tadamichi

The iShares 0-5 Year High Yield Corporate Bond ETF (NYSEARCA:SHYG), which we covered a couple of months ago around the previous inflation data, may like the falling credit spreads and possibly also the new CPI readings, but we still see issues. The CPI’s decline below 3% may not be enough for the Fed. While disinflation is visible, it is slow, and progress could be undone. We are also generally apprehensive about credit spreads. They’ve come down again after the market scare on the jobs report, but they are still low. On both accounts, we avoid SHYG for its sensitivity to credit spread changes but also its substantial duration. Still not the play for us, and would probably not be the play even if CPI were to cool more.

SHYG Breakdown

The key data to know are that SHYG has mostly BB and B rated bonds in it, meaning meaningful credit risk and within the junk status, and that it has a duration of around 2.25 years, which means a decent amount of sensitivity to changes in SHYG YTMs, both from credit spread revisions and from changes in the market imputed risk-free rate.

On the general factors first, the jobs data last week really scared markets and caused a bit of a market panic. Credit spreads rose but then fell again, but not entirely down to the historically low levels they were inexplicably sitting at before the jobs data, which ended up not even being that scary, and possibly driven by weather effects and the blip in seasonal employment effects.

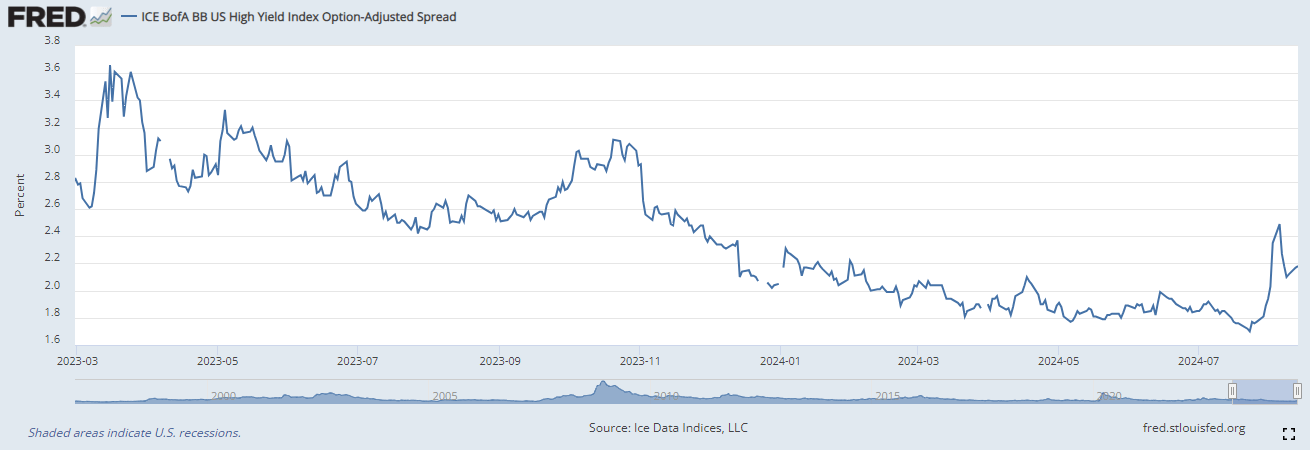

Credit spreads BB (FRED)

Credit spreads for BB instruments and B rated instruments are still at historically low levels. The economic situation, with large maturity walls and an uptick in financial distress, still doesn’t appear to be reflected in high-yield bond prices. Credit spreads are lower than in previous periods of less considerable outstanding macroeconomic questions.

However, we want to talk more about the very latest CPI data. It’s below 3% which is technically the edge of the Fed’s policy band on the upside. But the components of inflation that anchor expectations are upticking, including shelter. Also, oil could rebound and cause issues for the overall CPI figure. Services are also being very sticky, inherent in their connection to the stickiness of labour inflation, which is driving expectations. Inflation expectations are still 3% as of the late July Michigan survey.

We think that this one reading is not enough. Even if it is sustained at this level, it won’t be enough for a cautious and sensible Fed. Relenting in policy could undo the hard-fought and limited ground already gained. This interacts with the credit spread situation as there is some negative reflexivity in high-yield bonds that otherwise kicks in, which is that a weaker economy also means lower benchmark rates, which can aid the credit picture a bit for those BB and B companies holding on. But in this case, where there is a sticky inflation issue, that negative reflexivity is not present.

Bottom Line

Inflation expectations have reason to remain too high, persisting the high inflation. Recent data continues to show a high-expectation figure. The slight downtick is alright, but oil could turn and there’s also the issue that the really sticky and scary elements of inflation, those also with the largest persisting effect through the labour channel like shelter, are still up. At least there is other commodity and goods deflation in a veritable reversal from the COVID-19 era goods boom. Still, on outstanding macro questions and less negative reflexivity impacting the contribution to YTMs from credit spreads and also the likelihood that markets will get excited for nothing again on the CPI reading have us being wary of SHYG. The credit spread exposure would have us looking at risk-free Treasury ETFs at most, which are comparatively more interesting, also because they have the benefit of carrying lower expense ratios than the relatively high 0.3% on SHYG.

Thanks to our global coverage, we’ve ramped up our global macro commentary on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration.

{kind=link}