Andrii Dodonov

EPD stock and our barbell investment model

We recently started a position in Enterprise Products Partners L.P. (NYSE:EPD) for our income account. As communicated in this brief post, the position was to replace our Verizon shares, which we terminated recently. Before I dive into EPD further, I must first take a step back and say a few quick words about our overall investing strategy. I use a so-called barbell model to manage my family investment portfolio. As detailed in my earlier article,

…contrary to the popular advice of building “a” retirement portfolio or “the” perfect retirement portfolio, we always hold two portfolios: one for short-term survival (e.g., a visit to the ER next month) and one for long-term growth (e.g., take care of things when we are 90 years old and estate planning for kids and grandkids). Isolating long-term and short-term risks is the first step of diversification.

And we suggest you do the same at ANY stage of life – just adjust the amount of funds you put in each end of the barbell. Under this overall philosophy, my thesis here is to explain why EPD is an excellent choice for the income end of the barbell. In the remainder of this article, I will elaborate on the following considerations:

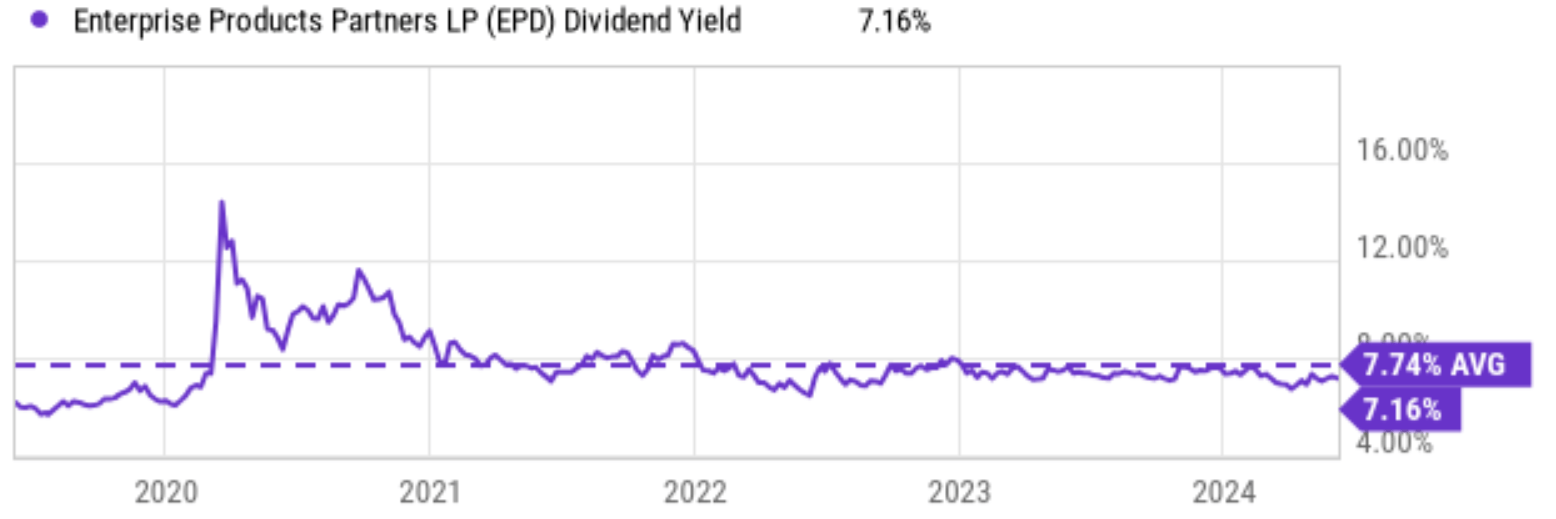

First, EPD currently yields about 7.16% (see the next chart below), providing a very high current income both in absolute and relative terms (e.g., it is significantly higher than Verizon Communications Inc. (VZ) shares we sold recently). What’s more important are the growth rates and consistency. As a dividend champion, EPD has been growing its dividends consistently for the past 25 years. Enterprise has one of the best and most resilient operations in the midstream sector in my view, to be elaborated on more later.

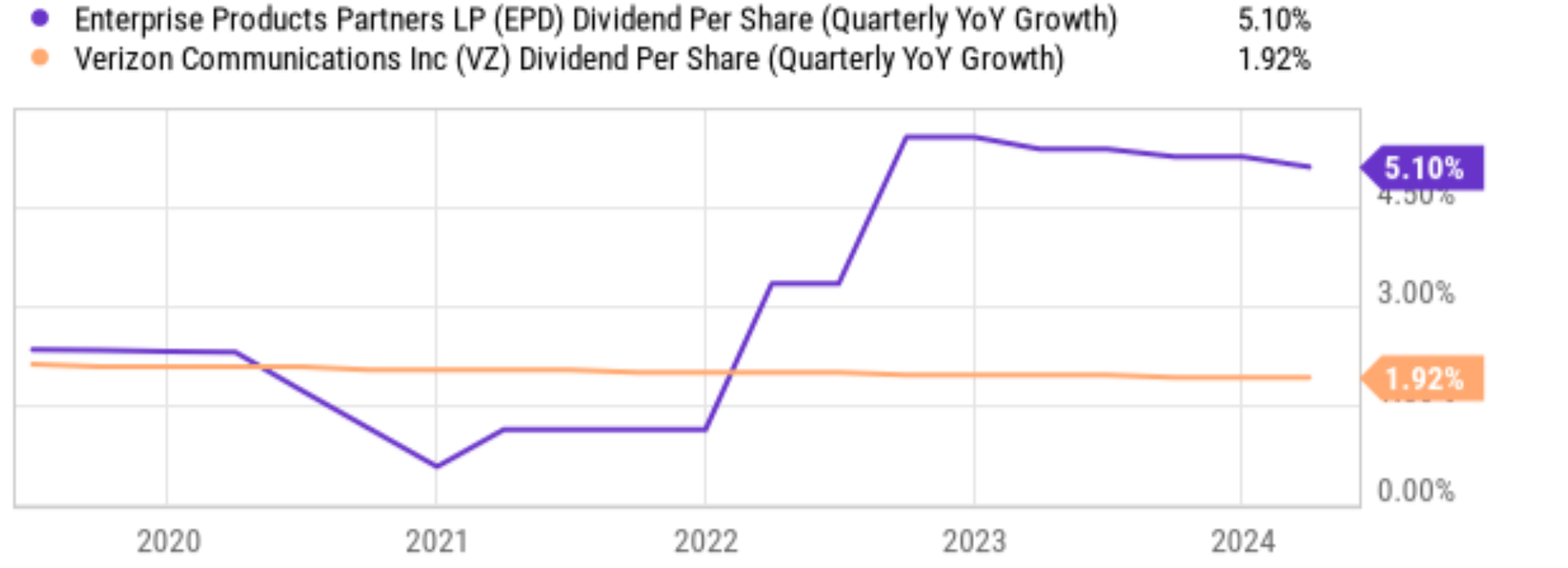

And the growth rates are quite robust, as demonstrated by the second chart below. The YOY growth rates dropped sharply during the pandemic, but shortly recovered to be above 4% per annum (which is also about the average growth rate in the past 10 years). Later, I will explain why I anticipate such a healthy growth rate to continue given our future power, especially the need driven by AI technology and high-end manufacturing.

Finally, the valuations are very reasonable despite a robust growth outlook.

Seeking Alpha Seeking Alpha

EDP’s relevance to our AI future

I assume you are familiar with the challenges and opportunities surrounding our AI technologies. These issues range from technological to ethical and legal. Among all these issues, a less-often discussed, but a crucial issue in my view is energy cost. As argued in my recent article analyzing NVIDIA Corporation’s (NVDA) new Blackwell chips,

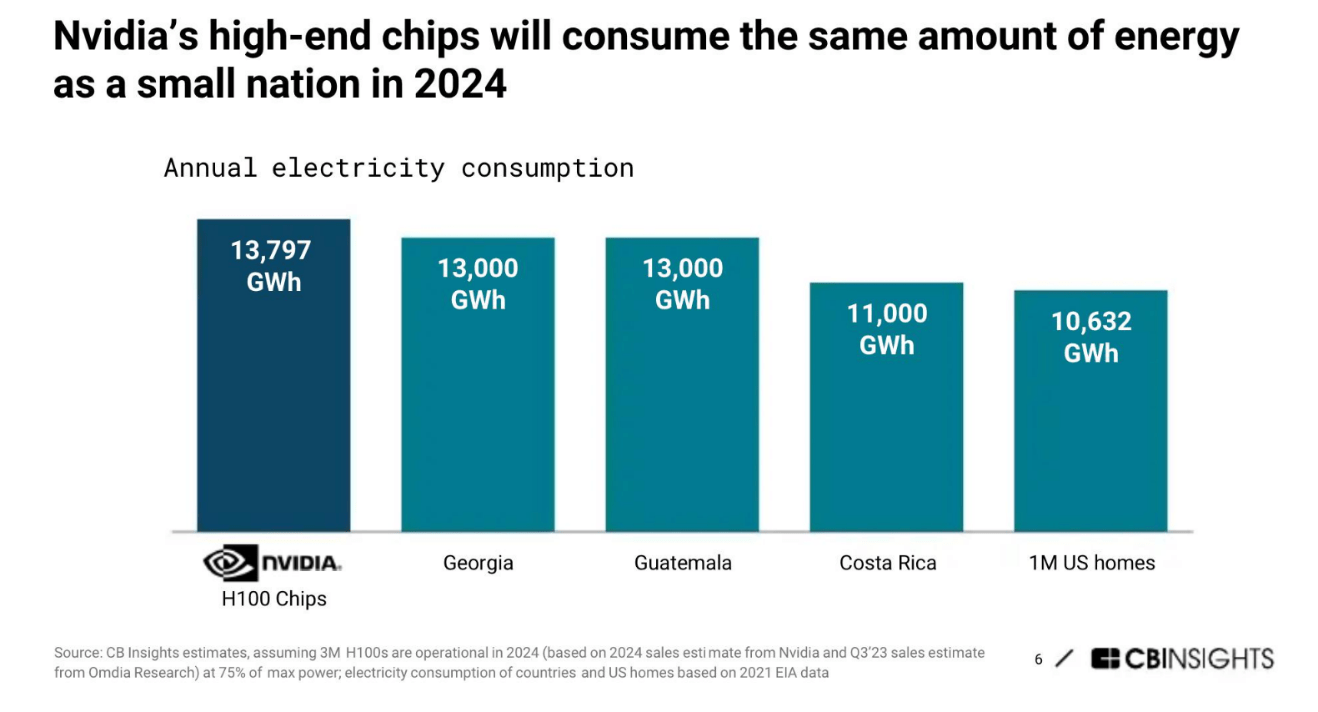

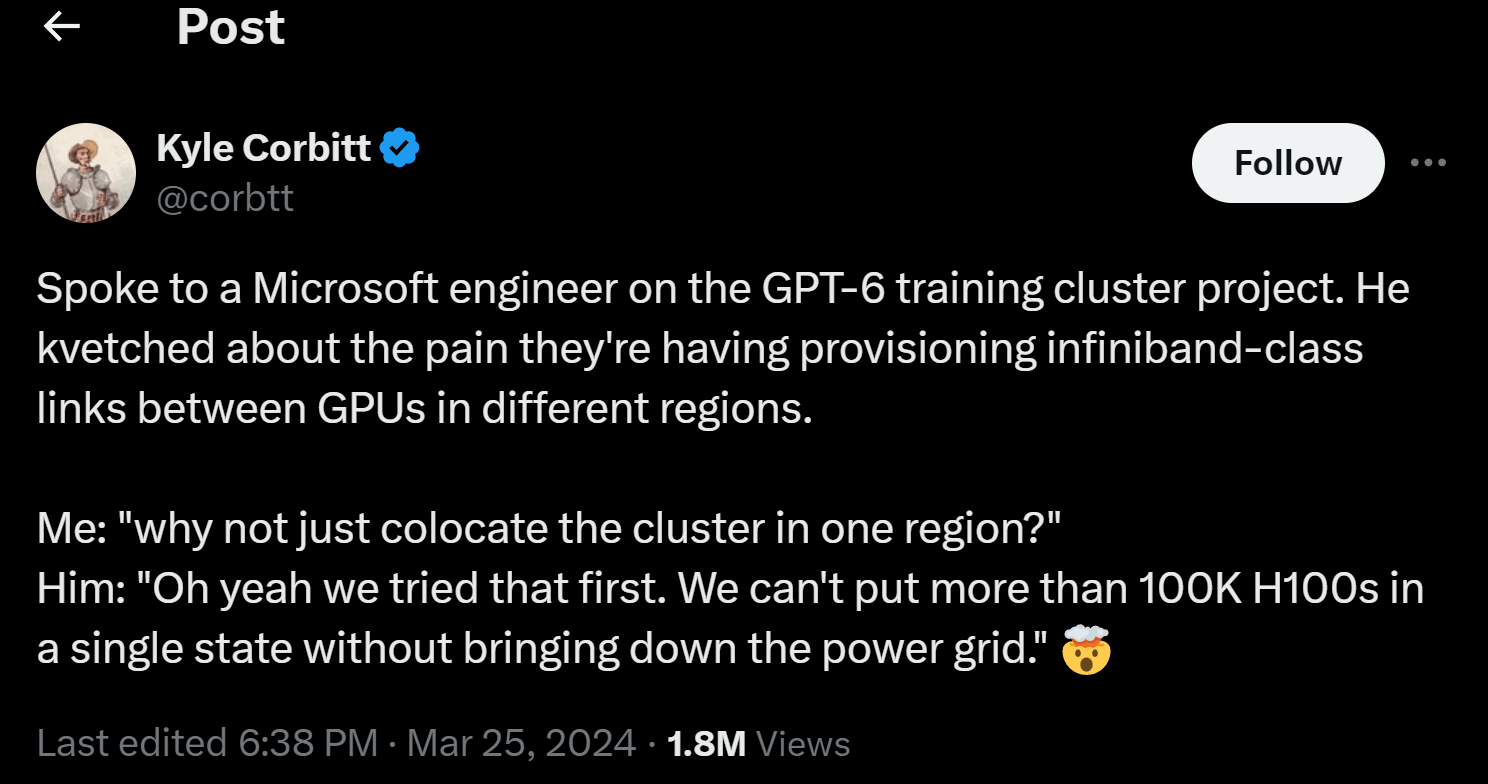

… each of Nvidia’s H100 chips consumes 700W of energy at peak operation. This is more than the power consumption of the average American household. Collectively, NVDA’s high-performance AI chips are estimated to consume more energy than many small nations as you can see from the chart below. Even for one data center, which typically employs thousands to tens of thousands of these chips, the peak power consumption can overload the power grid of a region or even a state according to the following comments from Microsoft engineers (see the second chart below).

CBInsights Source: X.com

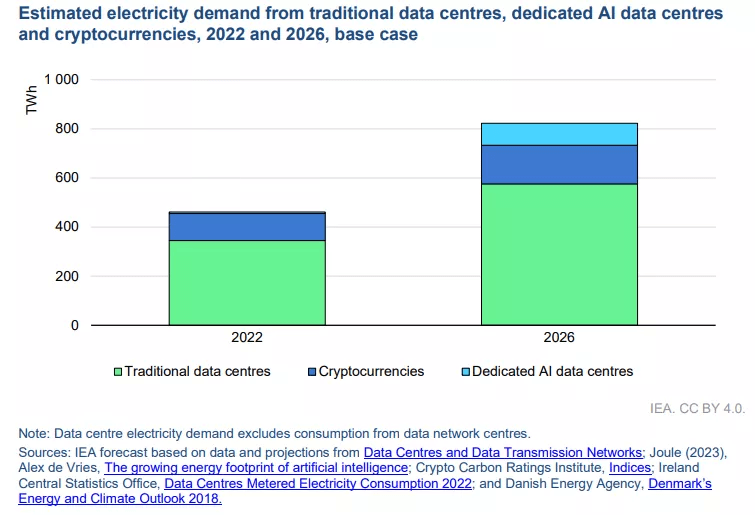

Besides AI, our digital future also includes other power-hungry technologies such as cryptocurrency, intelligent manufacturing, etc. (see the next chart below). I believe EPD would benefit greatly from utilities building new baseload facilities to meet such future power needs. The demand for electricity in the U.S. has been growing rapidly over the past few decades. However, certain regions of the country have had issues bringing new gas-fired power plants online. The reindustrialization of America (again, led by AI and other digital technologies) requires enormous amounts of electricity, and my view is that the country has been underinvesting in its power-generating capacity for years if not decades.

IEA

EPD is a leading integrated provider of natural gas and natural gas liquids (“NGLs”) processing, transportation, fractionation, and storage services in the country (with some Canadian exposure too). The main operation of EPD is precisely the transportation of natural gas from one location to another. Given my outlook for our growing power need, and especially the geographical unevenness of such need, I expect EPD to see its profitability climb in tandem as we construct more power capability.

Next, we will see that EPS is indeed well-positioned to help us meet this need.

EPD’s construction program

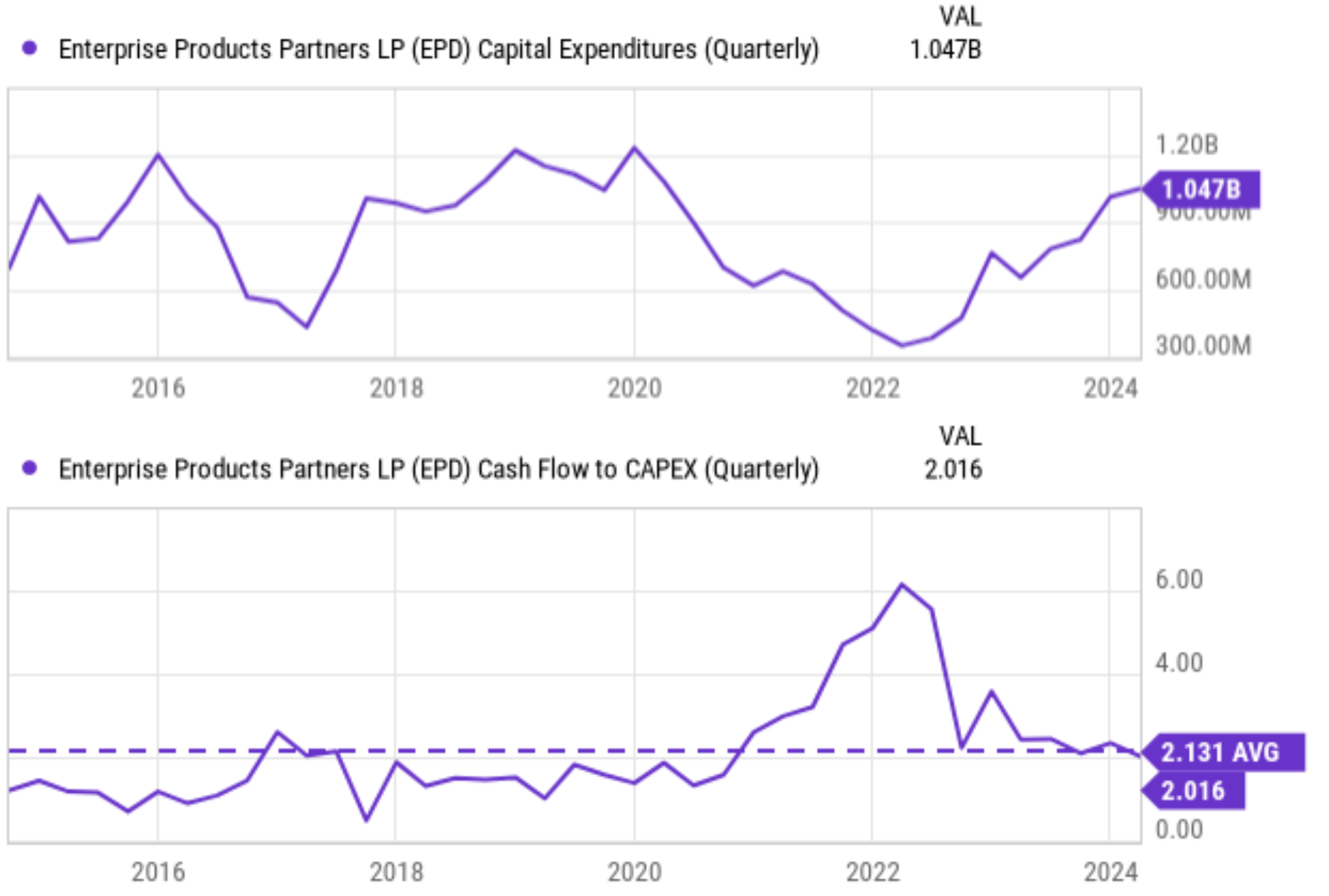

To meet our future energy needs, EPD has many sizable construction programs ongoing. It is involved in most shale plays in the United States, and it is one of the biggest members in this space. For example, it intends to spend $3.5 billion both this year and next to expand its operations. As of April 2024, Enterprise had $6.9 billion worth of projects being developed. To better contextualize things, the next chart shows its CAPEX expenditures in recent quarters (top panel). As seen, the expenditures have been trending up substantially in the past 1~2 years.

Seeking Alpha

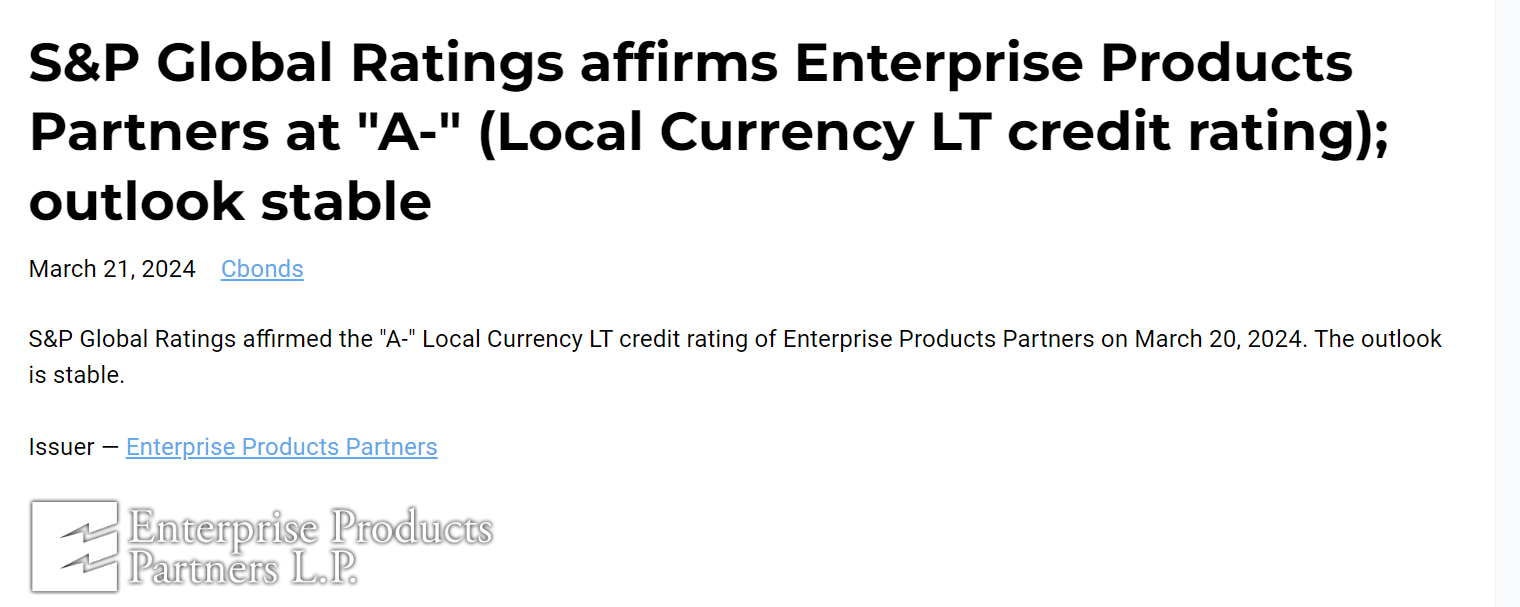

However, thanks to its strong cash generation and solid balance sheet, the company is in a good position to fund its capital projects sustainably. As you can see from the bottom panel of the chart above, despite the increased CAPEX expenditure recently, its cash flow to CAPEX ratio remains slightly above its historical average (a high ratio means better capital allocation flexibility). The balance sheet is sound, too. Many midstream companies are overleveraged due to their heavy dependence on borrowed funds to finance new projects. In Enterprise’s case, only about half of its total capital consists of debt. The partnership receives strong credit ratings with a stable outlook (see the next chart below).

CBonds

Other risks and final thoughts

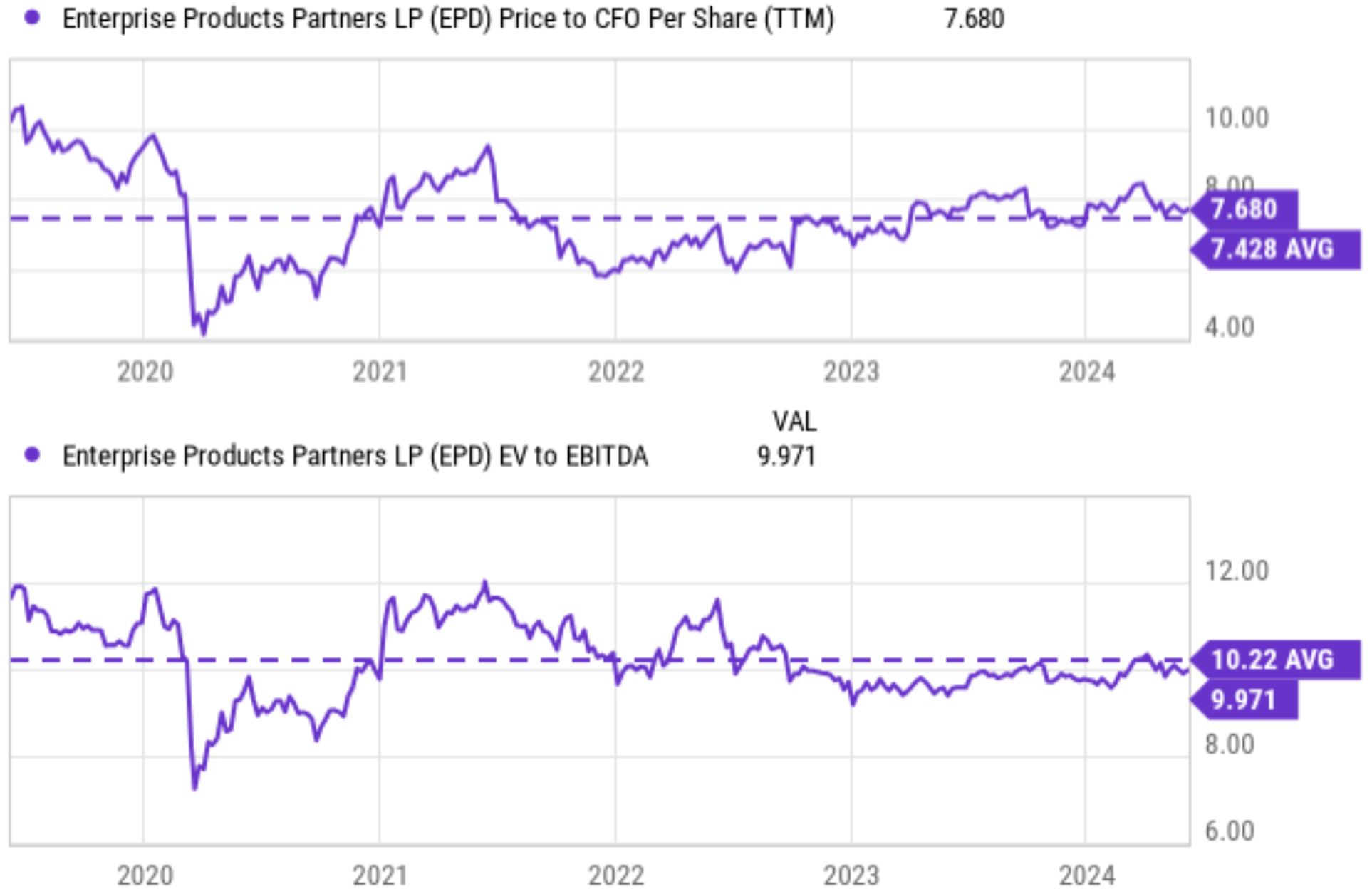

Despite the growth potential and solid financial position, the stock (or the unit to be more precise, given its MLP status) is reasonably priced. As you can see in the top panel of the chart below, in terms of P/CFO ratio, EPD is currently priced at a ratio of 7.68x at the price of this writing, very close to it (only about 3% higher). As a midstream stock, EPD uses more leverage than the general economy. As such, it is important to take a look at its leverage-adjusted valuation metric too. The bottom panel shows EPD’s EV/EBIT ratio compared to its historical averages. As seen, this metric points to the same conclusion of a very reasonable valuation. Its current EV/EBITDA ratio is 10.2x, again essentially on par with its historical average of 9.97x.

Seeking Alpha

In terms of downside risks, I assume investors are all familiar with the common risks facing EPD and other similar midstream companies. These risks include fluctuations in oil prices, fluctuations in natural gas prices (often exceeding those of oil prices), environmental regulations, et al.

For EPD, there are some additional risks to consider. First, given its vast network of facilities, pipeline spills and damages are always a risk. The possibility of potential incidents (either due to natural disasters or facility malfunction) can cause significant financial impact and also reputation damage. Second, EPD’s current focus remains on hydrocarbon fuels and has very limited exposure to renewable energy sources (which is an area some of its peers are investing in). Such lack of exposure may expose EPD to the threat of competition from renewable energy providers. However, I think this is a very remote threat. My view is that given the increasing demand for our energy needs, renewables will not be even enough to meet the INCREASE in our demand. In other words, I expect robust growth for “traditional” energy sources such as natural gas also (see the next chart).

All told, my conclusion is that EPD is an excellent opportunity for accounts oriented towards income generation. To recap, EPD offers a well-rounded package combination with a high current yield (over 7% currently), healthy dividend growth rates, remarkable consistency, and reasonable valuation. Looking ahead, I anticipate the growth rate to continue at a robust pace given our future power demands, especially those driven by the expansion of AI applications and other power-hungry digital technologies.

U.S. EIA

{kind=link}