JHVEPhoto

Dear readers/followers,

When I last covered Chemours (NYSE:CC) the company had seen some irregularities in its operations in accounting. In my last article, I saw a positive rate of return for the investment I made a few months prior – and the current rate of return from that article is barely negative here – but since my last piece, the stock is actually down a bit over 10%.

In this article, we’ll look at the longer-term implications and background of this move. I’ve long owned Chemours, unfortunately not too great returns, but I continue to believe that the company’s position in refrigerants and crucial chemicals has a potential for growth that outweighs the negative risks or downside at this time and valuation.

Investing in chemical businesses, like with other commoditized fields, comes with a certain amount of volatility. This is not a good investment sector for people who spook easily, or who feel the need to “act” or do something when something happens to the stock. The right way to react, in my view, is to look at the cause, gauge the actual effect for the long-term thesis, and work from that. Typically, the move is an overreaction and thus does not warrant our reaction beyond noting it and acknowledging that it happened.

Let’s see if there’s anything to consider here.

Chemours – 2Q24 had some weaknesses, but none of them are material or long-term

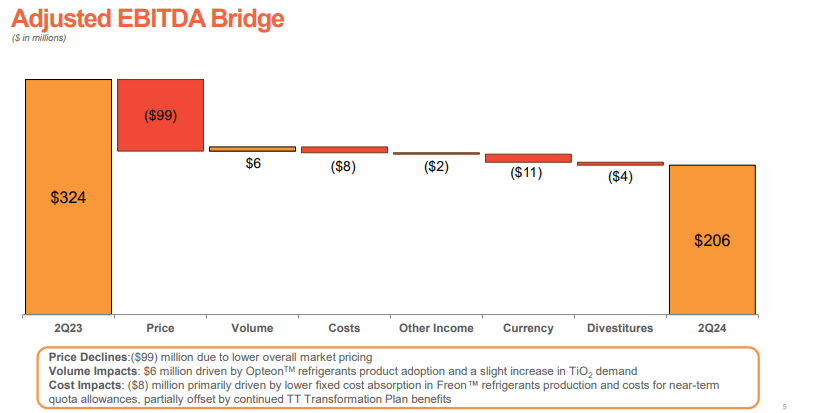

So, for 2Q24 the company generated over $1.5B in sales, and over $200M in adjusted EBITDA. To say that this represents a poor result would be wrong. This is also confirmed by the fact that the company saw a 16% sequential volume growth in the Titanium segment, despite operational disruptions in the company’s production.

On the refrigerant side, there was continued strong uptake and adoption of Opteon refrigerants, one of the primary reasons I continue to invest in Chemours. The company also owns Teflon, and has received permission to expand the production in the APM Performance solutions segment.

In correcting the company’s overall trends since the audit and accounting irregularities, the company has appointed a new CFO with the goal of driving enterprise growth.

EBITDA was down, and this is probably where much of the negativity about Chemours results in 2Q24 comes from. Pricing was the reason – not volume. The company actually sold slightly more, but the pricing trends are still not positive here.

Chemours IR (Chemours IR)

On a net sales basis, trends were flat – the company neither grew nor declined all that much for most of its important segments, and on the EBITDA and margin sides, things were either flat or slightly negative.

Another reason the share price is likely down is the cash moved to the Water District settlement fund (though this was already restricted cash prior to 2Q24). The company continues to have $1.5B+ in liquidity, and over $600M in cash, making any liquidity issues a non-starter here.

It’s wrong to characterize the company’s second quarter as anything other than a challenging environment. Titanium dioxide disruptions in Altamira due not to company decisions or maintenance but to drought, continue in this period. It’s a good example of how climate can affect a company in ways that the company cannot control. The production outage was unexpected, but given pricing trends I do not believe that even at normalized production the results would have been substantially better either. That’s why the segment is moving towards cost savings – the current TT transformation plan targets over $120M in savings, and by 2Q24 the company has reached $100M of this target. This is what I would rather focus on – because it’s something that the company can control, and which shows the company delivering on execution promises.

The TSS and Refrigerants sector/s remains more volatile than TT. TSS had a slow start, but there was still some inventory lag due to excesses from previous periods. The company has now also split sales of refrigerants into two categories – Opteon and Freon – to distinguish the growing segment of Opteon, with the less Environmentally friendly freon. It’s Opteon that we want to focus on here, and this part of TSS saw double-digit quarterly top-line growth, where it now represents over 55% of the total sales mix. Meanwhile, Freon products are declining in sales popularity with continued volume declines, compounded by slower and lower pricing. The importance of Opteon can be further emphasized by new regulation from the US – the AIM Act – which focuses on refrigerants and the illegal import of other refrigerants. It’s my continued stance that the company is in a prime position to take advantage of the effects of such regulation and become a leader (more than it already is), in refrigerants that conform to these regulations. And this is a definite positive.

Other than this, the company is seeing plenty of stability in other parts of the business. The company’s sales of performance materials, in the APM sector, are solid. The company’s corporate expenses are also fully in line with expectations.

Do I therefore see a reason to justify a double-digit drop in the share price as of 2Q24? I can’t say that I do. I believe this represents more of a fear reaction to a company that has already done a number of things “wrong” (referring here to the irregularities), but as we saw in that article, it can turn around for Chemours very quickly (as is the case with a chemicals business).

For that reason, I believe the market is overreacting here. The second quarter did provide us with some very interesting business dynamics that affected the company’s bottom and top line developments – but none of these justify this sort of drop, not in the short, nor in the long term.

I therefore say that the upside to Chemours is unchanged.

It is this logical approach which I apply to all of my investments – and which has served me well, resulting in significant long-term upside for my investments. While it does at times result in very long wait times – several years – I do believe the upside by far outweighs the downside when it comes to this.

And for that reason, my valuation thesis for Chemours is as follows.

Valuation for Chemours – The company requires patience of around 2-4 years for a good ROR

Let me be clear in saying that Chemours remains a speculative stock – no doubt about that. The “Buy” rating I have on the stock comes with the clear message that this stock could, and has, go/gone up and down, and this is not something I expect to change.

What does that mean about the upside?

Like I said, I approach this investment – and any investment – using logic. If a company is not a “bad” business, and there is a fundamental demand for its products, that consequently means it’s an investable business at a certain price. My “job” becomes determining that price in the long-term, but preferably in the short term as well. To do this, we have certain tools and assistance.

BB-rating implies the company’s credit is stressed, and while liquidity is good, the company’s long-term debt/cap is up to almost 84%. This is not ideal, and something the company is likely to change. The market cap of sub-$3B also implies that while the company does have good market positions, it’s not one of the largest chemical players around.

The dividend is safe. I believe this. At a dividend rate of about $1/year, the 5.14% dividend we have today, is at a payout ratio of less than 90% – and the company has shown commitment to this. But again, it’s not ideal as I prefer companies to be more conservative here.

This means we need to account for these not-insubstantial risks when putting a price on the company. My price in my last article was $35/share. The company is now a long way from this, and as of this latest drop, Chemours has become materially more attractive.

What you need to understand is that there is an expected trough in 2024E. We’ve expected this for over a year at this point. But beyond that trough, an upside is coming. What upside is harder to tell, but I believe that there will be an upside that makes the price of $20/share look very, very cheap indeed.

I forecast at least 80% EPS reversal potential in 2025E, on the back of operational improvements and macro reversal – specifically TT pricing. The analysts following Chemours expect more than this, over 110% in 2025E, and another 37% in 2026E. If anything close to this materializes, even just trading at 8x P/E which is the company’s current average, we have an upside of no less than 25% per year, while investing at a very discounted rate. This makes for a total RoR of 70% until 2026E. (Source: Paywalled F.A.S.T Graphs Link)

There’s also the fact that Chemours has a historically proven trend of beating estimates. 44-50% of the time, the company’s reversal potential is non-trivial and they do better than 10-20% of forecast estimates. And when the company trades as low as this, most investors are likely to underestimate the upside and focus on the downside overly much.

It’s my place as a valuation investor to find the opportunities that others do not. To seek the “diamonds in the sand”. I believe Chemours could provide you with outsized returns at this valuation if you’re willing to hold it for a number of years.

I am – and that is why I am adding it here.

My thesis for Chemours is now as follows.

Thesis

- The company is fundamentally appealing due to its chemical portfolio but is hounded by potential legal issues and risks – both future and historical, as well as an unappealing liability profile. The recent disclosure is only the latest example of this. This needs to be discounted, but it’s entirely possible to do so – just keep your targets below 10x P/E and a share price of $35/share, adjusted for the new information, but remove some of that discount due to a higher current upside.

- I keep CC as a “Buy” and “Bullish” rating, with an overall price target of $35, below the current analyst average, but considered fair on a peer and risk/reward comparison. As of September 2024, I am shifting my target here somewhat, and now expecting a good 2-3 year trend, with the recovery of TT and other parts towards the 2H of 2024 or early 2025E.

- I do clearly maintain a “speculative” rating on the stock, however, and I would not make this a core position in any portfolio at this time. However, I am slightly adding to my position once again as of September of 2024.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

As things stand now, the company is still a “BUY”, and it fulfills every criterion that I have except one – the quality, due to its non-IG-rating. However, it’s very “speculative”, and that needs to be kept in mind. I reflect this by not giving it an overall qualitative rating.

{kind=link}