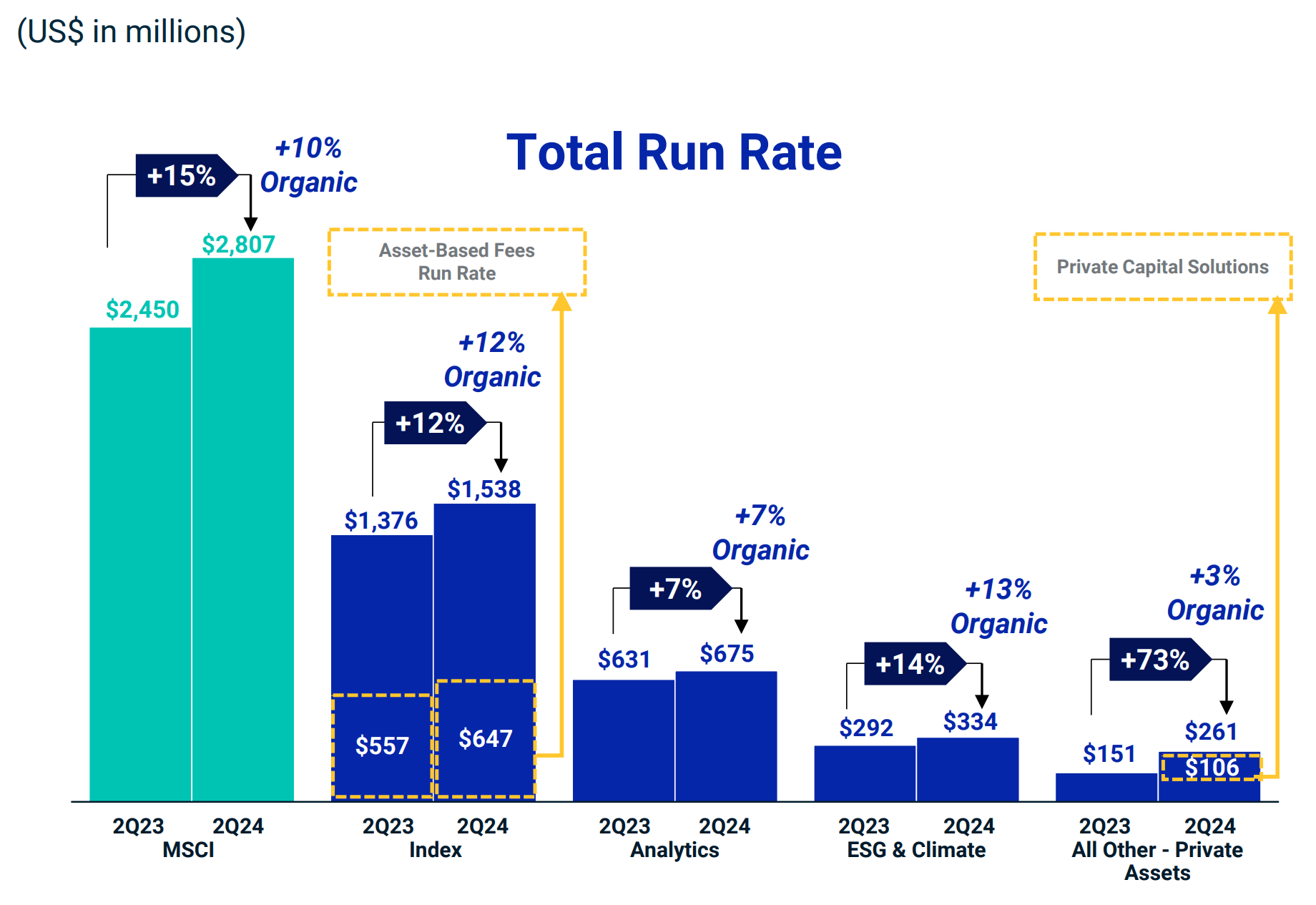

Index segment

The index segment subscription run rate growth came in at 9%.

By geography, both EMEA and APAC contributed 10% growth in subscription rate growth in index.

By client base, the two more significant index client segments which make up 68% of index subscription run rate, asset managers and asset owners, grew at 8% and 12% respectively. The hedge funds and wealth managers segment saw their index subscription run rate grow 24% and 11% respectively.

By products or modules, the custom indexes and special package segment grew 17% from the prior year. In particular, in 2Q24, MSCI helped a large asset manager client launch a new custom ETF climate series linked to the MSCI Transition Aware Select indexes. In addition, MSCI closed the Foxberry acquisition, which will lead to an enhanced custom index platform launch in the second half of 2024.

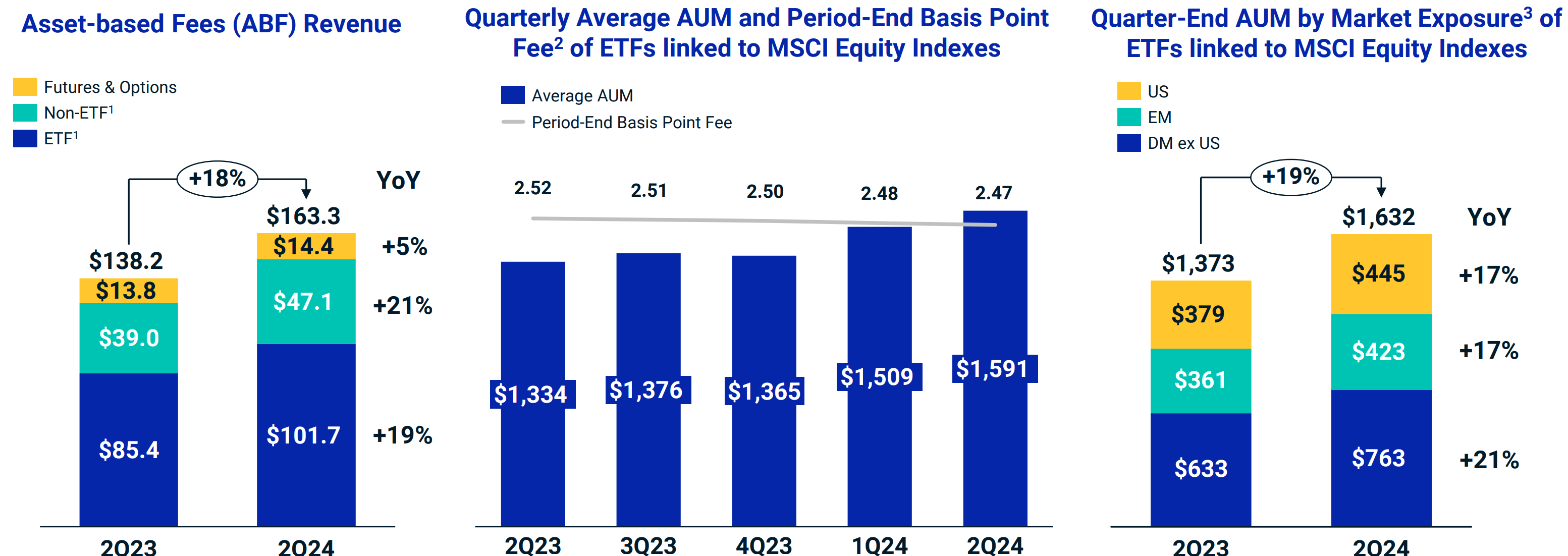

Asset-based fees grew 18% from the prior year, benefiting from an increase in AUM by 19% from the prior year, and in the quarter, MSCI saw $28 billion cash inflows into MSCI-linked equity ETFs and $21 billion in market appreciation in the second quarter.

Index segment metrics (MSCI)

Specifically, ETF products linked to MSCI indexes continue to grow, which strengthened MSCI’s position as a top index for ETF products, with the number of equity ETFs linked to MSCI indexes doubling from the prior year. This brought in $2.5 billion in cash flows and represents almost 30% market share in the new equity ETF fund flows.

Analytics, ESG and Climate and Private Assets

Relative to the size of the index segment, the analytics, ESG & climate, and private assets segments when combined is smaller than the index segment, but they do bring some unique characteristics and diversification to the business model.

Run rate breakdown (MSCI)

First, in the analytics segment, organic subscription run rate growth was 7% and revenue growth for the segment was 11%. Analytics achieved new recurring subscription revenues of more than $21 million, which was the best ever second quarter achieved and also the best ever retention rate for the second quarter of 96%. This performance is a result of a strong quarter with hedge funds, where MSCI’s equity risk models achieved a large win for a new client’s recent fund launch. Almost $4 million in new recurring subscription revenues came from asset owners, which was up 63% from the prior year, as asset owners look to improve their enterprise risk management. In terms of drivers, the strong analytics performance was driven by an environment where its customers are increasingly focusing on investment risk, credit risk and liquidity risks, and MSCI is a leader on these. In addition, another driver is innovation within the analytics segment, which includes delivering risk analytics through visualization and integrating AI capabilities within the business.

Second, in the ESG & climate segment, organic subscription run rate growth was 14% and revenue growth was 12%. There was also a 30% climate run rate growth. Apart from the Moody’s partnership, MSCI continues to launch new products in the ESG & climate segment, with a new data set to help customers align better with corporate sustainability reporting directive in Europe. MSCI also launched the MSCI GeoSpatial Asset Intelligence, which has already led to two signed deals, one of which is with a large private credit general partner. The MSCI GeoSpatial Asset Intelligence product provides customers with AI capabilities that will identify physical and nature-based risks on more than 1 million locations for 70,000 public and private companies. Management shared that the initial client interest has been encouraging.

Third, in the private assets segment, organic subscription run rate growth was 3% and revenue growth was 72%. The strong revenue growth was a result of an acquisition of Burgiss, and excluding the impact of Burgiss, there was a 17% growth in the subscription run rate for private assets. The retention rate for private assets is currently about 93%

Cautiously optimistic

Given that 2Q24 results were encouraging, I am cautiously optimistic about the outlook for MSCI.

In particular, I do think that my base case that the last quarter’s cancellations and weak sales performance were not the start of a deteriorating trend is affirmed.

The fact that we saw solid growth and rebound in retention rates from the prior quarter was a positive, and management also commented that there was no deterioration in the current 2Q24 quarter.

That said, I added the term cautious there because of management commentary.

MSCI continues to expect cancels to be elevated in 3Q24 compared to the prior year and that longer sales cycles continue to persist.

In my view, this is due to two factors. Firstly, after the single client event that resulted in $7 million in cancels as a result of a merger between two major global banks in Europe, while most of that headwind occurred in 1Q24, there are still some near-term market headwinds from that in 3Q24. Secondly, 3Q24 tends to be a seasonally softer quarter for MSCI.

Roughly $7 million worth of cancels came from a single client event, a historic merger of two major global banks in Europe that affected us across index, ESG and analytics

Management saw high levels of client engagement around the world in 2Q24. Clients were interested in new areas of collaboration with MSCI. For example, Moody went into a strategic partnership with MSCI to bring MSCI’s sustainability data and models to Moody’s clients. This is a win-win partnership that not only demonstrates how Moody views MSCI as a leader in ESG, but MSCI also benefits from this as it gets access to Moody’s Orbis, which is a private company database. This is useful for MSCI given it has been focused on getting better data, especially in the ESG and climate space, which can be difficult to obtain, so this partnership benefits MSCI in multiple ways.

In addition, MSCI just launched MSCI private capital closed end fund indices as clients have been requesting for such products and growing investor interest in private markets. There are 130 of such indexes, constructed from a universe of private capital funds with more than $11 trillion in capitalization. This includes all kinds of private assets, like private equity, private credit, private infrastructure, amongst others.

This is an interesting new opportunity for MSCI to focus on, where MSCI is uniquely positioned to address this market and able to address the technical challenges that others may not be able to. The first one is the $15 trillion of underlying data across all private assets, with $11 trillion used to build the 130 indexes announced above, and $4 trillion for its other real asset indices. MSCI has the largest and highest quality data across all players, which is a huge advantage. The second one is the understanding and capability to understand the investment process and metrologies to create indices, where MSCI obviously has spent decades to build. The last one is the distribution, where MSCI once again has a large client base of asset owners and managers.

Lastly, as there is growing client interest in utilization of AI technologies, MSCI launched the MSCI AI Portfolio Insights tool, which is a new risk product suite that combines generative AI with advanced analytical tools and modeling capabilities to help customers identify risks.

Management sees that AI can be implemented in the business to improve cost efficiencies and enhance revenues. MSCI is seeing some attractive economics in terms of how AI can be deployed within MSCI to drive cost efficiencies, and this will be embedded into the budgeting for 2025 in particular. MSCI has also seen how AI can help with new product development across different segments and businesses.

I think that strong client engagement around the world and across client segments, along with positive momentum in the equity markets, should lead to momentum in the sales front.

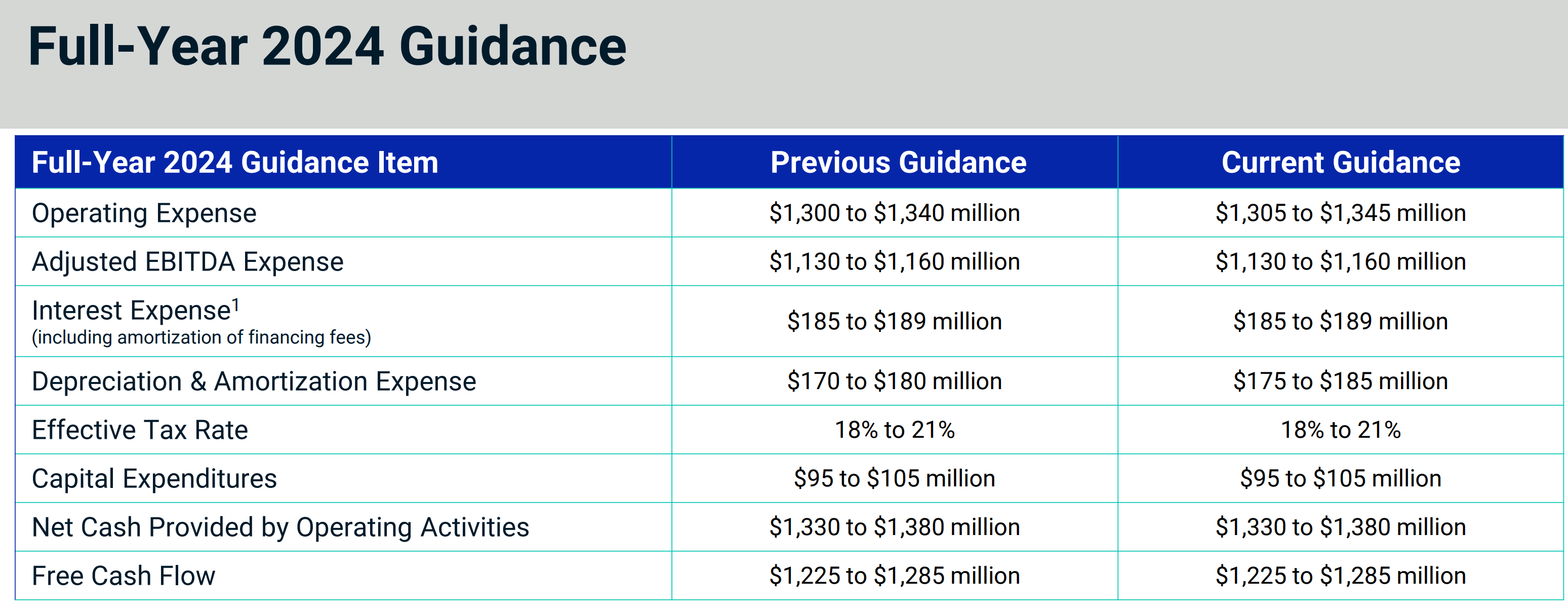

On the guidance front, MSCI reiterated most of the 2024 guidance, with the exception of a less than 0.5% increase in operating expenses coming from slightly higher D&A. This increase came from an acquired intangible amortization expense from the Foxberry acquisition, which was closed in April.

2024 guidance (MSCI)

Valuation

The 2Q24 results were a confirmation of my model, with just a modest revision to the operating expenses line.

One thing that I had to adjust the model for was the significant share buybacks that MSCI was doing, which resulted in EPS being revised higher due to the lower share count.

There was a 2% reduction in share count since the prior quarter, and I assume a modest 1% reduction in share count each year (MSCI reduced share count by 1.5% each year on average since 2019).

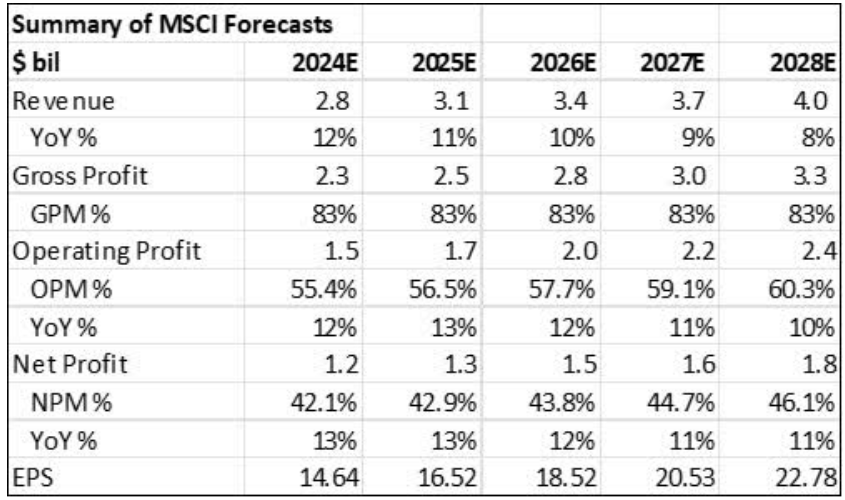

As such, my MSCI 5-year forecasts as shown below. I forecast MSCI’s EPS CAGR to be 11% over the 5-year period, which is based on assumptions that the cancellation rates do not worsen from here and that the macro and market environment remains stable, with continued efficiency improvements in the business driving operating margin expansion, as shown below:

Summary of my 5-year financial forecasts for MSCI (Author generated)

My intrinsic value for MSCI is $627, again using the discounted cash flow model and assuming the 40x terminal multiple and 11% cost of equity. The 40x terminal multiple is reasonable here, given that in the past five years, MSCI’s 5-year average P/E is 52x. When I excluded MSCI’s abnormal P/E of 71x in 2021, the 5-year average P/E goes down to 46x. In addition, it has a 10-year average P/E of 42x. As a result, I think that 40x 2028 P/E is fair for the company based on historical valuations, continued leadership in the space, and a highly attractive business model with high retention rates and recurring revenues.

My 1-year and 3-year price targets are $678 and $859 respectively, which imply 40x 2025 and 2027 P/E. Again, I think these multiples are reasonable given what was mentioned above.

Conclusion

As I have suggested multiple times in the article, I think that the 2Q24 earnings for MSCI should help relieve fears about worsening fundamentals.

Despite a tough operating environment, MSCI continues to excel as the market leader and demonstrate the quality of its business model.

The new businesses in which it is investing in should drive incremental growth in the future, while its leadership in its core index business continues to shine.

As we move past the headwinds that we saw in 1Q24, and as the environment becomes a more favorable one for MSCI, we will likely see the company’s investments in innovation and new products deliver sustainable long-term growth for the company.

{kind=link}