alexandre17/iStock via Getty Images

I upgraded Equifax (NYSE:EFX) from ‘Buy’ to ‘Strong Buy’ in my previous coverage published in April 2024, anticipating a modernization of the mortgage business, as well as strong growth momentum in the non-mortgage business. The company delivered 8% organic revenue growth with a 13% growth in non-mortgage businesses in Q2 FY24. It is impressive for the company to deliver 4% growth in US mortgage revenue despite a 13% decline in mortgage credit inquiries. I anticipate the mortgage business to continue recovering, and the non-mortgage to sustain growth momentum. I reiterate ‘Strong Buy’ rating with a one-year price target of $360 per share.

Best Play for Interest Rate Cut

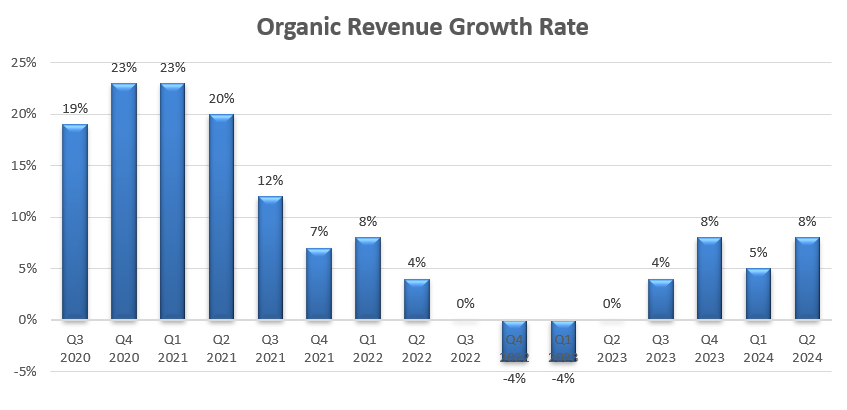

In Q2, Equifax delivered 8% organic revenue growth with 13% growth in non-mortgage businesses, as shown in the chart below.

Equifax Quarterly Earnings

The Fed is likely to cut interest rates this September, and it is timing for investors to think about companies that can benefit from lower interest rates. I view Equifax as one of the top performers amid an interest rate down cycle. Key reasons include:

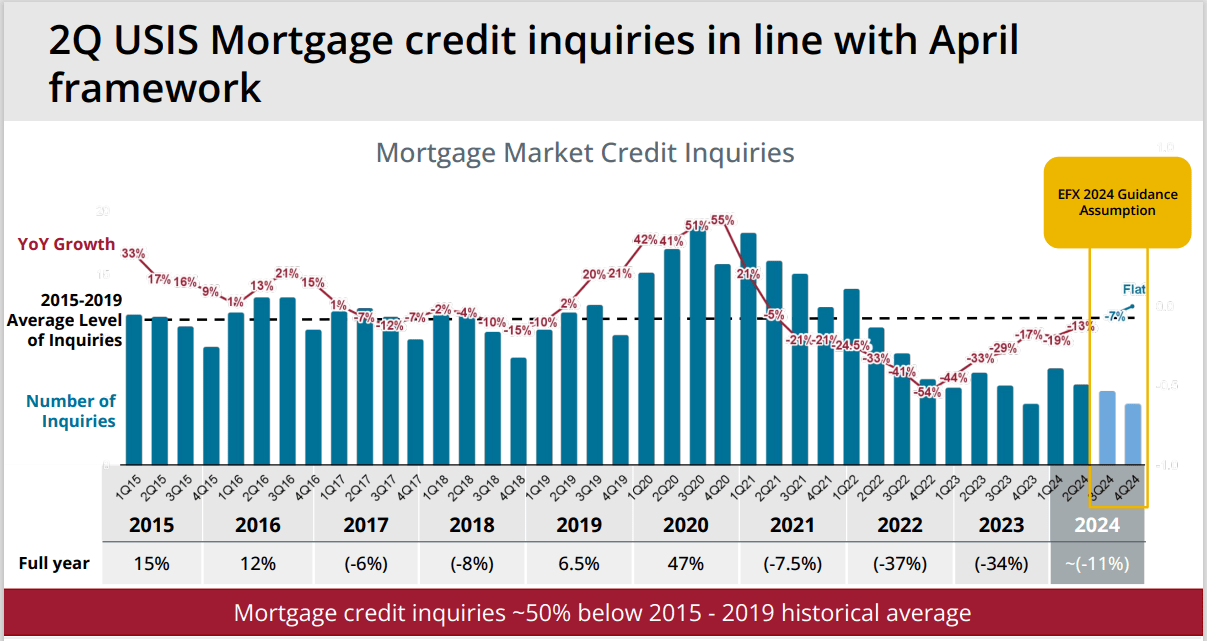

- During the period of rising interest rates, the U.S. mortgage credit inquiries declined by 7.5% in 2021, followed by a sharp 37% decline in 2022 and 34% drop in 2023, as shown in the slide below. Equifax anticipates the overall mortgage credit inquiries will decline by 11% in 2024, assuming no change in interest rates. Even without any interest rate cuts, the credit inquires market has already begun to stabilize; after all, some mortgage refinance demand is non-discretionary.

Equifax Investor Presentation

- As indicated in my previous article, Workforce business is Equifax’s most important growth driver. Workforce Solutions grew by 5% in Q2, with 12% non-mortgage revenue growth offset by 12% mortgage revenue decline. When we enter into the interest rate cut cycle, I anticipate the mortgage component will start to recover. Mortgage represents around 25% of total Workforce revenue, and is quite sensitive to the interest rate. As such, the revenue growth in Workforce Solutions is likely to accelerate in FY25.

- Lastly, when the Fed starts to lower the interest rate, I anticipate the job market will gradually start to recovery. As pointed in my previous coverage, Equifax is providing employment verification services, and possesses the largest database for employment and income data. An improving job market could potentially benefit their Workforce solution business.

Growth Projection and DCF Update

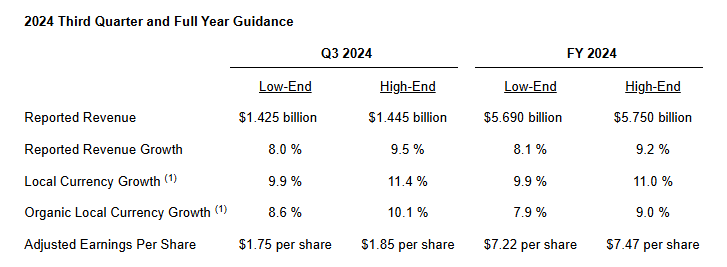

Equifax is guiding for around 9% revenue growth for FY24, as detailed as follows:

Equifax Quarterly Earnings

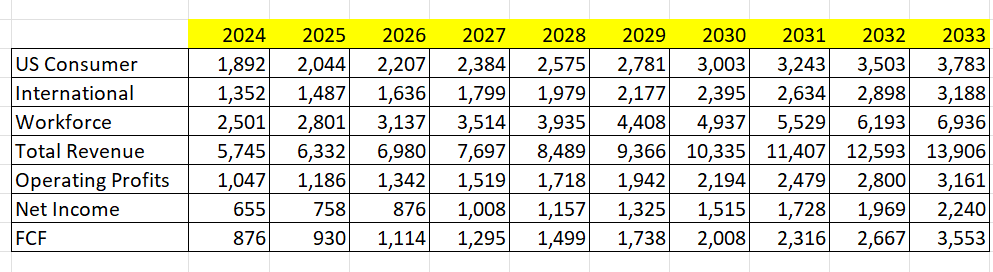

I calculate Equifax will deliver 9.1% revenue growth in FY24, then accelerate to 10.2% from FY25 onwards. Key assumptions include:

- US Consumer: I anticipate the segment will grow by 10% in FY24, driven by accelerated non-mortgage growth. During the earnings call, Equifax disclosed that the company has completed the cloud migration for the US consumer business. The cloud migration will help Equifax’s customers better utilize Equifax’s credit inquiries servers. From FY25 onwards, I anticipate the US consumer will grow by 8%, in line with the growth rate in a normalized interest rate environment.

- International: I anticipate the growth momentum will be sustained in the near future, growing by 10% annually. Equifax has been investing in their consumer/commercial B2B solution, as well as data analytics for their international market. These value-added services will help the company sustain double-digit revenue growth in the near future.

- Workforce: I forecast the segment will grow by 8% in FY24, then accelerate to 12% from FY25 onwards, primarily driven by the anticipated interest rate cut. As discussed earlier, I anticipate the Fed will begin to cut interest rates this September, and Equifax’s Workforce Solutions will benefit materially from FY25 onwards.

On the margin side, there are several factors to be considered:

- Equifax has already completed their infrastructure upgrades and investments over the past few years. They have successfully migrated most services into cloud infrastructure. Therefore, the depreciation and amortization costs are likely to come down in the future.

- During the earnings call, the management indicated a strong pricing environment for Equifax’s key services. The pricing improvement will expand their gross margin going forward.

- Lastly, Equifax is likely to achieve operating leverage from their SG&A expenses, as revenue growth continues at a high single-digit rate.

Considering all these factors, I calculate Equity will achieve 50bps annual margin expansion. The DCF summary can be found as follows:

Equifax DCF

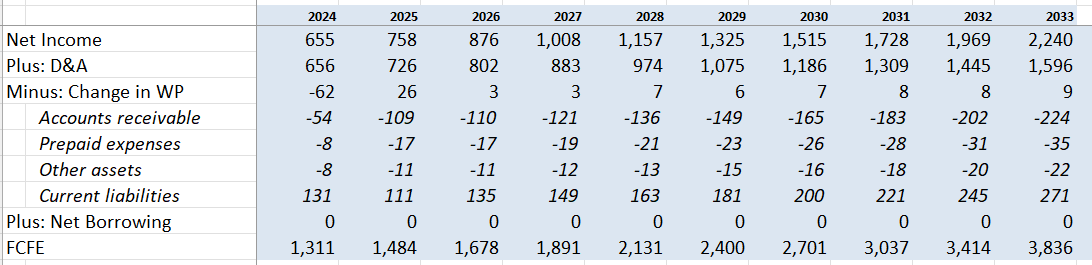

I calculate the free cash flow from equity (FCFE) as follows:

Equifax DCF

The cost of equity is estimated to be 12.3% assuming: risk-free rate 3.8%; beta 1.42; equity risk premium 6%.

Discounting all the FCFE at a rate of 12.3%, the one-year target price is calculated to be $360 per share.

Downside Risks

Equifax completed the acquisition of Boa Vista Serviços (BVS), the second-largest credit bureau in Brazil. Equifax has made good progress in integrating BVS so far, generating $41 million in revenue during the quarter. However, considering the weak economy and high inflation in Brazil, I am cautious about Equifax’s business prospects in the country. Equifax is still in the process of integrating BVS’s core assets, and it remains uncertain whether the company will face any integration challenges in the near future.

End Note

I view Equifax as one of the best stocks to invest in during an interest rate cut cycle, as a significant portion of their overall businesses will benefit from a lower interest rate environment, in my view. I reiterate ‘Strong Buy’ rating with a one-year price target of $360 per share.

{kind=link}