Jonathan Kitchen

I have written a lot over the past two years about the importance of rates of change in high-frequency economic statistics. Most investors and many market pundits focus on the absolute numbers when determining the relevance of a data point for the economy and markets. For example, an inflation rate of 6% is horrible on a standalone basis, but what is far more important is the direction the rate is headed in over the coming months. If the 6% rate is going to gradually fall to 3%, then it is bullish. If it is going to gradually rise to 9%, then it is extremely bearish. Focusing on rates of change is what led me to the conclusion two years ago that the US economy would land softly, and I have never deviated from that outlook. Time will tell, but that forecast has gone from a slim minority to the majority view today. Now I am focusing on a different rate of change, but it is not a bullish one.

Everyone knows the Magnificent 7 stocks have powered a significant percentage of this bull market’s gains since it began in October 2022. The stock prices of Amazon (AMZN), Alphabet (GOOG) (GOOGL), Apple (AAPL), Tesla (TSLA), Nvidia (NVDA), Microsoft (MSFT), and Meta Platforms (META) continue to realize astoundingly positive rates of change. The issue at hand is that the fundamentals have been so outstanding that their rates of change are at a turning point.

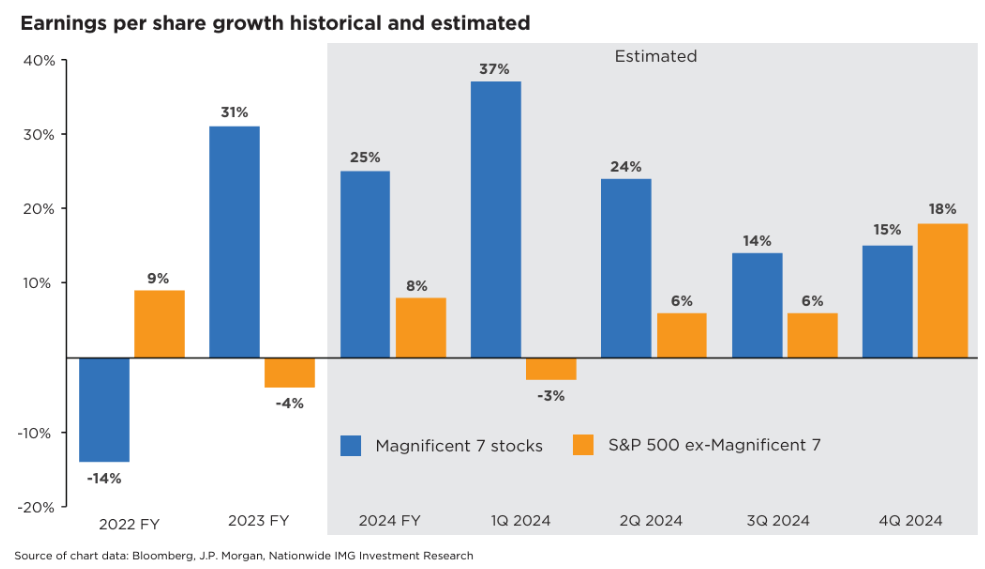

At the end of April, I shared the chart below, which depicts that the peak rate of earnings-per-share growth for the magnificent ones in 2024 was expected to occur in the first quarter of this year. While there have been upside revisions to forward estimates, the inflection point in earnings growth expected for the quarter just ended is still intact. This negative rate of change is glaringly obvious. Meanwhile, the remaining 493 names in the S&P 500 (SP500) were expected to realize growth for the first time in five quarters, which is a positive one.

Bloomberg

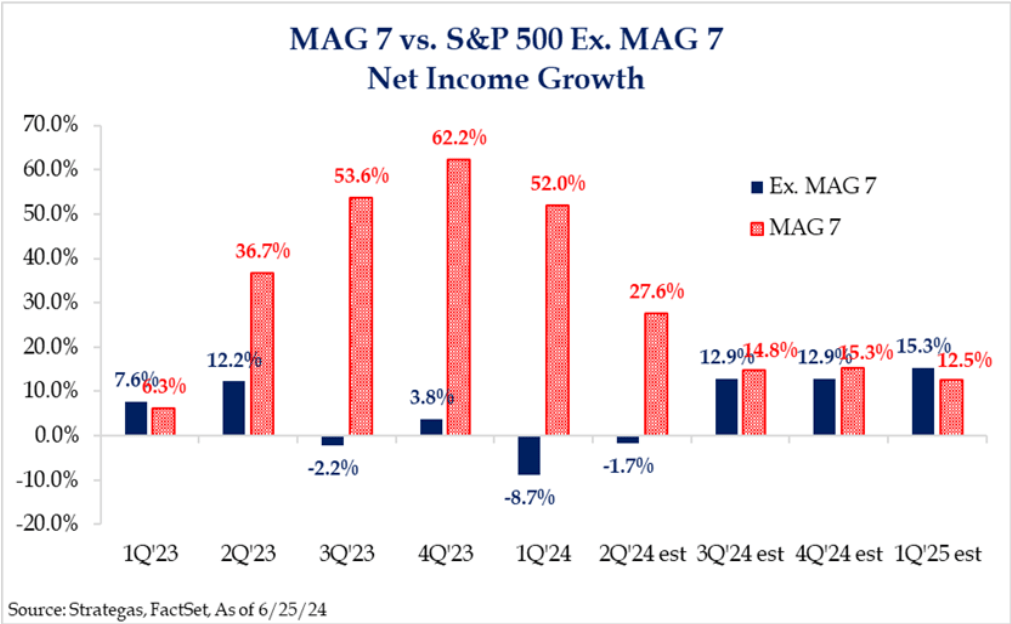

Two months later, I followed with a similar chart. It showed how net income growth rates for the Magnificent 7 had peaked in the fourth quarter of last year and were expected to fall dramatically from the first quarter of this year to the second. Again, a negative rate of change. Meanwhile, the decline in net income bottomed for the remaining 493 names in the first quarter of this year and is expected to improve dramatically in the current quarter.

Bloomberg

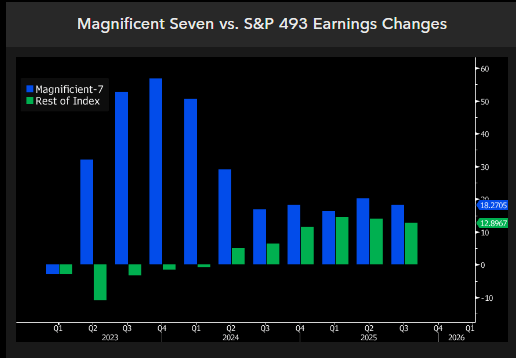

In the latest depiction of these two opposing rates of change, we see the same thing. The magnificent ones are expected to realize sharply lower rates of year-over-year earnings growth, while the remaining 493 members of the S&P 500 are expected to swing to year-over-year earnings growth for the first time in the past five quarters.

Bloomberg

It has been stunning to see investors ignore the deteriorating growth rate expectations for the Magnificent 7 by driving their stock prices to ever more dizzying heights. At the same time, they are largely ignoring the remaining 493 names on a collective basis, which are expected to realize improving fundamentals. Market prices typically lead to fundamental developments, but not in this case. At least not yet.

It will be interesting to see how investors respond to second-quarter earnings reports. I think the euphoria over AI has inebriated many who are not focusing on the fact that they are paying more for less when it comes to the Magnificent 7.

Lots of services offer investment ideas, but few offer a comprehensive top-down investment strategy that helps you tactically shift your asset allocation between offense and defense. That is how The Portfolio Architect compliments other services that focus on the bottom-ups security analysis of REITs, CEFs, ETFs, dividend-paying stocks and other securities.

{kind=link}