SeanShot

Introduction

I have good news!

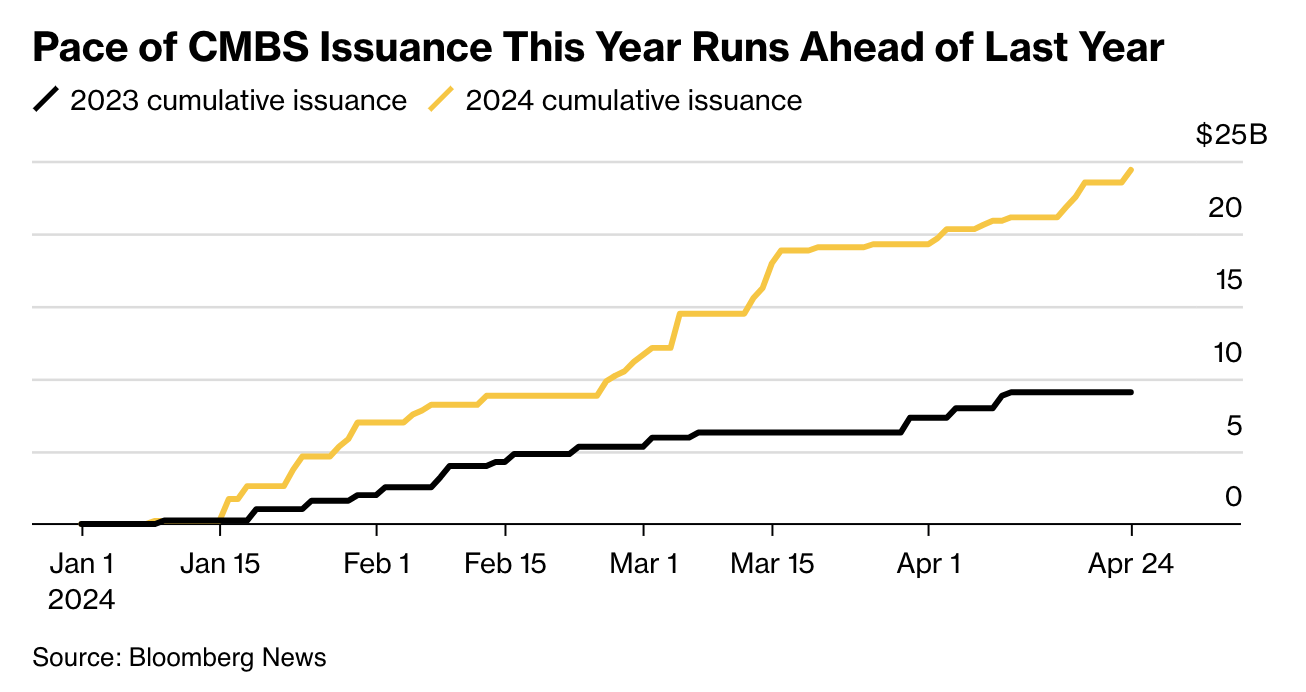

Bloomberg reported that commercial real estate debt is making a comeback.

Investors have bought close to $25 billion of new commercial mortgage-backed securities so far this year. That’s 170% more compared to the same period in 2023.

Last year, CMBS issuance suffered from the bankruptcies of smaller regional banks, a steep uptrend in interest rates, and a halt in commercial property demand. Now, some of these headwinds are fading – despite no signs of a sudden decline in interest rates.

Bloomberg

Two paragraphs from the article stood out (emphasis added):

“Borrowers have been holding out for an opportunity to refinance debt with short-term maturities and now they’re seizing on lower spreads to do it,” said Raviv Shtaingos, head of structured credit at ORIX Corporation USA.

[…] “People have been listening to the Fed and looking at economic data and concluding, ‘Rates are coming down or stabilizing, now is a good time to do deals,’” said Paul Staples, a trader at Academy Securities Inc.

I’m bringing all of this up because it’s time to discuss S&P Global (NYSE:SPGI).

The company is the world’s largest rating agency, which makes developments in the credit market so important. It’s also a company that increasingly uses its data to create value-adding products and services, allowing it to rapidly grow revenue with a fantastic high-margin profile.

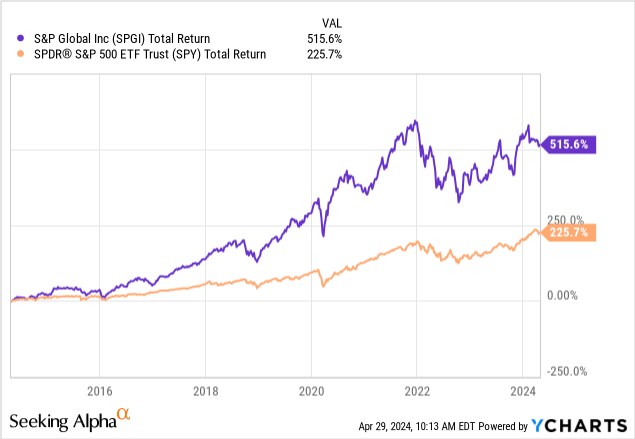

As a result, SPGI shares have returned 516% over the past ten years, beating the fantastic 226% return of the S&P 500 by a wide margin.

My most recent article on the company was written on December 18, when I called the company “One of the most impressive financial stocks” in the title.

Since then, shares are down 4%, lagging behind the market’s 8% return.

As I wrote in that article, short-term weakness was not unexpected – and a thing I’m embracing.

As I believe that the market has gone a bit too far, I am expecting to get a 10% to 15% correction opportunity next year, which I may use to add another top-tier financial stock to my portfolio.

In this article, I’ll update my thesis using the company’s latest earnings and explain what makes this rating powerhouse such a special company.

So, let’s dive into the details!

High-Margin Growth With A Strong Tailwind

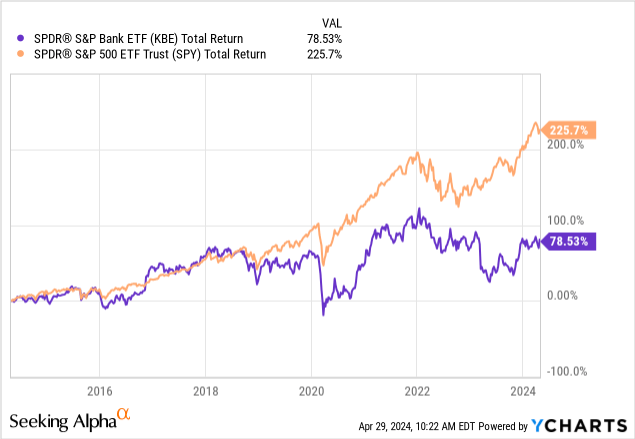

In general, I’m not a fan of the financial sector. In my honest opinion, too many companies in this sector have no moats.

Banks, for example, operate in a highly competitive industry with low entry barriers and a horrible risk/reward picture that comes with steep declines during recessions. The same goes for a range of other lenders and related businesses.

As much as I like buying good banks after a serious stock price decline, the long-term risk/reward tends to be poor. The chart below supports this thesis.

I want businesses with wide-moat business models, which allow these companies to grow on a consistent basis and offer services that are critical for the modern financial sector.

This includes stock exchange operations (which I love!), data providers, and rating agencies like S&P Global that have found ways to grow beyond their traditional rating services.

The company also generates most of its revenues from recurring sources, which adds a lot of stability and earnings visibility.

S&P Global

With that said, S&P Global is currently benefitting from stronger tailwinds, which is why I started this article by shedding some light on CMBS demand.

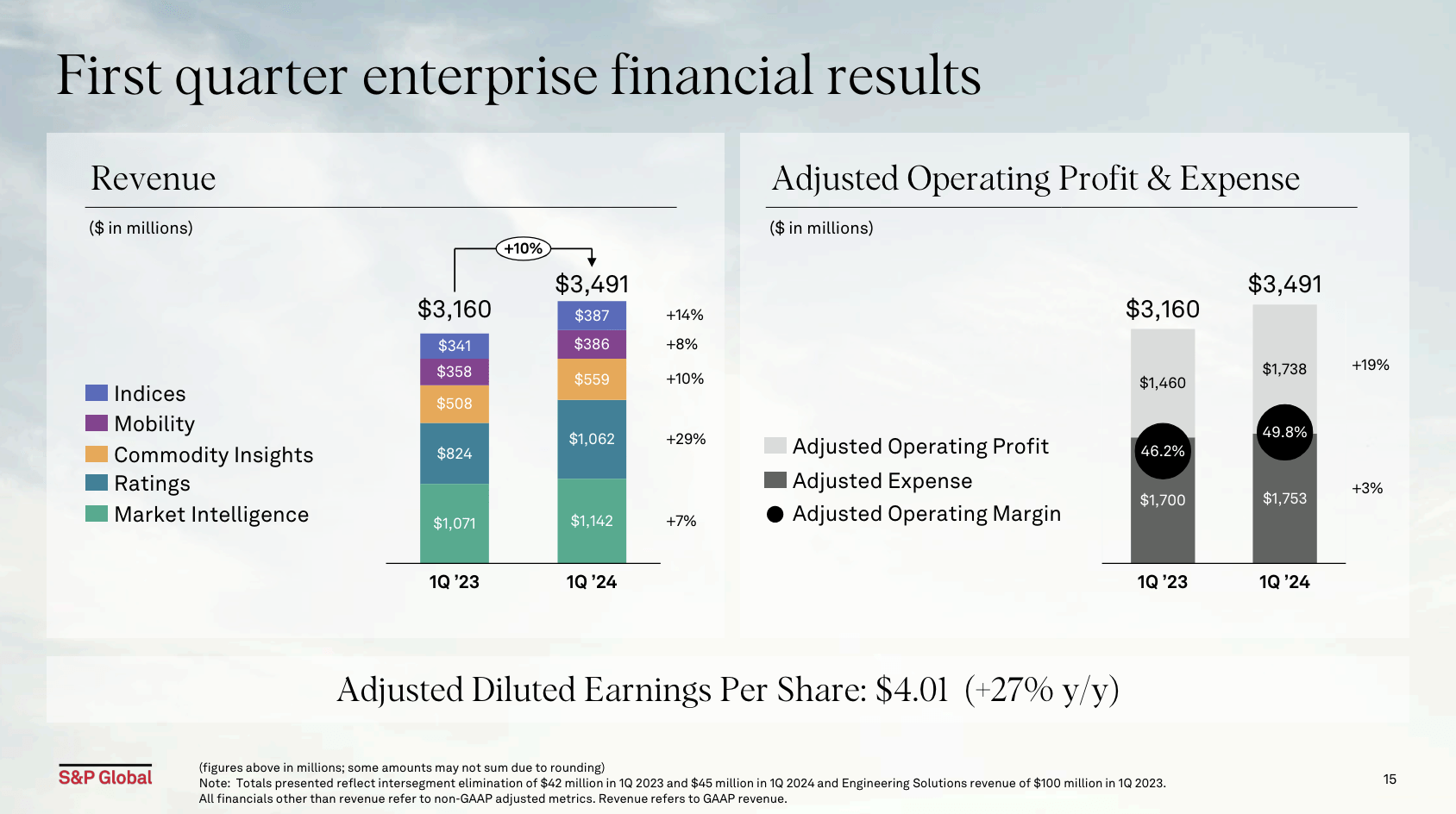

In its just-released first quarter, the company reported 14% revenue growth, adjusted for the divestiture of Engineering Solutions. Total revenue was $3.5 billion, the highest number in the company’s history.

This growth was primarily attributed to higher transaction revenue in the Ratings division, in addition to an 8% year-over-year increase in subscription revenue across the entire company.

S&P Global

Adding to that, 27% growth in adjusted EPS was fueled by a more than 350 basis points improvement in adjusted operating margins!

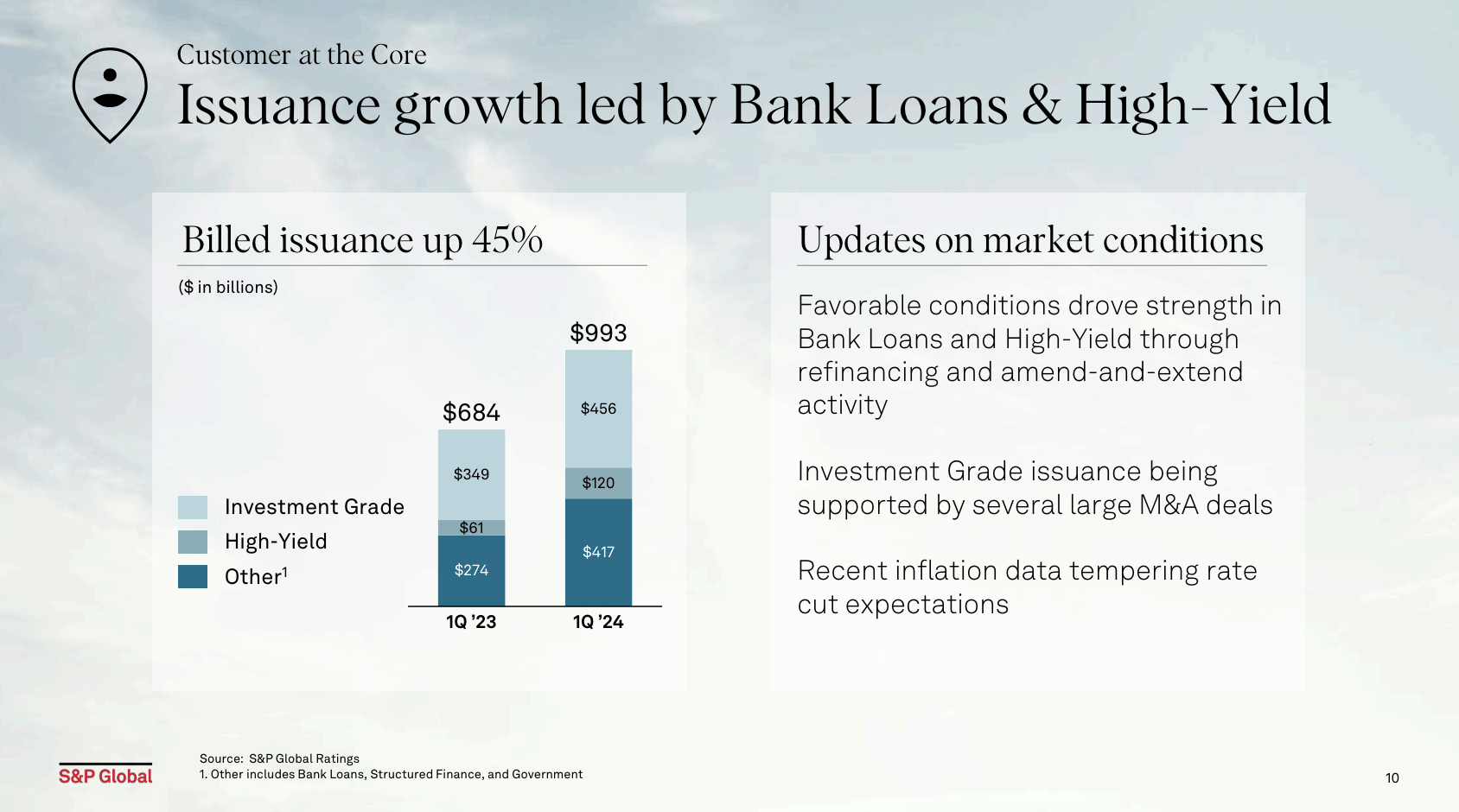

The company also noted that equity markets saw strong volumes from IPOs and M&A activities, while debt issuance reached its highest level since 2021.

In fact, the company confirmed perfectly what we discussed in the introduction. I added emphasis to the quote below:

Billed issuance increased 45% year-over-year in the first quarter. Tight spreads and stabilizing risk appetite in the market created favorable conditions for issuers. We saw investment-grade, high-yield and bank loan volumes all increased as issuers took full advantage to raise debt early in the year. We do expect much of this strength was pull-forward from later in 2024, reinforcing our continued view of a stronger first half than second half in issuance volumes. – SPGI 1Q24 Earnings Call

S&P Global

Nonetheless, we are not out of the woods. The company made clear that uncertainties persisted, driven by macro and geopolitical factors. I agree with that, as I expect persistent inflation to force the Fed to keep rates higher for longer.

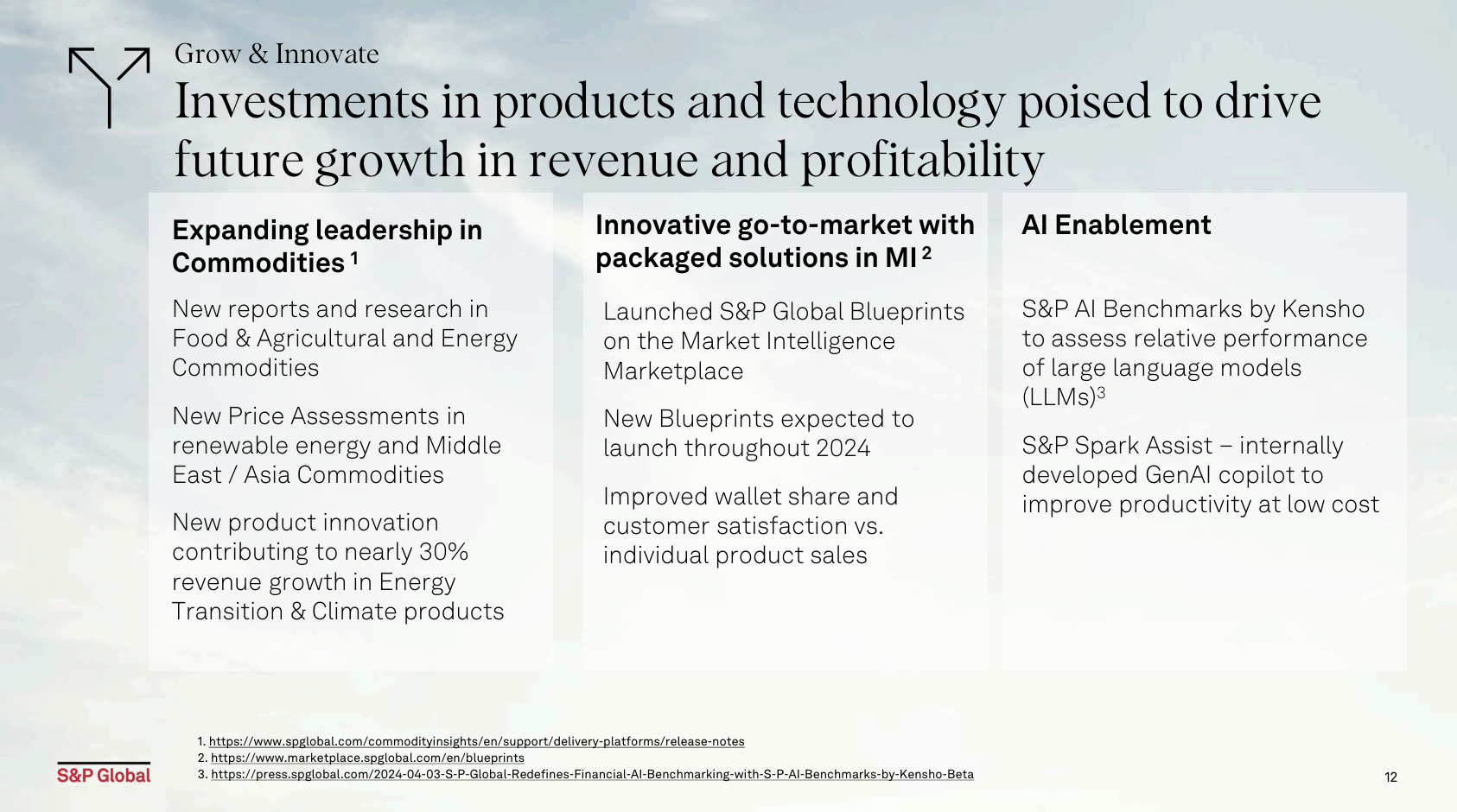

That said, beyond ratings, the company launched new products and improvements to existing offerings.

Developments worth mentioning include the launch of a food and agriculture commodities dashboard, new price assessments for renewable energy, and the introduction of Blueprints in Market Intelligence, which are tailored packages of data sets and tools for specific customer types and requirements.

Blueprints also allow customers to experience more of S&P Global’s products, which may make it easier to upsell them.

S&P Global

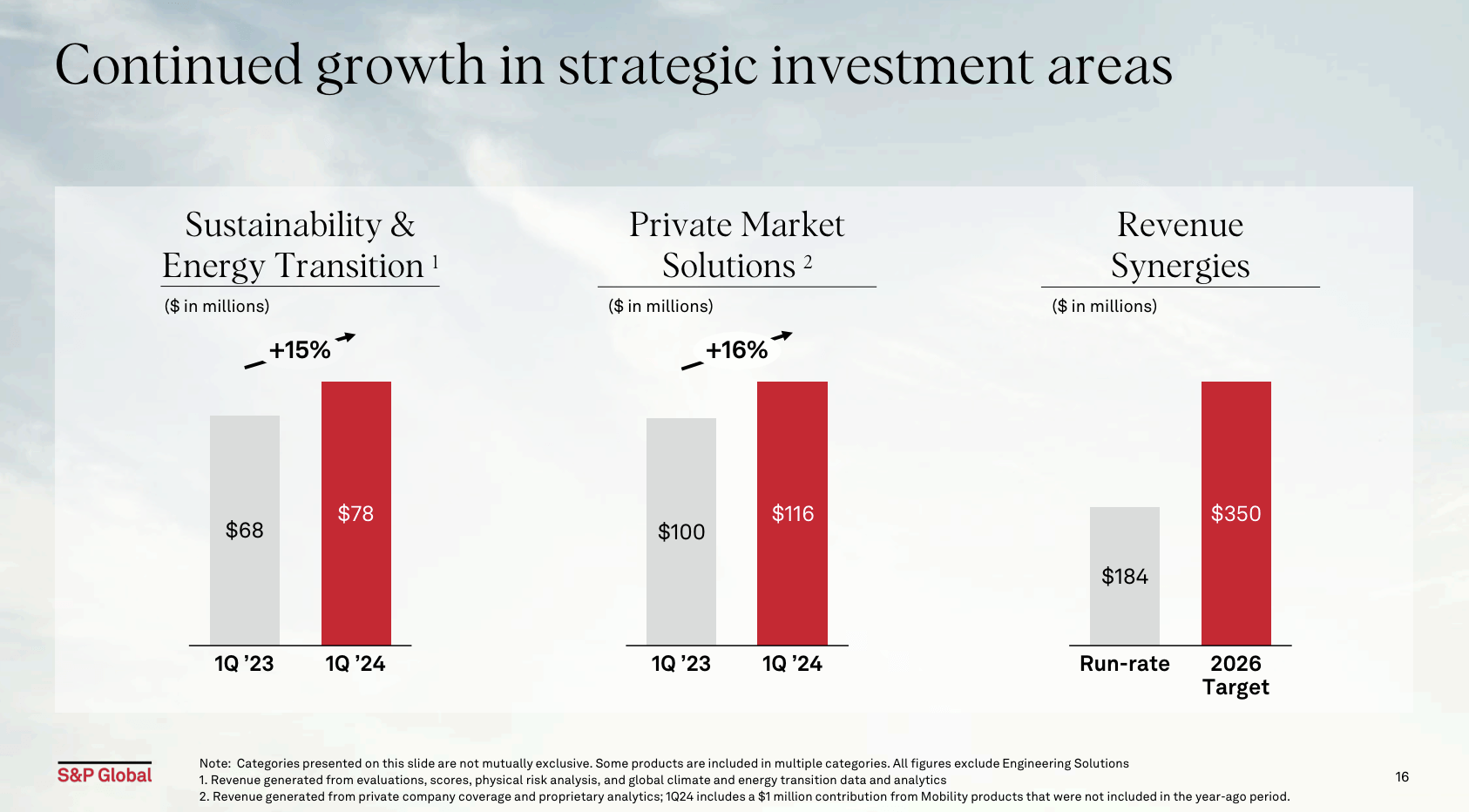

The company also reported rapid growth in energy transition and climate products and highlighted developments in AI-fueled services.

For example, the company has something called S&P Spark Assist. That’s a copilot platform aimed to improve productivity, facilitate innovation, and reduce time spent on routine tasks.

That’s where the company’s valuable data comes in – that most other AI bots have no access to (to my best knowledge).

Essentially, by leveraging proprietary data and expertise, S&P Global developed the platform internally, delivering a competitive system at subdued costs.

[…] we’re delivering the power of generative AI to our people in an easy-to-use platform at the cost of less than $1 per user per month. We’re incredibly excited about what this tool can do for our people, and we’ll provide more details around use cases and productivity as we progress through the year. – SPGI 1Q24 Earnings Call

In general, when it comes to new product launches and operational synergies, the company is ahead of schedule toward achieving its $350 million revenue synergy target, with an annualized run rate of $184 million by the end of the first quarter.

- In 1Q24, the company saw $56 million in revenue synergies, driven by successful cross-sell initiatives.

- It launched 25 new products and plans to launch 15 additional synergy products by the end of this year.

S&P Global

Having said all of this, the company is upbeat about its future, which bodes well for its valuation.

Shareholder Value & Valuation

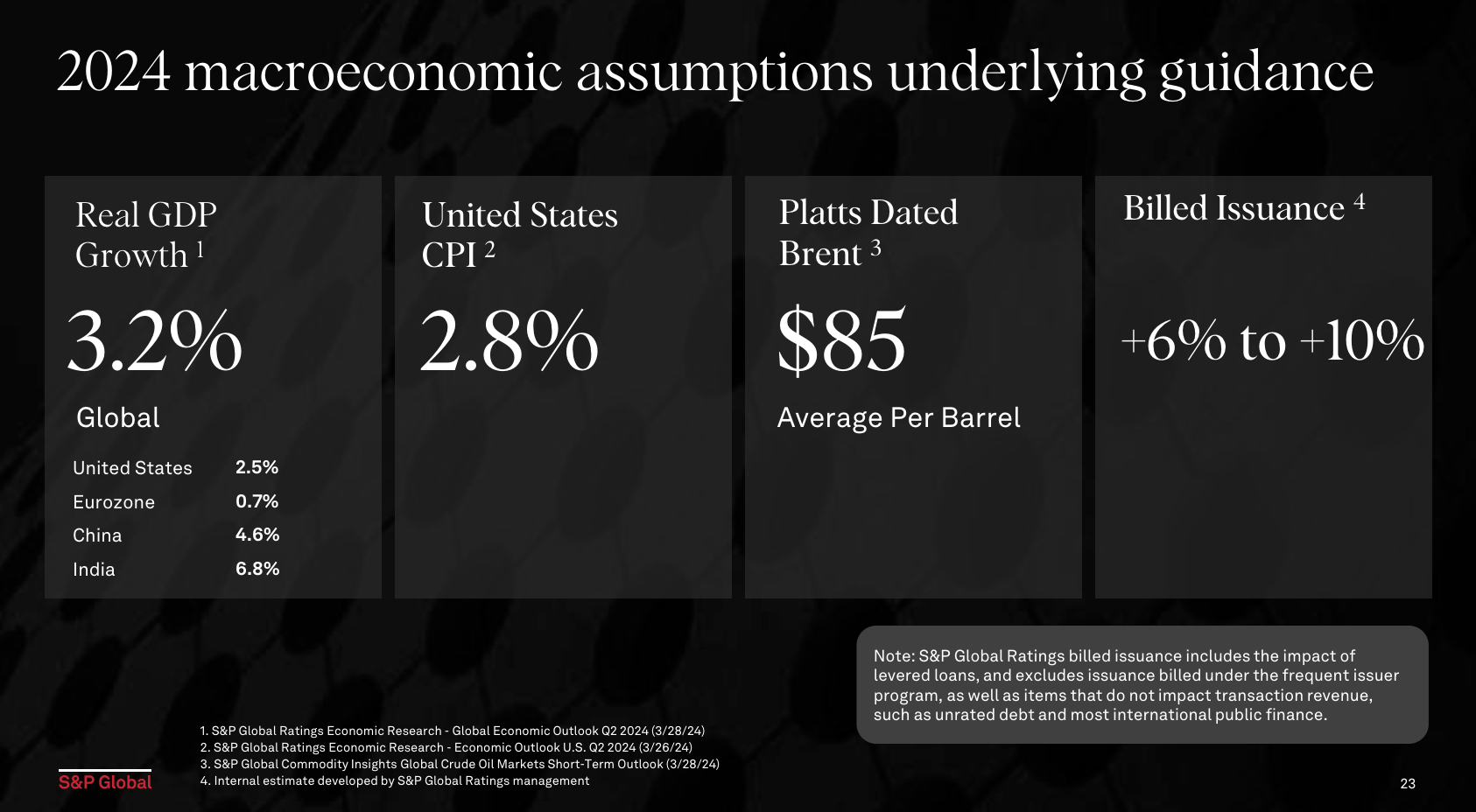

Higher-than-expected. That’s how I would summarize the company’s “big picture” 2024 outlook, as it hiked its assumptions for GDP growth, inflation, and the average price of Brent crude oil.

S&P Global

While these developments have caused the market to price in fewer rate cuts, it’s overall a good development for the global economy.

The company is also upbeat about billed issuance, which is due to issuers taking advantage of favorable market conditions, and the same reason that explained why issuance did so well in the first quarter.

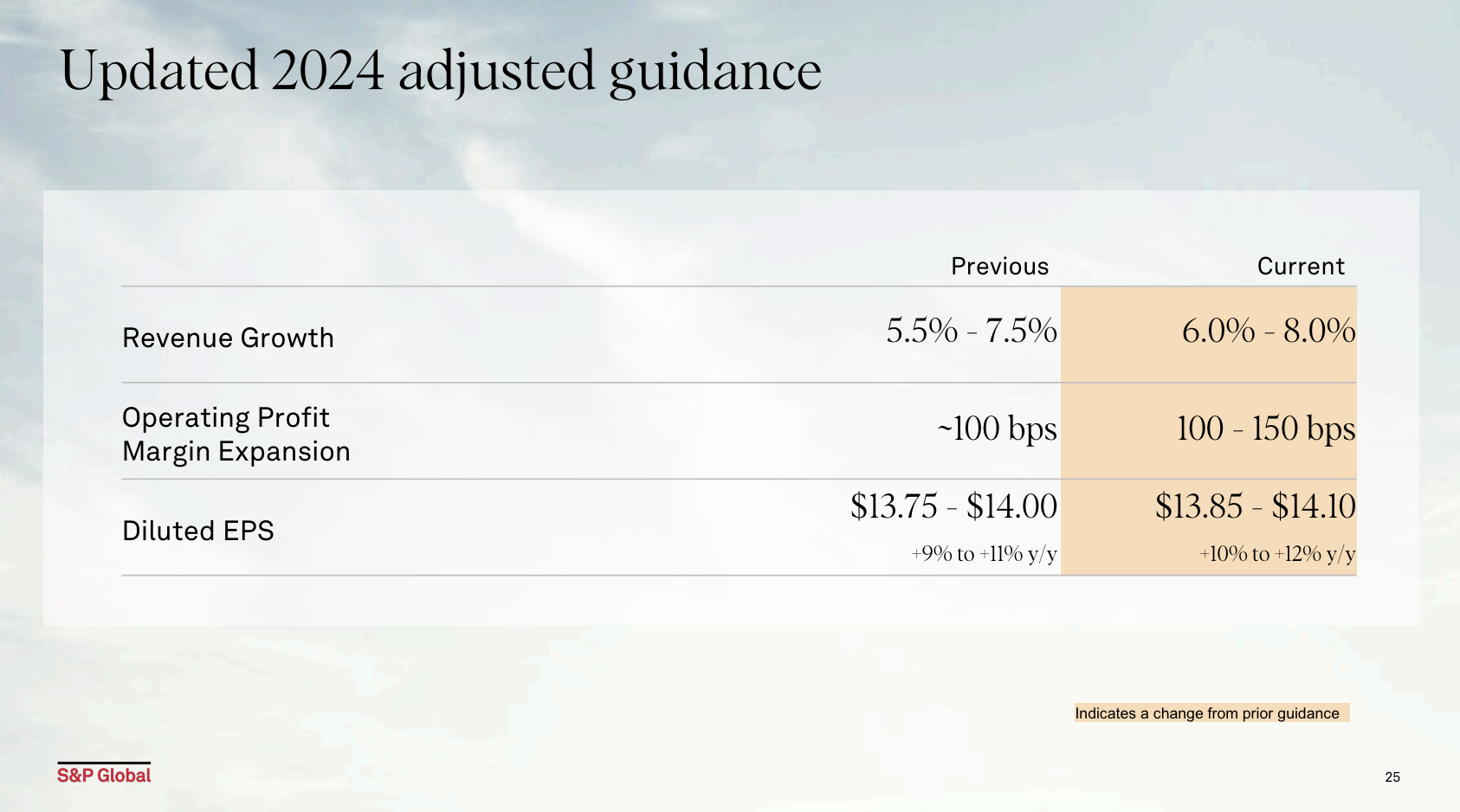

As a result, the company’s full-year guidance anticipates higher revenue growth, stronger margins, and higher EPS. However, these expectations include the potential for softening in the second half of the year, as a lot of debt issuance has been pulled forward.

S&P Global

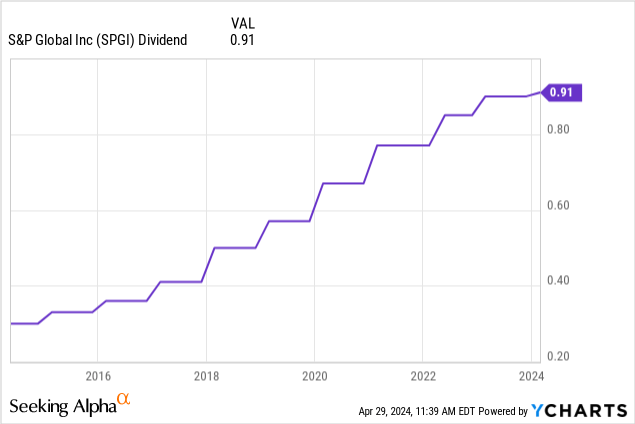

In the first quarter, SPGI also hiked its dividend.

However, the hike was a bit underwhelming, as it hiked by 1.1% to $0.91 per share per quarter. This translates to a yield of 0.90%.

The good news is that the company has a sub-30% payout ratio and a 5-year CAGR that is still 12.5%.

The only reason why its yield is so low is its fantastic stock price performance, which more than made up for its low yield.

With that said, there’s good and bad news.

- Good news: Analysts agree with the company, as they expect strong growth to last. Using the FactSet data in the chart below, analysts expect 12% EPS growth in 2024, potentially followed by 14% and 13% growth in 2025 and 2026, respectively.

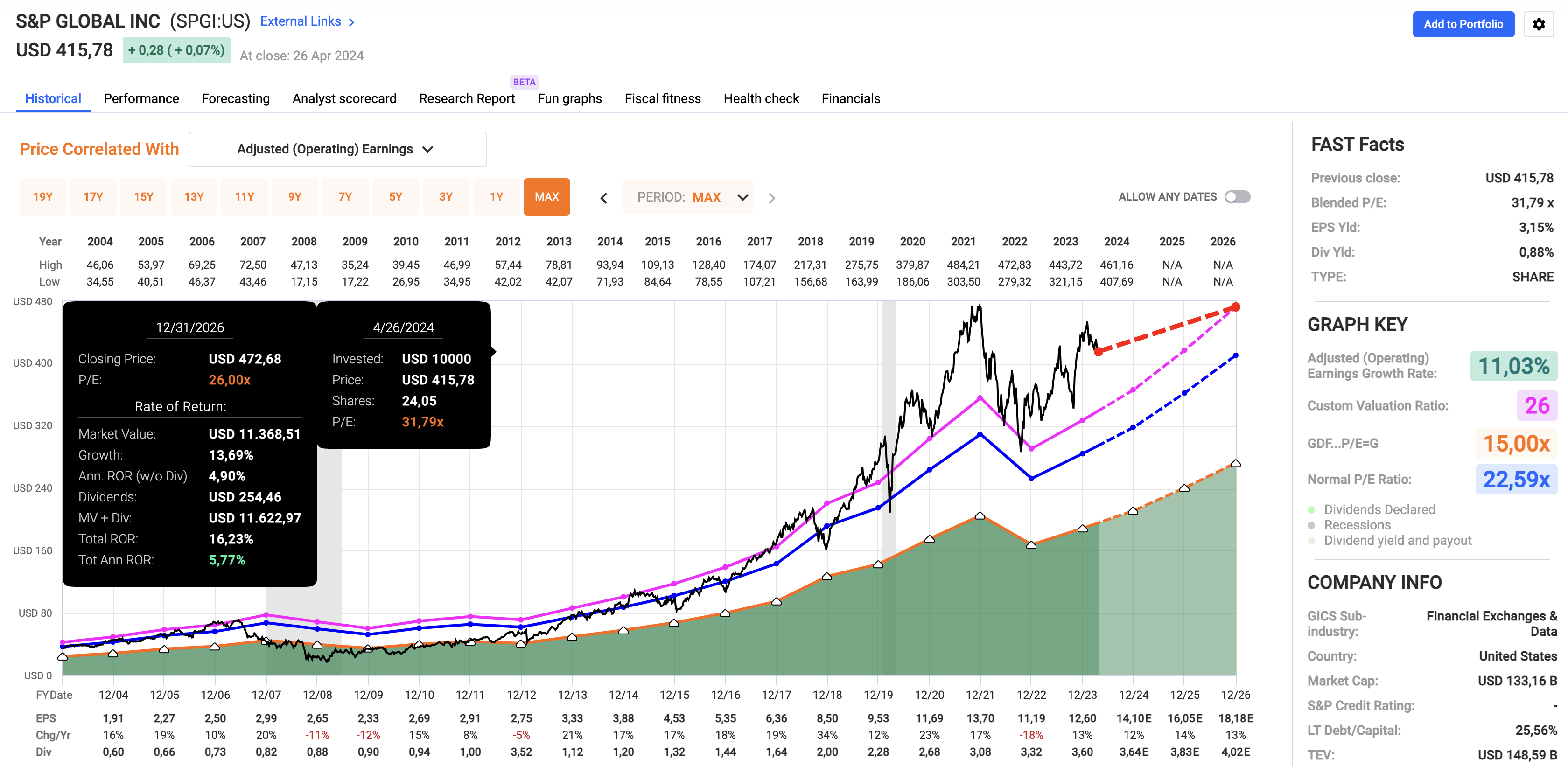

- Bad news: A lot of good news has been priced in. SPGI is trading at a blended P/E ratio of 31.8x, which is above its 20-year normalized P/E ratio of 22.6x (blue line) and its ten-year normalized P/E ratio of 26.0x (pink line).

FAST Graphs

Using its ten-year multiple (26x), we get a fair stock price of roughly $473 by incorporating EPS growth expectations. This is 14% above its current price.

The current consensus price target is $493.

All things considered, I stick to my Buy rating. However, I would not make the case that new investors should initiate a full position at these prices. Given the market’s latest rally and economic risks tied to a higher-for-longer interest rate and inflation environment, I believe the SPGI stock price could see a correction in the months ahead.

Takeaway

S&P Global shines as the world’s leading rating agency, leveraging data to fuel high-margin growth.

Despite short-term market fluctuations, SPGI’s robust revenue and EPS growth in 1Q24 underscore its resilience and innovation.

However, while its outlook remains bullish, I believe cautious optimism is warranted due to its premium valuation.

Hence, monitoring for potential corrections could present opportunities for strategic investment in this financial market giant.

Pros & Cons

Pros:

- Leading Position: As the world’s largest rating agency, SPGI has a dominant position in a very important market.

- High-Margin Growth: Its use of data drives impressive revenue growth and maintains attractive profit margins.

- Innovation: By constantly evolving beyond traditional rating services, SPGI introduces new products and services.

- Revenue Stability: With a significant portion of revenue coming from recurring sources, SPGI provides earnings visibility and resilience.

- Future Outlook: Upbeat guidance and strategic initiatives position SPGI for continued success, enticing long-term investors.

- Dividend Growth: While the stock has a low yield, it comes with elevated historical dividend growth.

Cons:

- Valuation Concerns: The premium valuation relative to historical norms raises questions about near-term upside potential.

- Market Fluctuations: Vulnerability to market downturns or economic uncertainties could impact stock performance.

- Dividend Yield: While the dividend is increasing, the current yield remains modest, which could be an issue for income-focused investors.

- Timing Consideration: Given the recent market rally, a cautious approach may be prudent, waiting for potential corrections before initiating a full position.

{kind=link}