Yarygin

NewLake Capital Partners (OTCQX:NLCP) recently released its Q2 2024 results, and after covering it for my first time in May, I decided to follow up and discuss these results, along with some of management’s comments from its Q2 earnings call.

I maintain my Buy rating, as NLCP offers an attractive cash flow instrument, with its growing 8% dividend yield.

Q2 Results

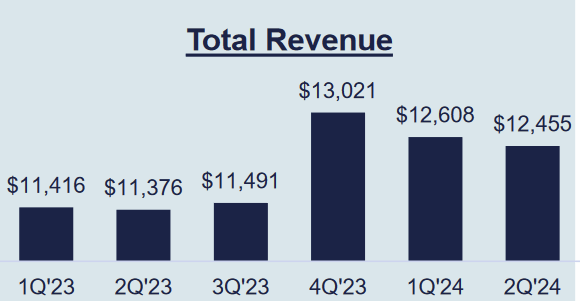

The company announced strong results, with increases in year-over-year revenue. That said, there were some declines from recent high points.

Q2 2024 Company Presentation

After a quarterly peak in Q4, it has been down slightly. In their latest 10Q (pg. 28), the company noted:

We own 32 properties, leased to 13 tenants. As of June 30, 2024, all of our tenants are performing under their lease agreement with the exception of one tenant discussed below.

Revolutionary Clinics failed to pay 50% of its June and July 2024 contractual rent under its lease agreement. The Company is currently in discussion with the tenant to negotiate a resolution, which could include rent deferrals or other concessions.

This seems to be a contributing factor, particularly as there were no underpayments on rent among their tenants in Q1. NewLake has had trouble with Revolutionary Clinics (“RC”) before. Elsewhere in the 10Q (pg. 20), they explained that they invested in warrants of RC’s equity in for delinquent rent, back in October 2023.

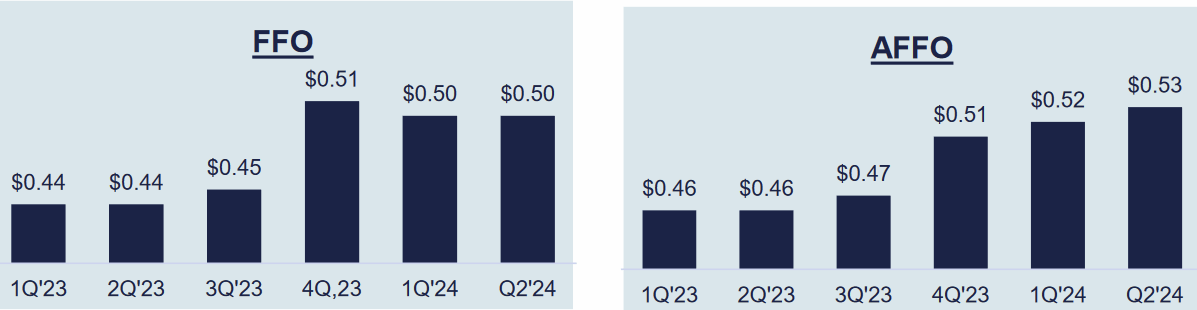

Q2 2024 Company Presentation

Still, the cash flow situation shows strength, and Adjusted Funds From Operation per share were even reported as higher sequentially. Absent any buybacks, this largely because the company has enjoyed lower operating expenses.

Q2 2024 Form 10Q

This allowed for a $0.02 in the quarterly dividend, roughly 4.9%.

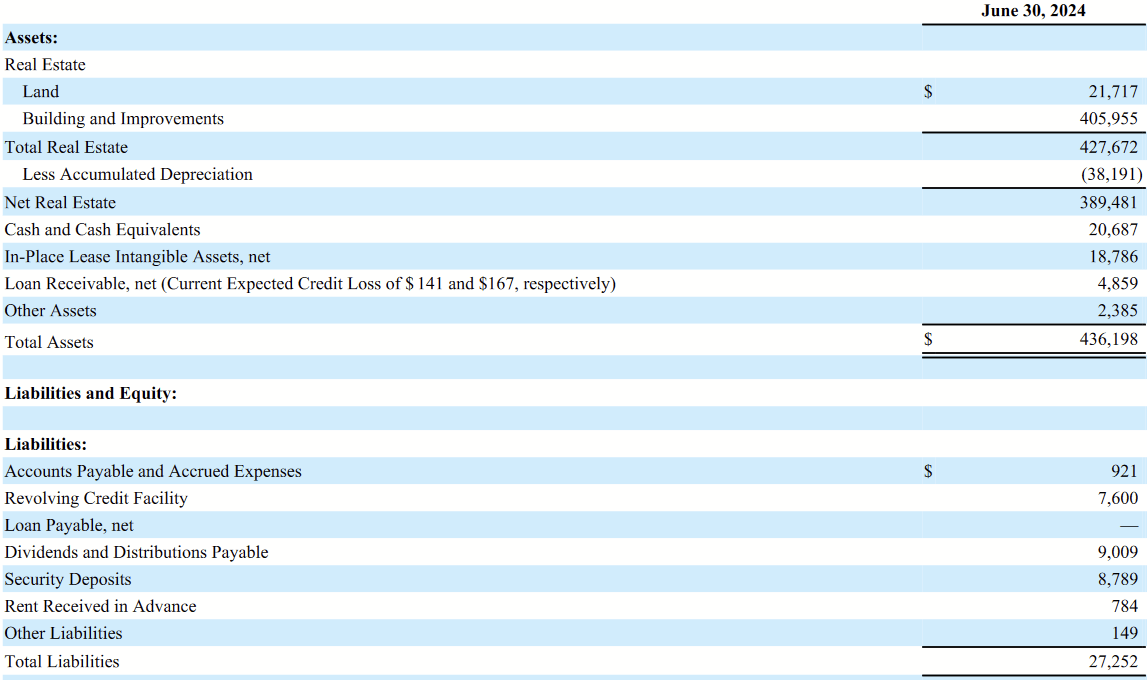

Balance Sheet (Q2 2024 Form 10Q)

The balance sheet, meanwhile, remains healthy, with virtually no debt and thus lacking a great deal of risk.

Q2 2024 Form 10Q

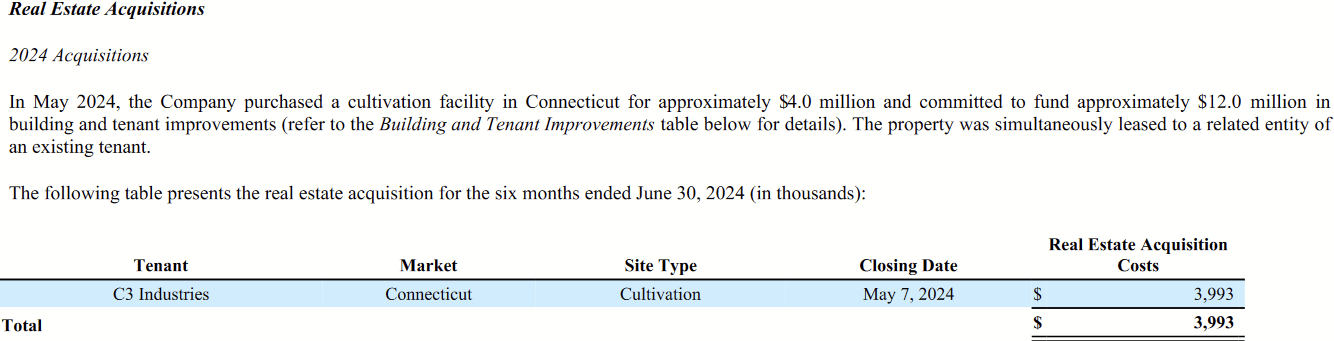

Just one new asset was acquired this time, with an existing tenant (C3 Industries), and it is still under development, so its contribution to cash flows will not be realized for some time.

Overall, I feel it was a good quarter for the company, continuing along its growth trajectory with only a minor hiccup from RC.

Future Outlook

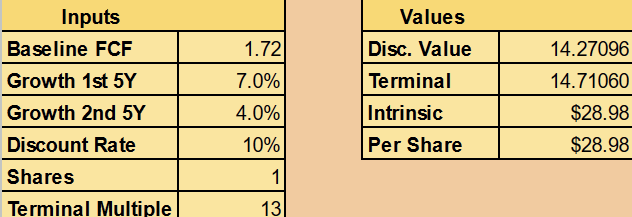

First, I want to update my valuation. Using a Discounted Cash Flow model (based on the dividend per share), I had valued it at $27.63. I had used the following assumptions:

- 7% annual growth the first 5 years

- 4% growth the next five

- Terminal multiple of 13

And to quote my reasoning:

While growth is showing signs of slowing, these new tailwinds and New Lake’s smaller size show to me that it could still manage a modest average of 7% the next five years (so not wild but better than inflation). As the portfolio saturates, new deals will each contribute less to growth, and management may find similarly attractive operators in need of sale-leaseback to be fewer, hence why I’ve lowered my growth expectations. A terminal multiple of 13, meanwhile, prices in a similar yield as today’s.

I maintain those assumptions, but I updated the DCF-like model to use the new, annualized dividend.

Author’s calculation

Priced for a 10% discount rate (typical return of a broad market index), that raises the valuation to $28.98.

Aside from the fact that cannabis has been a rapidly growing industry, there are other reasons we can reasonably expect single-digit growth for NLCP’s dividend. In the earnings call, CEO Anthony Coniglio explained:

And what’s important about having been one of the early movers in the sector as we’ve been developing relationships with the industry for over five years. And when you have a lease in place, it’s much easier for an organization that has familiarity with you, has a negotiated document with you to turn to you. And we certainly do see those conversations coming across the transom on a regular basis.

We saw the above play out with their latest acquisition of the cultivation site with C3. While they weren’t as early as Innovative Industrial (IIPR), they have been earlier than everyone else, and I think they still enjoy an advantage here.

More broadly, their sale-leaseback transaction remains attractive (relatively speaking) to cannabis operators who want to invest for growth. Coniglio also explained in the call:

…we’ve engaged in this dialogue with management teams about do they take the shorter-term debt, they enter into a sale-leaseback process. And I’ll share with you what we tell them is what we find is the companies that choose sale-leaseback are doing so because not only is it competitively priced relative to where the debt opportunity is today, not only do they want to get maximum proceeds because usually your sale-leaseback transaction provides greater proceeds that mortgage that.

Banks are heavily limited in their ability to lend to cannabis operators by federal law, so mREITs are essentially their next option, an example being AFC Gamma (AFCG), and they similarly command high interest rates because of limited access to capital in this space. The difference with a lease is that there’s no upcoming principal repayment, and lacking many other lenders, the odds of successfully refinancing are lower. This further supports my view that NLCP can continue to grow its dividend attractively.

The biggest risk I perceive is more long-term in nature, wherein federal law may finally relax to the point that cheap mortgages and other forms of financing are more attractive than sale-leasebacks at these yields. While NLCP could potentially make this up by taking on their own leverage to amplify returns, it would still change the dynamic and potentially be disruptive to new acquisitions or any leases that need renewal.

Conclusion

NewLake continues to push forward, offering an attractive dividend yield of over 8% at current prices. With limited financing options, operators must rely on sale-leasebacks to fund their growth. NLCP is therefore well-poised to ride that growth with high yields on their increasingly diverse portfolio of cannabis properties. While an evolving regulatory environment demands investors not be complacent, the current undervaluation makes the shares a wonderful buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

{kind=link}