Torsten Asmus

Shares of controversial investment bank and financial services provider B. Riley Financial or “B. Riley” (NASDAQ:RILY) lost almost 70% of their value last week after the company suspended its quarterly dividend, delayed the filing of its quarterly report on form 10-Q and warned of substantial impairments to its asset base:

Net loss available to common shareholders is expected to be in the range of $435 million to $475 million during the three months ended June 30, 2024 or $14 to $15 per diluted common share compared to net income available to common shareholders of $44 million or $1.55 per diluted common share for the three months ended June 30, 2023.

Net loss during the three months ended June 30, 2024 is due in part to non-cash items including a significant decrease of approximately $330 million to $370 million in the valuation of our investment in Freedom VCM, the indirect parent entity for Franchise Group (“FRG”), and our loan to Vintage Capital Management, LLC, an expected impairment charge of approximately $28 million primarily related to the goodwill of Targus, and a charge of approximately $25 million related to a valuation allowance for deferred income taxes. The Company is in the process of completing the valuation of these items which could impact these estimates.

Last year’s ill-advised participation in the management buyout of Franchise Group continues to haunt the company.

While an external investigation cleared the company of related misconduct allegations, the deterioration of Franchise Group’s fundamentals has resulted in the requirement to impair the majority of the company’s investment in the Vitamin Shoppe parent and seemingly almost the entire $200+ million promissory note owed by former Franchise Group CEO Brian Kahn’s hedge fund Vintage Capital Management.

On last week’s conference call, the company also disclosed a SEC investigation related to the Franchise Group transaction and its dealings with Brian Kahn.

The impairments will result in an almost 40% reduction to the company’s core asset base:

Total loans receivable and securities and other investments is expected to be approximately $853 million to $893 million at June 30, 2024, a decrease of $509 million to $549 million from $1.40 billion at March 31, 2024.

On a more positive note, cash and cash equivalents increased by $46 million to $237 million on a sequential basis.

However, total cash and investments of $1.1 billion are dwarfed by almost $2.3 billion in outstanding debt and preferred stock.

Not surprisingly, the impairments will wipe out the remainder of stockholders’ equity on the balance sheet.

While the company claims “operating adjusted EBITDA” of $50 million for the second quarter, market participants are rightfully scrutinizing the viability of the company following recent events.

Considering B. Riley’s dire financial condition, tarnished reputation and resulting limited access to the capital markets in combination with an aggregate $870 million in bond debt maturing until the end of 2026, the company appears to be on the brink of collapse.

However, founder Bryant Riley is not willing to throw in the towel yet as evidenced by Friday’s take-private offer:

(…) while I am extremely confident in the Company’s ability to continue to successfully execute our strategy, I believe that the Company, its clients and customers, and employees would benefit greatly from private ownership of the Company.

I am therefore submitting this letter to propose a “going private” transaction that would result in my acquisition of all of the outstanding shares of common stock that I do not presently own.

I want to make it clear that I plan on continuing to report financials to the SEC and our bonds and preferred’ s will continue to be publicly traded. It is possible that I will continue to list on a secondary exchange if there are shareholders that would like to participate in this transaction.

That said, I am proposing to acquire all of the shares of common stock of the Company that I do not presently own for a purchase price of $7 per share. This valuation represents a 40% premium over the current price.

I expect that a special committee consisting of independent members of the board of directors of the Company (the “Board”) will consider the proposed transaction and make a recommendation to the Board. I do not intend to proceed with the proposed transaction unless it is approved by the special committee. The transaction would also be subject to a non-waivable condition requiring approval of a majority of the shares of common stock of the Company not owned by me, senior management, or any of our respective affiliates.

Consummation of the proposed transaction would be contingent on the “majority of the minority” stockholder approval described above, receipt of required regulatory approvals, and other customary conditions to closing. I plan to finance the transaction with debt and, potentially, equity from third party capital providers with whom I have deep and long-standing relationships. The proposed transaction would not be subject to a financing condition.

While the company’s securities rallied on the news, I don’t expect Bryant Riley’s hail mary move to succeed for a number of reasons:

- There’s no committed financing at this point and given recent events, even long-standing business partners might be reluctant to become involved with the company.

- Long-term shareholders would have to approve a transaction resulting in massive losses for them with all potential upside handed over to Bryant Riley.

- The transaction won’t close in the near future but with each given day likely resulting in the loss of talent and more business partners turning their back on the company, Bryant Riley’s bailout attempt might be too late.

Please note also that based on the terms of the company’s preferred stock (RILYP, RILYL), a change of control would provide preferred shareholders the right to convert their holdings into common shares. While the conversion would be subject to a share cap, each preferred share with a liquidation preference of $25,000 could be converted into 2,176 common shares.

Should Bryant Riley’s offer include these conversion shares, a change of control would result in a huge payday for current buyers and the requirement for Bryant Riley to finance up to an additional $70 million (4,563 outstanding preferred shares could be converted into 9.93 million new common shares thus representing an approximately 25% stake). However, as these new common shares would likely be issued subsequent to the take-private transaction, I do not expect them to be part of the offer.

As B. Riley would be a private company going forward, former preferred shareholders could face problems to sell their newly issued common shares.

At least in my opinion, the company is likely to collapse long before a potential take-private transaction might be completed, particularly with Riley being in danger of violating financial covenants governing its $500 million secured term loan facility with Nomura Corporate Funding Americas (“Nomura”).

With Nomura being the primary secured lender, they might not be opposed to a debt default.

In case of bankruptcy, I would expect the company or its assets being sold in a court-supervised auction pursuant to section 363 of the U.S. Bankruptcy Code.

While secured lenders are likely to recover most if not all of their claims, unsecured noteholders might face a major haircut with common and preferred equityholders holding the bag.

For speculative investors, Riley’s dire situation offers a number of compelling opportunities:

Investors betting on a near-term bankruptcy should consider shorting the company’s preferred and common shares even in light of elevated borrowing rates.

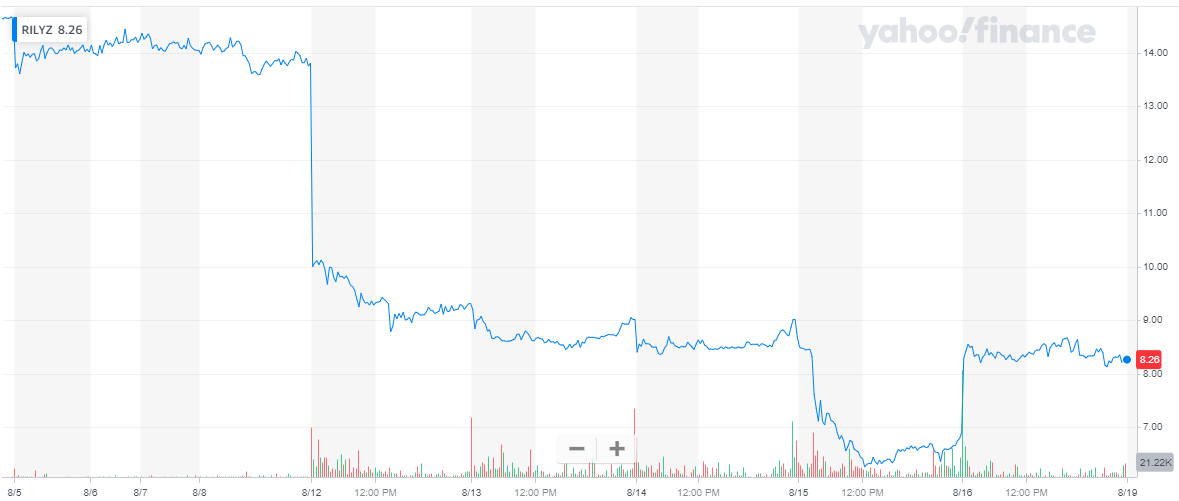

In case of a speculation on a potential recovery for the company’s unsecured debt, investors should pick the most discounted bonds (RILYT and RILYZ) as all notes are ranking pari passu.

Investors betting on Bryant Riley’s take-private offer including the above-discussed conversion shares should consider buying the preferred shares due to their favorable change of control provisions. The company’s unsecured notes (RILYM, RILYG, RILYK, RILYN, RILYZ, RILYT) would also be a major bailout beneficiary.

However, I would strongly advise against a bet on the company’s common shares as upside appears limited to the $7 offered by Bryant Riley while under a bankruptcy scenario, any sort of recovery would be highly unlikely.

Bottom Line

Following the disclosure of massive impairment charges and a SEC investigation related to the company’s participation in last year’s management buyout of Franchise Group as well as the suspension of the common share dividend, B. Riley Financial’s shares have lost almost 70% of their value in recent sessions.

On Friday, a non-binding take-private offer by founder Bryant Riley stopped the bleeding but I would consider chances for an eleventh-hour bailout as slim at best.

However, in order to have some skin in the game, I decided to take a small position in the company’s 2028 5.25% unsecured notes (RILYZ). A successful take-private transaction would likely result in the notes recovering most of last week’s losses, while a bankruptcy would not necessarily wipe out my investment (albeit a loss would still be likely).

Yahoo Finance

Please note that only the most speculative investors should consider getting involved with B. Riley Financial at this point. Dependent on the assumed outcome, there are currently a number of interesting bets across the company’s capital structure.

{kind=link}