carterdayne/iStock Unreleased via Getty Images

Overview

In my last article on HSBC (NYSE:HSBC) in Feb 2024, I had rated the stock as a buy, with a 28% upside potential and a fair value of $50 / share. The company recently released its Q1 earnings on 30 April, and the stock price jumped by ~5% last week- with majority of the gains occurring post the earnings release. Since my last recommendation, the stock has already gained over 10% in 3 months (vs. 3.24% for S&P 500).

In this article, I evaluate the latest earnings release in more detail and try to evaluate whether the fair market value of the company has changed, and whether it is still a Buy.

Q1 YoY earnings fell, but guidance for the year remains unchanged

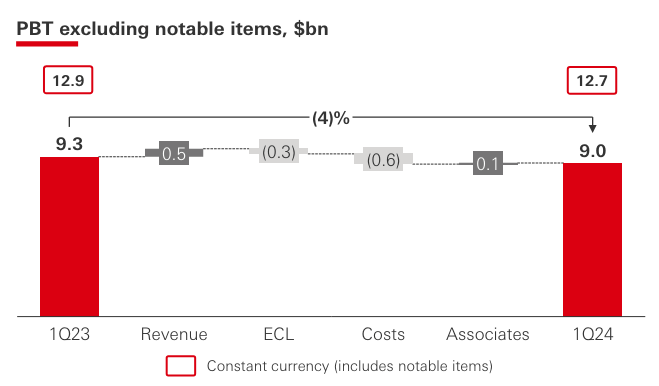

The Q1 24 PBT was $12.7 Bn (-2% YoY), however after excluding notable items the PBT was +9.0 Bn (-4% YoY). In my opinion, this is not very encouraging because the reduction in PBT is driven by increasing Expected Credit Losses – i.e. ECL and overhead costs (figure 1).

Figure 1: PBT Drivers YoY (Investor presentations)

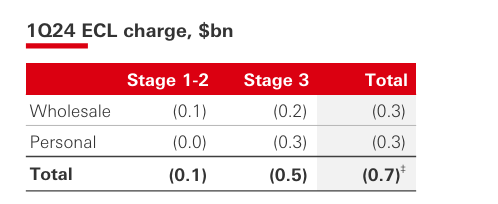

In my view, the data around ECL is not very inspiring and reflects potential stress signs going ahead. Particularly, the majority of ECL is driven by Stage 3 balances, which have a higher likelihood of default. Additionally, these are driven by the wholesale segment currently (figure 2). While the Bank has maintained that Personal segment ECL are stable QoQ (and has reflected this trend in the annual guidance), I believe there is a risk of these costs increasing if the Fed keeps rates higher for longer (as per the latest FOMC meeting) and in case the economy heads towards a mild recession.

Figure 2: ECL Drivers (Investor Presentations)

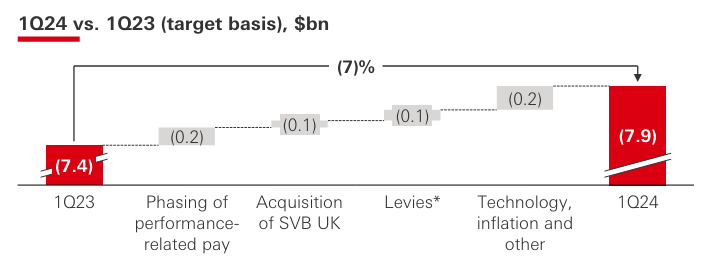

Additionally, the bank reported a 7% YoY increase in costs, driven primarily by (i) Phasing of accrual for performance related pay vs. 2023 and (ii) Tech, inflation & Other costs (Figure 3). The current yearly guidance stays at a 5% increase in costs vs. FY 23, and is significantly higher than the 3% guidance provided earlier. Moreover, I believe that even this might be tough to achieve given that the bank is investing heavily in new tech and inflation is proving to be stickier than expected.

Figure 3: Cost Drivers (Investor presentations)

All in all, I believe that the Quarterly results of HSBC were not very inspiring. However, the stock has seen a massive rally due to the aggressive buyback and dividend announced by the management.

Share buyback

During the earnings release, HSBC announced ~$8.8Bn worth of distributions. This included (i) Interim dividend of $0.1/ share; (ii) Special dividend of $0.21/share and (iii) a new share buy-back of up to $3bn. The special dividend is linked to the sale of the HSBC banking business in Canada to Royal Bank of Canada. While this boosts the dividend yield for investors, there are questions on how sustainable the current dividends are, given the missed quarterly profit expectations.

Nevertheless, I believe that these buybacks and dividends are good news for the existing shareholders in the short term, and have helped bolster the stock price post the earnings.

CEO Noel Quinn Resigns

Another important development that came out of the recent earnings call was that the current CEO of HSBC, Noel Quinn, who has been the CEO since 2019, has now decided to resign. Quinn had been a veteran at HSBC for over 37 years and has been the CEO since the last five years. The banks’ share-prices have risen 30% since Quinn joined as the CEO, and he was instrumental in navigating the bank through the critical COVID crisis and a massive lending crisis in China. While his resignation certainly came as a surprise, it is not alarming negative news. Quinn has said that he will continue to be at the helm of HSBC until he finds a successor, which is most likely expected to happen by the end of the year. In his resignation letter, he stated that he is resigning due to personal reasons and wants to strike a better balance between his personal and professional life. I believe this is not super surprising given that he has already spent a large part of his career at HSBC, and it is now likely time for younger blood to take over.

Geopolitical risks are expected to act as a headwind

As stated in my previous article, HSBC has very high exposure to the international banking segment outside the US. As per the annual report, the majority (>60%) of its exposure is in Hong Kong, Europe and the Middle East. With the US-China relations not showing any signs of getting better, the banks’ massive exposure to China is expected to be a sign of concern. HSBC has substantial positions in the real estate sector of China, which is currently under a massive duress, with home prices falling further in 2024. While the company did not report any increased ECL due to its exposure in China in this quarter, I believe this might begin to change over the coming quarters as the Fed is not showing any signs of cutting the interest rates very soon (and higher interest rates are expected to exacerbate the real estate crisis globally). Moreover, the situation in the Middle East is also not showing many signs of getting better, with Israel threatening to attack Rafah and other countries like Iran getting involved in the war. Everything is not rosy even for the most stable country in the region, i.e. Saudi Arabia- which is showing signs of a slowdown by potentially reducing its investment in multiple Vision 2030 infrastructure projects.

In my opinion, data over the last couple of months has demonstrated that the Middle East war might get dragged for longer than previously anticipated. Similarly, a potential recession in China has also increased in probability with the high interest rate situation. Given that any bad news on these fronts are likely to significantly enhance the risk exposure of HSBC, I believe it is preferred to not build significant new positions in the stock at the current time and price.

Valuation Update

One of the most credible valuation metrics for banks is the price to book ratio. Currently, the PB of HSBC has reached near 5 Year highs, around 0.88. For mature financial firms like HSBC, a PB ratio of 1 is justified, indicating that the stock markets are valuing the common stock equivalent to the market value of Assets less liabilities. Even though the PB ratio is still below 1 (indicating some upside potential) it is presently nearing the 5-year high – indicating limited upside potential.

Figure 4: Historic PB ratio (Tradingview)

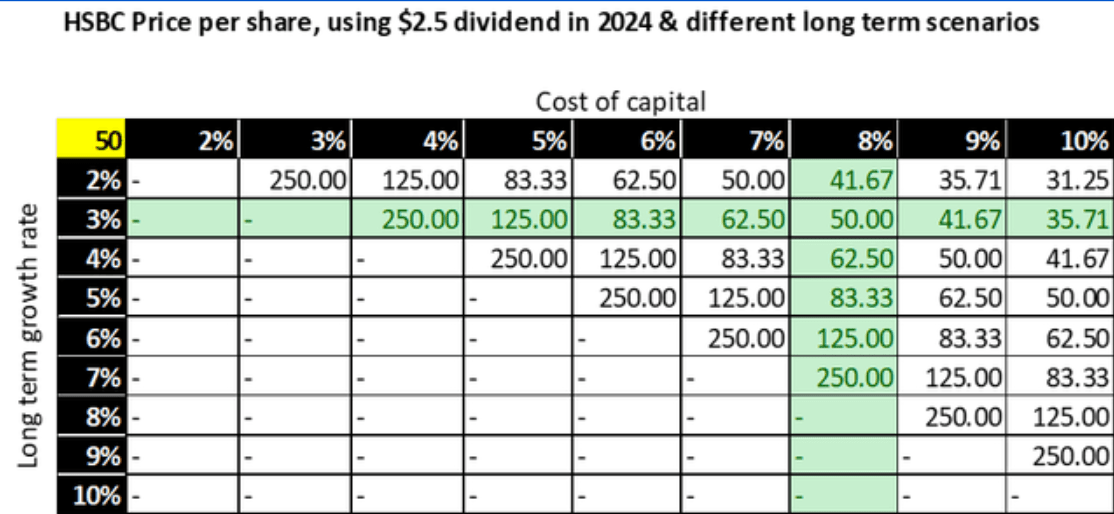

Even using other metrics, such as a Dividend discounting with different growth and cost of capital scenarios, I believe that the fair market value of HSBC still should be around $50 price as per my previous rating. I say that because the base case dividend and long-term growth scenarios for HSBC do not materially change after this earnings call. However, given that the stock price has increased significantly after the quarterly results, I see limited upside potential for any buyers wishing to initiate new positions in HSBC.

Figure 5: Fair Value sensitivity (Analysts estimates)

Last, but not the least, the price increases at HSBC have been higher than the rest of the banking industry during the last 3 months, with HSBC rising by >17% and S&P Bank ETF (KBE) increasing only by ~6%. Given this information, I believe there is limited upside potential for investors willing to take new positions in HSBC.

Figure 6: Stock price trends HSBC vs KBE (Tradingview)

Conclusion

As a conclusion, I believe that while HSBC is a strong company with decent fundamentals, I see very limited tailwinds in the near future that are likely to drive significant value for investors entering the stock at this point. Most of the good news in the stock, including its dividend yield, has largely been priced in after the quarterly results. Any potential bad news, particularly related to geopolitical risks or increasing cost beyond analyst estimates, are likely to lead to a reduction in stock price during the short/mid-term. Even on a long-term value basis, the stocks’ fair value is expected to be around $50 which does not represent a significant upside from the current levels (~13% upside).

Hence, I rate the stock as hold and would recommend new investors avoid creating fresh positions in the stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}