Jonathan Kitchen/DigitalVision via Getty Images

IHH Healthcare Berhad (OTCPK:IHHHF) [IHH:MK] stock is now assigned a Buy investment rating. IHH Healthcare’s 1H 2024 results beat expectations, and I see the company’s shares trading higher with multiple expansion driven by a positive growth outlook. The company’s major growth engines are a more favorable mix of procedures and an increase in bed capacity.

My previous October 2, 2020 write-up looked at IHHHF’s weak Q2 2020 results and the prospects of a turnaround in the second half of the year.

The company’s shares are traded on Malaysia’s stock exchange Bursa Malaysia and the Over-The-Counter market. IHH Healthcare’s OTC shares have low trading liquidity, but its Malaysia-listed shares boasted a three-month average daily trading value of $7 million as per S&P Capital IQ data. Investors can deal in IHH Healthcare’s liquid Malaysian shares with international brokers such as Hong Kong’s Monex Boom Securities and Singapore’s OCBC Securities.

IHHHF Reported Above-Expectations 1H Results Due To A Favorable Procedure Mix

On its corporate website, IHH Healthcare describes itself one of the world’s largest private healthcare groups” operating “over 80 hospitals in 10 countries.”

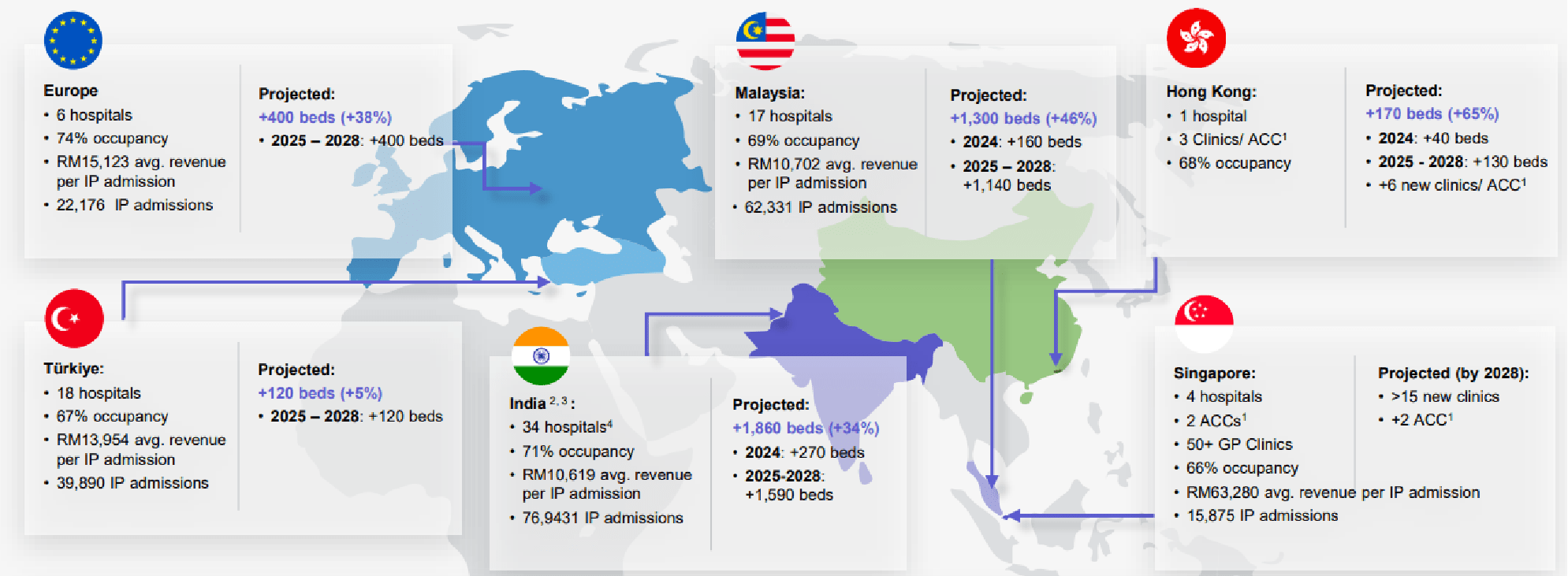

IHHHF’s International Network Of Hospitals

IHH Healthcare’s Investor Presentation Slides

Top line and EBITDA for IHH Healthcare expanded significantly by +23% YoY and +26% to RM 12,048 million and RM 2,748 million, respectively for the first half of this year. IHHHF had revealed its financial performance for the 2024 interim period with its results announcement issued on August 29.

Prior to the release of the company’s 1H 2024 results, the sell-side analysts’ consensus FY 2024 top line and EBITDA forecasts for IHHHF were RM 22,524 million and RM 5,075 million, respectively according to S&P Capital IQ’s consensus data. In other words, IHH Healthcare’s actual 1H 2024 revenue and EBITDA represented 53% and 54% of the respective consensus estimates. This means that the company’s 2024 interim results had exceeded expectations.

IHHHF indicated at the company’s 1H 2024 analyst call (transcript sourced from S&P Capital IQ) that its good interim performance was driven by “higher (revenue) intensity across all our key markets” achieved by “doing higher technology, higher equity procedures.”

The key measure of revenue intensity for IHH Healthcare is the amount of revenue divided by the number of inpatient admissions. Specifically, IHHHF’s revenue generated per impatient admission grew by +17%, +10%, and +9% for the Singapore, India, and Malaysia geographical markets, respectively in 1H 2024.

In its 1H 2024 results presentation slides, IHHHF noted that its hospitals in Singapore, India, and Malaysia benefited from “improving case mix”, “more complex cases”, and “complex treatments”, respectively. It is natural for the company’s revenue on a per-admission basis to rise, when it sees an increase in the number of procedures that are more challenging and involve higher costs. As an example, “proton beam therapy” is about three times as expensive as “conventional radiotherapy” as per IHH Healthcare’s 1H 2024 results briefing comments. Therefore, IHHHF’s financial performance gets better assuming that the company continues to benefit from a rising revenue contribution from higher-quality procedures (e.g. “proton beam therapy” etc) priced at a premium.

At its 2024 interim analyst briefing, IHH Healthcare mentioned that it has seen “signs of (high revenue intensity) sustaining over the (full) year” based on what it has observed in early-2H 2024. This suggests that there is a reasonably good chance of IHHHF performing well in the near future as the company’s mix of procedures remains favorable as per its disclosures.

Growth Prospects Are Strong With Capacity Expansion Plans

IHH Healthcare operated hospitals with a total of over 12,000 beds as of June 30, 2024, and a meaningful increase in bed capacity will be supportive of the company’s growth in the medium term.

In specific terms, IHHHF has set a goal of expanding its capacity by an additional 4,000 beds in the time frame between 2024 and 2028. This implies that the company’s hospital bed capacity has the potential to grow by a third in the coming five-year period.

Approximately 40% and 29% of the planned 4,000 new bed additions will be in the Indian and Malaysian markets, respectively as indicated in IHH Healthcare’s interim results presentation slides. In my opinion, IHHHF has made the right decision to pick India and Malaysia as the key markets for capacity expansion.

According to the latest data available from the World Bank, the annual healthcare spending on a per-capita basis for Singapore, Malaysia, and India was approximately $3,970, $487, and $74, respectively. It will be reasonable to think there is room for healthcare spending in Malaysia and India to grow in the years ahead and narrow the gap with other more developed Asian healthcare markets like Singapore.

I think the market has yet to factor in the positive growth outlook for IHH Healthcare into its valuations. As per S&P Capital IQ data, the company’s consensus FY 2023-2025 normalized EPS CAGR estimate is a strong +27%. This is supported by its capacity expansion plans and the procedure mix improvement mentioned in the previous section.

An average listed company is usually deemed to be fairly valued at a Price-to-Earnings Growth PEG ratio of 1 times. Considering that IHH Healthcare is a leading hospital operator with exposure to Asian healthcare markets with good growth potential, my view is that IHH Healthcare deserves to trade at a higher PEG than the average stock. A premium of 15% implying a PEG metric of 1.15 times will be appropriate in my opinion.

IHH Healthcare’s current PEG ratio is 0.85 times based on its consensus next twelve months’ normalized P/E metric of 23 times and the FY 2023-2025 bottom line CAGR forecast of +27%. A target PEG ratio of 1.15 times will translate into a capital appreciation potential of around +35%.

Variant View

There are two key risks to consider before investing in IHH Healthcare.

One risk factor is that IHHHF’s case mix turns unfavorable, assuming that a fewer number of complex procedures are done going forward.

The other risk factor is that IHH Healthcare increases its bed capacity by less than the 4,000 beds that it has targeted by 2028.

Conclusion

IHH Healthcare’s rating is upgraded from a Hold previously to a Buy now. The company’s financial performance for the 2024 interim period was better than expected, and its growth prospects are strong.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}