Money Trap xefstock

Performance Assessment

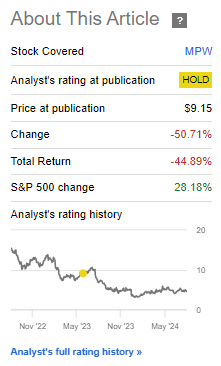

My last article on Medical Properties Trust (NYSE:MPW) was 1 year ago. At the time of publication, the sentiment on Seeking Alpha was strongly bullish. However, I warned of further asset quality risks in the REIT. Unfortunately, I rated the security a ‘Neutral/Hold’ instead of a ‘Sell’, which was clearly the wrong call:

Performance since Author’s Last Article on Medical Properties Trust (Seeking Alpha, Author’s Last Article on Medical Properties Trust)

Looking back, I think my analysis was both correct and timely. However, I made a mistake in the rating assessment as I believed a low valuation (P/B < 1) and a short squeeze risk due to a rather high short interest (20%) were saving graces. The key learning I extracted from this was to place far more weight on the balance sheet fundamentals, operational health of the business and the stock momentum than valuation and a temporary, perceived short squeeze risk.

Note that these learnings are not merely theoretical; I applied them successfully in my ‘Strong Sell’ views on B. Riley (RILY), which looked very similar to MPW despite being in a different business altogether; a weak balance sheet and cash-bleeding operational performance.

1 year later, not much has improved for MPW

I still have a bearish thesis on Medical Properties Trust:

- Impairments have become too regular

- The company is bleeding cash

- Leverage levels are high and unlikely to benefit much from rate cuts

- There are signs of operational weakness in the broader portfolio as well

- Despite trading below book value, it is likely a value trap

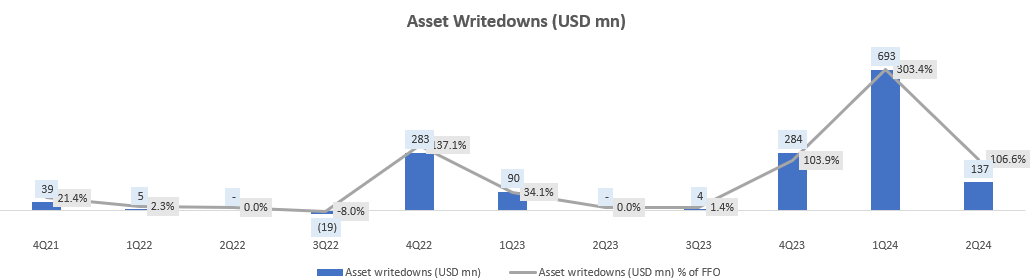

Impairments have become too regular

Impairments or asset writedowns are supposed to be one-time effects. However, for Medical Properties Trust, they have become a regular phenomenon:

Asset Writedowns (USD mn) (Company Filings, Author’s Analysis)

This is due to underlying weaknesses in its portfolio of tenants. For example, its largest tenant Steward making up 30% of overall revenues at the start of FY23 went under bankruptcy. And last year, another tenant called Prospect (11% revenue mix in FY22) also went significant impairments of almost $300 million.

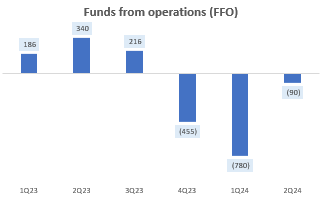

The company is bleeding cash

MPW’s FFOs are in a hole for the past 3 quarters, which have seen an outflow of $1.3 billion in total:

Funds from Operations (FFO) (USD mn) (Company Filings, Author’s Analysis)

This is not a good sign since the current liquidity (cash and equivalents) in the company is a mere $607 million.

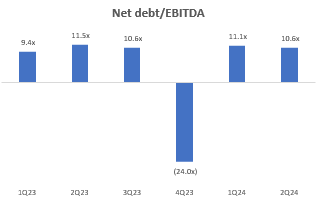

Leverage levels are high and unlikely to benefit much from rate cuts

Leverage levels are also high, with Net debt/EBITDA at 10-11x:

Net Debt/EBITDA (Company Filings, Author’s Analysis)

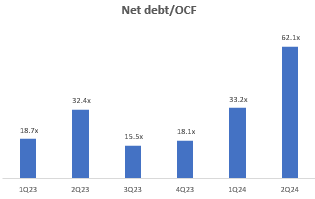

And the picture looks even worse if we look at a cash-flows measure of the extent of leverage used; net debt to operating cash flow (OCF) is more than 30x on an annualized basis and 62x as of Q2 FY24:

Net Debt/OCF (Company Filings, Author’s Analysis)

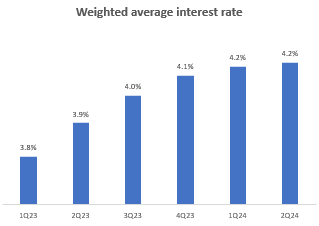

Moreover, with an elevated weighted average interest rate of 4.2%:

Weighted Average Interest Rate (Company Filings, Author’s Analysis)

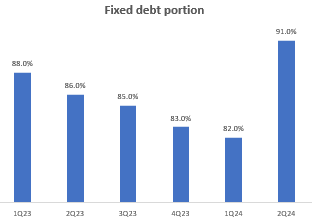

And a high fixed debt portion of 91%, jumping 900bps only in the last quarter:

Fixed Debt Portion of Total Debt (Company Filings, Author’s Analysis)

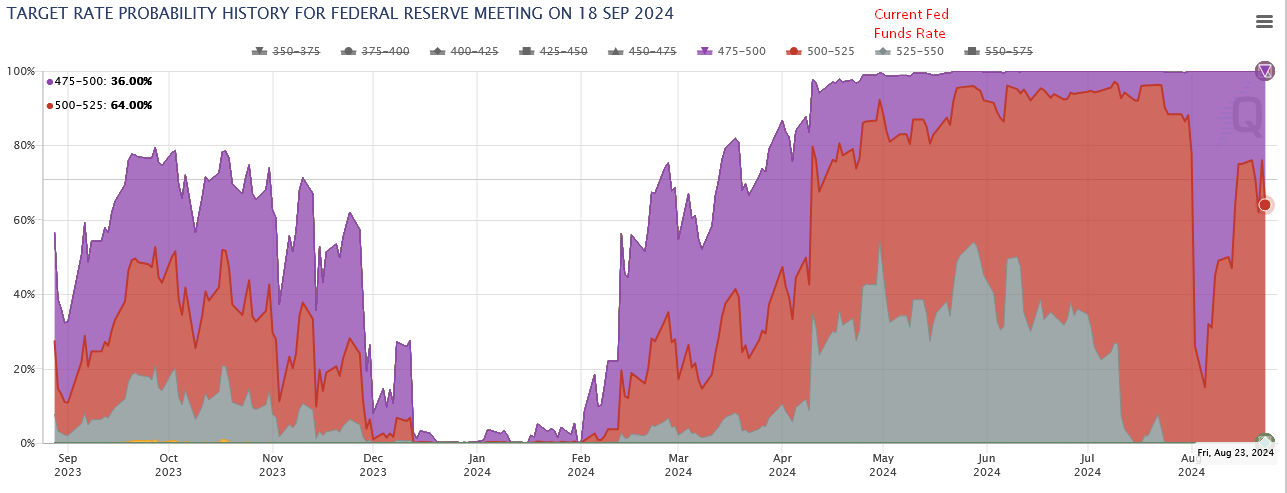

MPW has worsened its positioning to benefit from a rate cut upcoming in September 2024 (64% chance of a 25bps cut and a 36% chance of a 50bps cut):

Target Rate Probabilities for the September 2024 Fed Meeting (CME FedWatch, Author’s Annotations)

Federal Reserve Chair Jerome Powell as good as confirmed the market’s expectations for a rate cut in next month’s meeting a few days ago at the Jackson Hole Symposium:

The direction of travel [of rate cuts] is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.

– Federal Reserve Chair Jerome Powell at the 2024 Jackson Hole Symposium

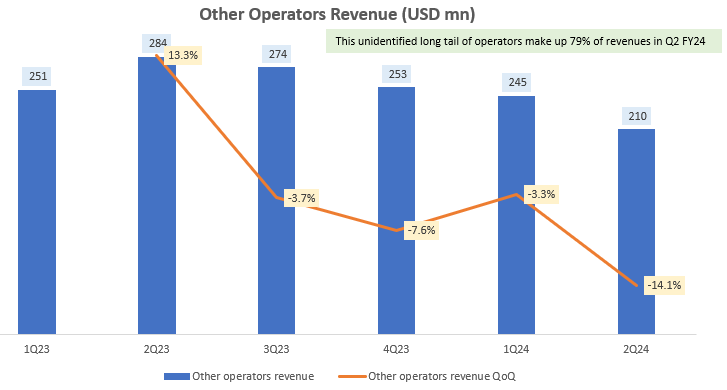

There are signs of operational weakness in the broader portfolio as well

As mentioned earlier, Medical Properties Trust’s largest tenants are undergoing financial stress. Moreover, it’s also seeing its business relationships turn sour as MPW is facing lawsuits from Steward.

But these issues are not limited to the larger, specific tenants named in MPW’s filings and supplemental disclosures. The business is also seeing YoY revenues decline at an accelerating rate, with the remaining long tail of operators making up 79% of total revenues:

Other Operators Revenue (USD mn) (Company Filings, Author’s Analysis)

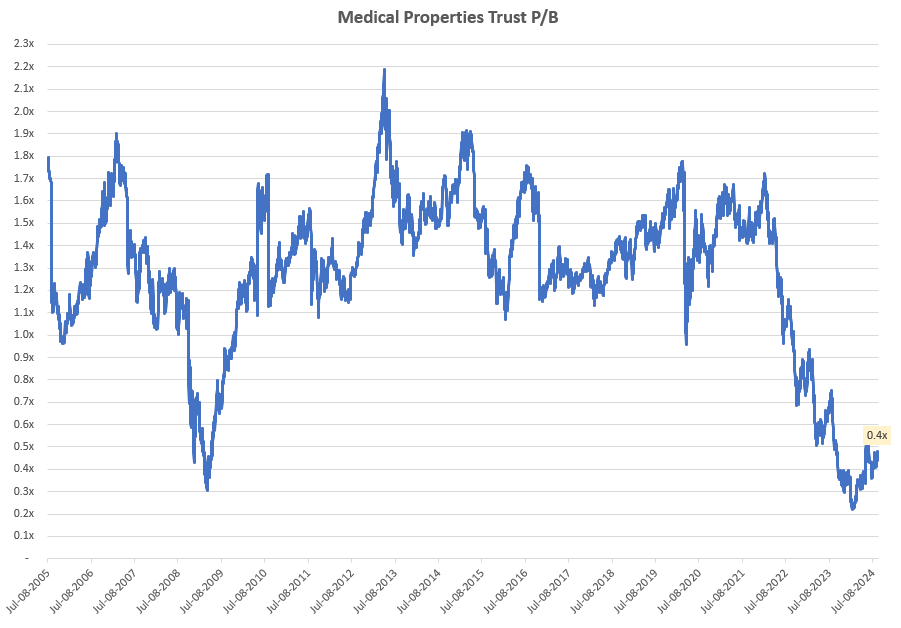

Despite trading below book value, it is likely a value trap

MPW is trading below book value at 0.4x P/B. This is even lower than the 0.7x P/B last year.

Medical Properties Trust P/B (Capital IQ, Author’s Analysis)

However, as mentioned in my performance assessment reflections at the start of this article, without favorable or at least improving fundamentals, I place less weight on this decadal low valuation levels.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do. All my charts reflect total shareholder return as they are adjusted for dividends/distributions.

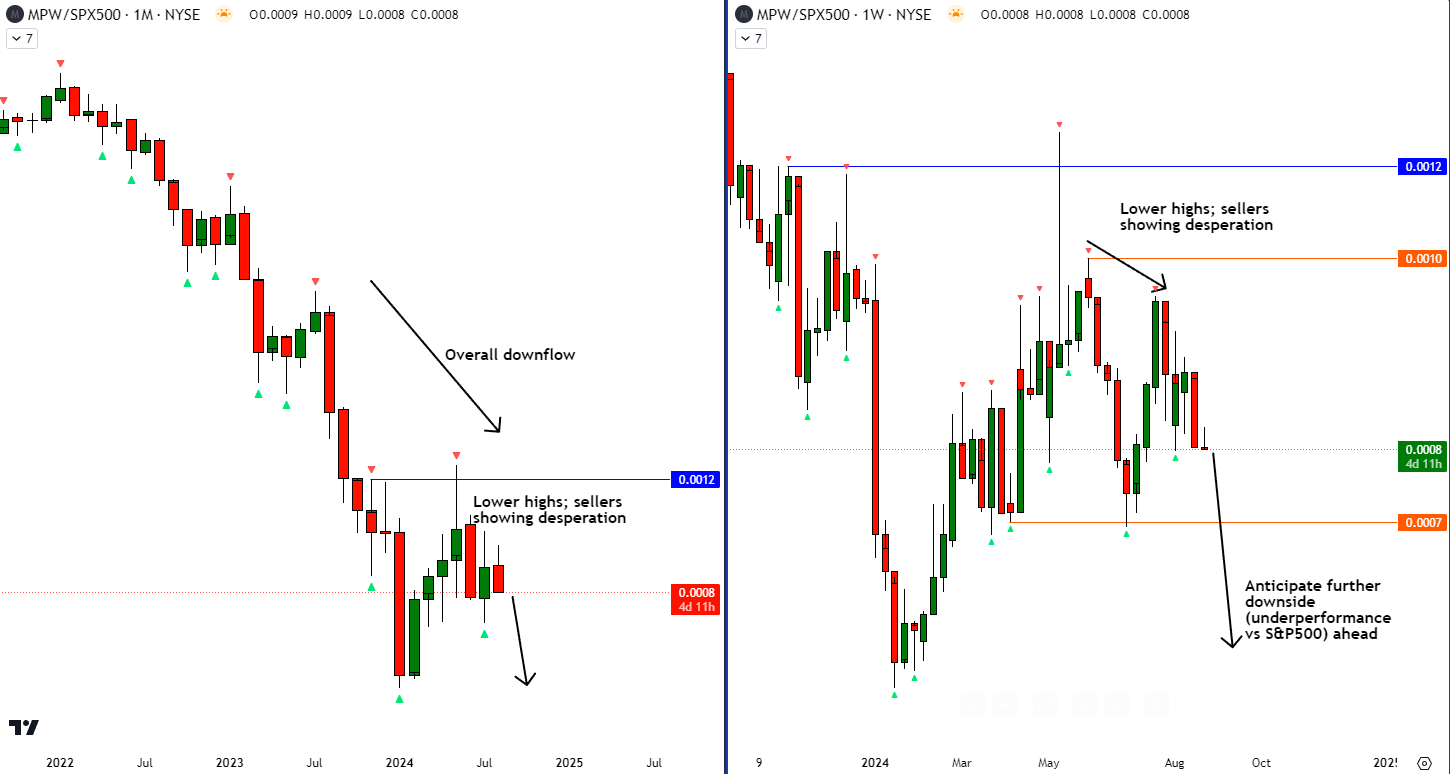

Relative Read of MPW vs SPX 500

MPW vs SPX500 Technical Analysis (TradingView, Author’s Analysis)

From a relative technical analysis perspective vs the S&P 500 (SPY) (SPX), MPW stock remains in an overall downward trend. On the weekly, we can see some signs of lower highs, indicating aggression and desperation by the sellers. Hence, going by the age-old wisdom of ‘don’t fight the trend‘, I anticipate further downside and hence underperformance vs the S&P 500.

Improving tenant fundamentals are a source of upside risk

A key source of upside risk, which I believe may improve the broader portfolio’s performance, is improving fundamentals in healthcare tenants. There are signs of this recently, as healthcare bankruptcies have slowed down, with bankruptcy filings expected to be 27% lower in 2024 vs 2023.

Takeaway & Positioning

My earlier analysis on Medical Properties trust warned of asset quality risks long well before the blowup in the stock due to the Steward (largest tenant) bankruptcy. However, I erred in rating the stock a mere ‘Neutral/Hold’ instead of a ‘Sell’ for some dubious reasons related mostly to seemingly low valuations, even when the balance sheet and operational performance of the company were shaky.

More than a year has passed since my last update on MPW. And my stance today on the healthcare REIT is a ‘Sell’. I still see glaring operational execution issues due to an FFO cash bleed, regular impairments, and declining revenues even in the broader portfolio of tenants. On the balance sheet side, I deem the leverage to be high and the debt position to be positioned unfortunately as the high and increased fixed interest rate debt portion undermines the firm’s ability to benefit from upcoming rate cuts. Given these weak fundamentals and a bearish read on the technicals vs the S&P 500, I believe even a 0.4x P/B valuation is insufficient to stage a genuine turnaround in MPW.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence. I also have a net long position in the security in my personal portfolio.

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

{kind=link}